Analyzing Todays 30 Year Mortgage Rate Drop: Historical Context and Market Reaction

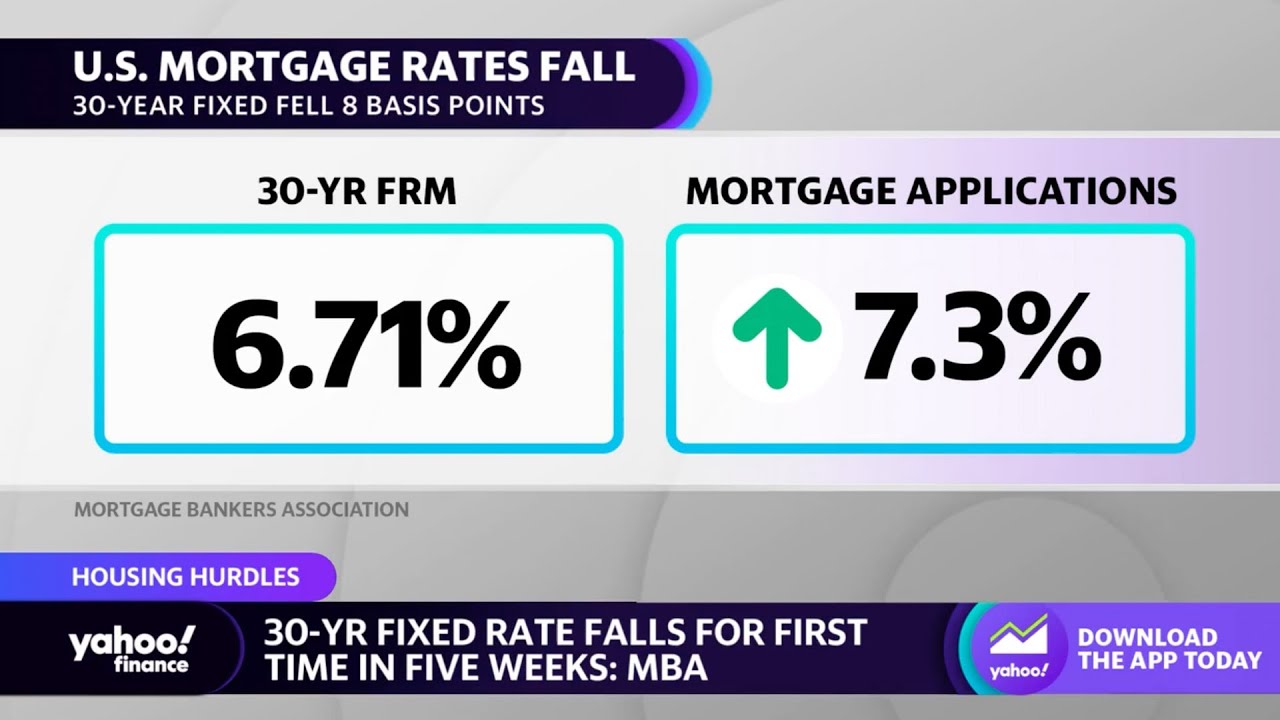

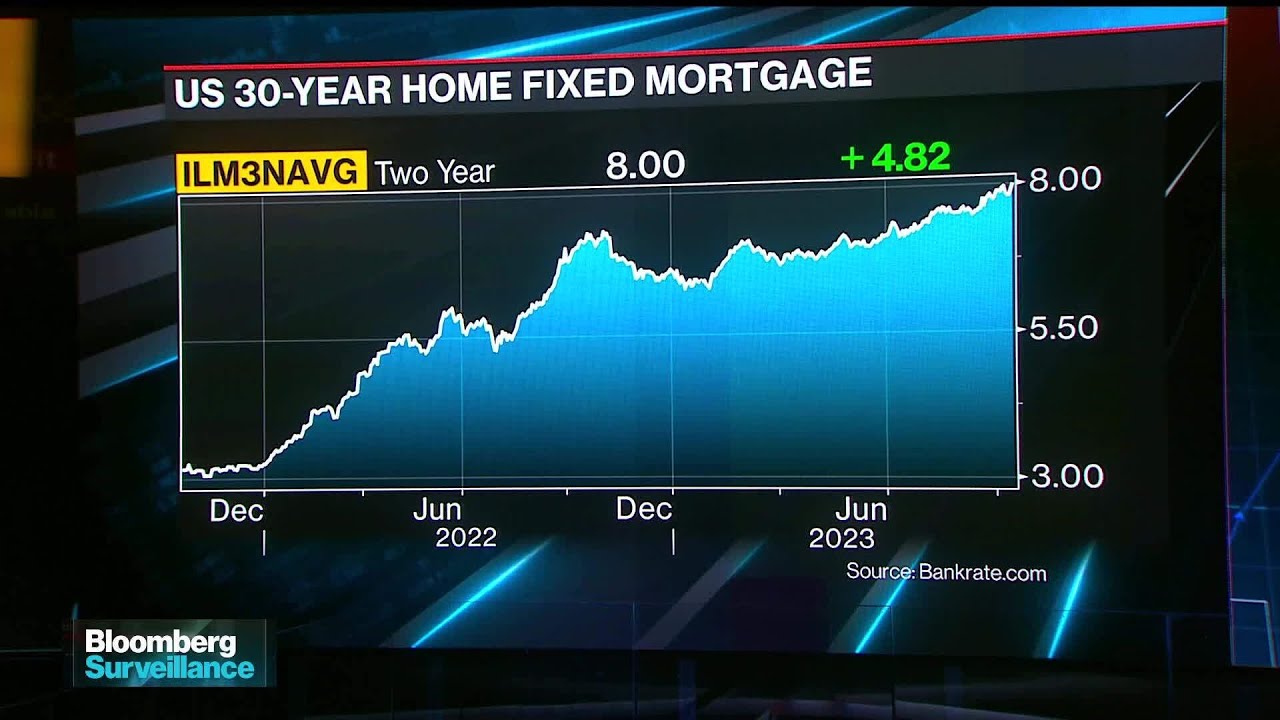

Just like the suspenseful plot twists in Tsukimichi Moonlit fantasy season 2, the mortgage market has delivered its own surprise: today’s 30-year mortgage rate has gracefully dipped below the 7% threshold. This movement is a significant deviation from the recent 23-year high of 8.03% back in October 2023. Now averaging at 6.74% the week of March 14, 2023, according to Freddie Mac, this shift is more than just a number—it’s a beacon of hope for borrowers nationwide.

Reflecting back, we’ve seen the pendulum swing from the record low of merely 2.65% in January 2021, which gave the real estate market a jolt akin to the best energy drink you could imagine. While nobody is expecting a return to those historic lows just yet, with today’s 30-year fixed-rate mortgage hitting a rather significant milestone, we’ve certainly got the market’s undivided attention.

As we sift through the myriad of factors that influence these numbers, reactions have emerged from every corner of the housing sector—much like the buzz that surrounds a celebrity news revelation such as Jennifer Lopez pregnant. Homebuyers and investors alike are perking up their ears to understand what this development means for them.

Factors Influencing Todays 30 Year Mortgage Rate Decline

Behind the scenes, like the carefully crafted narrative of a Drew Tarver performance, various factors are at play influencing today’s 30-year mortgage rates. The all-powerful Federal Reserve’s monetary policies are key – their actions often influencing the ebb and flow of mortgage rates. The recent dip signifies a less aggressive stance, perhaps, on inflation which in 2021 had lenders issuing loans with a cautious eye.

Additionally, the inflation rate itself acts as a harbinger for rising or falling mortgage costs. When inflation fears recede, rates tend to soften, granting relief to homebuyers. Let’s not overlook the bond market—mortgage-backed securities are the stage upon which mortgage rates perform, and recently demand in this niche has been robust, contributing to lower yields and, ergo, lower mortgage rates.

Even international headwinds have had their say, like a distant ripple reaching our domestic shores. Instability abroad can make U.S. investments, including real estate, more appealing and, by extension, affect mortgage rates.

| Date Noted | Average 30-Year Mortgage Rate | Comparison to Historical High (Oct. 2023) | Comparison to 2021 Average Rate | Significance |

|---|---|---|---|---|

| March 14, 2023 | 6.74% | 1.29% lower | 3.78% higher | Cooling from Oct. peak, but elevated. |

| October 2023 | 8.03% | 23-year high (no comparison) | 5.07% higher | Reached a 23-year high. |

| January 2021 | 2.65% | 5.38% lower | 0.31% lower | Record low at the time. |

| Average of 2021 | 2.96% | 5.07% lower | (no comparison) | Represented historic low rates for the year. |

| March 5, 2024 | Data not provided | Data not provided | Data not provided | Relevant data might provide trend insight. |

Comparing Todays 30 Year Mortgage Rate with Other Loan Options

The 30-year mortgage rate is like the leading actor in our financial saga, but co-stars, like the 15-year mortgage or the adjustable-rate-mortgage (ARM), are vying for attention, too. While today’s interest rates 30 year fixed invite lower monthly payments, a 15-year loan offers the allure of a lower total loan cost, although with higher monthly expenses.

An ARM could provide a low introductory rate à la promotional teaser; however, this rate could fluctuate over time. With the current rate changes, homeowners may wonder if it’s akin to stepping into the surreal setting of the From movie and opting to refinance. Real-time quotes from leading lenders such as Wells Fargo, Chase, and Quicken Loans are becoming more competitive, nudging borrowers to consider their options.

Real Estate Market’s Response to Today’s 30-Year Mortgage Rate Dip

Faster than the spread of exciting news in a small town, the real estate market is abuzz with the chatter over declining mortgage rates. Housing demand finds a second wind, and buyers’ purchasing power enjoys a corresponding uptick. Certain areas, like burgeoning tech hubs or cities with ongoing housing shortages, could see a proportionally higher impact.

Builders, their hard hats reflecting the hopes of many prospective homeowners, are now eyeing this rate as a potential catalyst for increased construction projects. Meanwhile, first-time homebuyers might be sizing this up as their golden ticket into the market. With rates lower than they’ve been in over a year, “For Sale” signs might start switching to “Sold” with increased regularity.

Long-Term Predictions for Todays 30 Year Mortgage Rate Trajectory

Predicting mortgage rates can be as tricky as forecasting the next big plot twist in popular entertainment. Yet, economists and market gurus are weighing in, positing that while today’s dip brings relief, the trajectory could swing back in response to unforeseen economic turbulence or policy changes.

Picture two scenarios: an economy regaining robust health could lead to rate hikes to keep inflation in check, or ongoing global uncertainties could see a sustained lower-rate environment. Government interventions, new housing policies, and regulatory frameworks could also serve as rate influencers.

Pros and Cons of Locking in Todays 30 Year Mortgage Rate

“Should I lock in?” That’s the million-dollar question for borrowers mulling over todays 30 year mortgage rate. There are definite perks to securing a rate south of 7%—predictable monthly payments and overall interest savings over the life of the loan emerge as clear winners. However, let’s not sugarcoat it—rates might dip even further, and those who lock in might be left feeling like they jumped the gun. Mortgage lock-in strategies come in various forms, and a financial advisor’s expertise can radically improve decision quality.

Innovative Mortgage Planning Strategies in a Volatile Rate Environment

Just as technology has revolutionized our lives, the mortgage industry isn’t lagging behind. Advisors are championing innovative planning approaches to leverage current rates. Think adjustable-rate mortgages with rate caps, or loans that offer the flexibility of modifying certain terms mid-life. Furthermore, online mortgage platforms are democratizing the process, making information and tools more accessible and empowering better borrowing decisions.

What Todays 30 Year Mortgage Rate Dip Means for You

For those sneaking a peek at their mortgage options, here’s the deal: now could be a tempting time to dive in or refine your existing mortgage. Assess your unique financial situation—is the timing right for you to buy or refinance? The rate change holds the potential to shift your financial planning gears and may just be the spark needed for reevaluating your investment mix.

Navigating the Future: Adapting to Rate Fluctuations with Confidence

Armed with knowledge and keen astuteness, you’re adeptly positioned to navigate through the mortgage rate rapids. Consulting with financial mavens is invaluable during these dance-on-a-dime times. Remember, rates may rise and fall like tides, but with a strategic, educated approach, the dream of homeownership remains within reach. So, as we’ve embarked on this detailed exploration of todays 30 year mortgage rate, let’s step forward with assurance, ready to make the smartest moves in our mortgage journey.

Unraveling the Twists of Today’s 30-Year Mortgage Rates

Who could’ve guessed that the meandering world of mortgage rates would give us such a thrill? Just when you blink, today’s 30-year mortgage rate does a little dip and dance, ducking below the big old 7%. But let’s not just chat about numbers and percentages. Let’s dive into some tidbits that make mortgages more than just a yawn at the bank.

You might think the concept of a 30-year fixed mortgage has been around since the dinosaurs, but hold your horses! It was only after the Great Depression that the U.S. government stepped in, creating long-term, fixed-rate mortgages as a way to help American families own homes. Fast forward to today, and peeking at today’s 30-year fixed-rate mortgage feels like sneaking a glimpse into the nation’s economic soul.

Hold onto your hats, because here’s a quirky byte: did you know that countries like Japan and Switzerland have had negative interest rates? Imagine that! Paying less over time rather than more. Alas, that’s a story from a land far, far away from today’s interest rates 30-year fixed, which hover in positive territory, influencing everything from your monthly budget to the type of home you can afford.

And while we’re prattling on about mortgages, get this – not all 30-year mortgages are created equal. Once upon a time, before today’s 30-year mortgage rates garnered headlines, would-be homeowners had to muster up a hefty 50% down payment. Nowadays, you can snag a mortgage for much less upfront, smoothing the path to homeownership like a hot knife through butter.

So, there you have it – a dollop of trivia on today’s 30-year mortgage rate, spiced up with a dash of history and splashed with a pinch of international intrigue. It’s not just about snagging a good rate; it’s about appreciating the kaleidoscope of factors that make each percentage point something to chat about over your white picket fence. Just imagine the stories your mortgage rate could tell if it had a voice!

What is the current 30-year fixed-rate mortgage?

– Ah, talking current numbers! As of the week of March 14, 2023, 30-year fixed-rate mortgages are sitting pretty at an average of 6.74%, per the handy data from Freddie Mac. So, if you’re in the market for a new home, that’s the magic number to keep in your back pocket!

Have 30-year mortgage rates dropped?

– Well, isn’t this a breath of fresh air? Yup, 30-year mortgage rates have indeed taken a tumble – they’re down a notable 1.29% from the heart-stopping 23-year high of 8.03% recorded in October 2023. Looks like those rates decided to chill a bit!

Are mortgage rates going down in 2024?

– As the saying goes, “What goes up must come down,” right? In the wacky world of mortgage rates, though, predictions are about as solid as a house of cards. But good news – this year has shown a friendly trend, with rates cooling off from their October highs. Though they’re still higher than your grandma’s apple pie recipe, there’s a whiff of hope they might keep descending in 2024.

What are real time 30-year mortgage rates?

– Looking for real-time 30-year mortgage rates? Hold onto your calculators, because those numbers bounce around like a kangaroo on a trampoline! For the freshest, up-to-the-minute figures, your best bet is to check with lenders or financial news outlets that update daily.

Are mortgage rates expected to drop?

– Ah, the crystal ball question! While we all wish we had a direct line to the future, it’s tough to say with certainty if rates will drop. They’ve been playing hard to get since reaching a high in October 2023, but our fingers (and toes) are crossed for relief down the line!

When can we expect mortgage rates to drop?

– Timing the market is trickier than finding a needle in a haystack. Mortgage rates are a fickle bunch, influenced by enough factors to make your head spin. Since they’ve recently dipped from their October peak, we might see more drops, but don’t set your watch to it; economic conditions love to surprise us!

How low will mortgage rates drop in 2024?

– 2024 could be the year of the rate roulette, with mortgage rate forecasters throwing numbers around like confetti. Some speculate they’ll dip lower, but pinning down how much is like trying to nail jelly to a wall. We’ll just have to wait and see!

Will mortgage rates decline in 2025?

– Predicting 2025’s mortgage rates is a bit like trying to guess next year’s “Word of the Year” – it’s all up in the air! Factors like inflation, economic policies, and global events will have their say, so fingers crossed the trend leans towards decline.

Will interest rates fall?

– Interest rates are the moodiest – one minute they’re up, the next they’re down. Overall, they’ve shown a tad willingness to fall after peaking in late 2023, but whether they’ll bend lower or bounce back up is the million-dollar question.

Will 2024 be a better time to buy a house?

– Looking to stake your claim in Home Sweet Home-ville in 2024? The crystal ball’s a tad cloudy, but given rates have started to retreat from their heights, the year could potentially serve up more favorable conditions than we’ve seen. Keep your ears to the ground!

What will mortgage rates be in 2025?

– Wish we had a time machine to sneak a peek at 2025’s mortgage rates, huh? While that’d be the ultimate life hack, for now, we’re all playing the guessing game. Economic experts can make educated guesses, but in reality, it’s about as predictable as your Aunt Edna’s mystery casserole.

What will home mortgage rates be in 2025?

– Anyone got a magic 8-ball? Home mortgage rates in 2025 are still anybody’s guess. The economic tea leaves aren’t super clear right now, but here’s hoping they spell out some good news for future homeowners.

What is the highest 30-year mortgage rate ever?

– Ever heard of “historically high”? That’s how we’d tag the 8.03% peak of October 2023 – a 23-year record-smasher for 30-year fixed mortgage rates. It’s the kind of number that can make your wallet weep!

Why a 30-year mortgage is better?

– Opting for a 30-year mortgage isn’t just about spreading payments like butter over toast, it’s about keeping those payments lower and more manageable, too. This can leave you some wiggle room in your budget for life’s other adventures – because, let’s face it, who doesn’t love a little extra cash for the fun stuff?

Is a 30-year mortgage more expensive?

– Going the long route with a 30-year mortgage can indeed be more of a marathon than a sprint money-wise. Interest piles up over a longer period, so in the grand scheme, you’ll likely fork over more than with the speedier, but heftier, payments of a shorter-term loan. But hey, for many, it’s worth the trade for monthly payment breathing space.