Understanding 30 Year Fixed Rate Mortgage Rates

The Attraction of Fixed Rate Mortgages in Uncertain Times

Hey, let’s face it, we’re living in some unpredictable times, folks! The roller coaster rides of interest rates in previous years have left many of us craving a spoonful of stability when it comes to our finances. That’s where fixed-rate mortgages come in, standing tall as the Statue of Liberty, promising predictability in a sea of economic chaos.

Fixed-rate mortgages, especially those with a 30-year term, are a godsend for long-term planning. They’re like your favorite comfort food – they just never let you down. You can budget effectively, knowing that your mortgage payments will remain consistent throughout the duration of the loan, no surprises there!

And let’s not underestimate the psychological appeal; there’s a homeowner peace of mind that comes from locking in a fixed rate. It’s akin to putting down roots in a community; it’s stable, it’s secure, and it’s yours.

How Are 30 Year Fixed Rate Mortgage Rates Determined?

Ah, the mysterious forces at work behind the curtain! Mortgage rates, especially the 30-year fixed mortgage rates, are influenced by a ballet of economic indicators. The Federal Reserve’s policies may lead the dance, but the economy’s performance plays its tune.

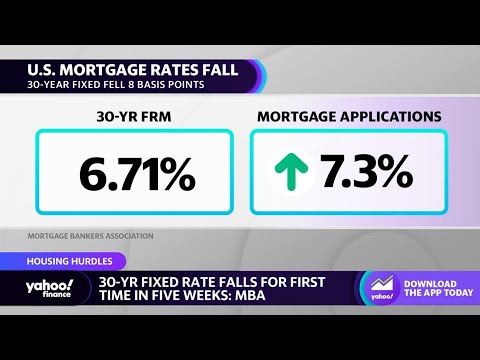

Looking back at history, including the all-time low of 3.25% interest rate back in 2020, rates have wobbled like a child’s first bike ride. However, various factors like inflation, the overall health of the housing market, and even global economic events can make the rates pivot.

The Current State of 30 Year Fixed Rate Mortgage Rates

Fast forward to 2024, and the data is singing! We are witnessing impressively low 30-year fixed mortgage rates today – lows that would have our parents do a double-take. Compared to the gnarly double-digit rates of the 1980s, these are more than just figures; they’re a testimony to a favorable lending environment.

Experts, donning their financial spectacles, point to a smorgasbord of causes. They highlight controlled inflation, robust economic patterns, and other financial fairy dust that’s keeping these rates at historic lows.

The Impact of Historic Lows on Home Buyers and the Real Estate Market

Now, let’s weave some real-life magic into our narrative with a couple of case studies. Think about our friend, the first-time buyer, who’s suddenly got a purchasing power like a superhero – zooming into the housing market with a pre-approval letter as their cape.

Then, there’s the seasoned homeowner, eyeing their mortgage like it’s a financially draining nemesis. They go for the refinance – and bam! They’re saving more dough than a bakery on a Sunday morning. This combo of lower payments and increased equity? It’s stirring up the market dynamics more than a top chef’s best recipe.

Comparing 30 Year Fixed Rate Mortgage Rates with ARM Rates

Picture this: You’re at a financial crossroads – one sign pointing to “30-Year Fixed”, the other to “ARM” (Adjustable Rate Mortgage). ARMs are like that carnival ride that seems calm at first and then, whoops, there’s a twist! They start with a lower rate which can change over time, potentially faster than a chameleon on a rainbow.

In some corners, particularly when interest rates are doing a high-wire act, an ARM can be kind of tempting. Sure, there’s a gamble involved, but sometimes life is about rolling the dice.

Speaking of real deals, banks and lenders are throwing out some competitive ARM rates to entice the risk-takers. But as always, buyer beware.

How to Secure the Best 30 Year Fixed Rate Mortgage

Alright, let’s get down to the brass tacks of mortgage shopping. You want the lowest rate possible? Then pump up that credit score, save up for a solid down payment, and let’s compare the big players like Bank of America, Wells Fargo, and Quicken Loans. Each has a suite of offerings in 2024 that would make a Swiss Army knife look under-equipped.

But remember, it’s not just about the rate. There’s a maze of fees and other costs that could ambush your budget if you’re not careful. So grab a magnifying glass and read the fine print like it’s a treasure map.

Pros and Cons of Locking in 30 Year Fixed Rate Mortgage Rates Now

We snagged a coffee with a financial planner to get the lowdown on whether you should lock in a rate now. “It’s like catching butterflies,” they said with a knowing smile. “If you’ve got one in your net, securing a low rate now can save future headaches.”

However, there’s always the ‘what ifs,’ right? What if rates go lower? Well, then you’ll be wishing you had a time machine. The key is financial planning – consider where you’re at now and where you see yourself in the future.

The Long-term Implications of a 30 Year Fixed Rate Mortgage

Imagine your mortgage as a marathon. Over time, with a 30-year fixed rate mortgage, you could be pocketing enough savings to take a cruise around the world. But you’ve got to be mindful of the risks. If rates take a nosedive or life throws a curveball and you need to move, you could be left with some financial ‘what-ifs.’

Here’s the pro tip: Prepare yourself. Locking into a fixed rate mortgage is a commitment, not unlike marriage, and there’s no ‘swipe left’ option here. Know your budget, understand your long-term goals, and talk to folks who’ve played this game before.

Customer Testimonials on 30 Year Fixed Rate Mortgage Rates

Real talk – nothing speaks volume like hearing from the horse’s mouth. Homeowners who’ve nabbed low rates are enjoying their financial freedom like a kid in a candy store. Their journeys with lenders have had more ups than downs, and they often look back at their decision as a financial slam dunk for their personal finances.

What Experts Are Saying About Future 30 Year Fixed Rate Mortgage Trends

Turning to the crystal ball, experts are chattering about future trends in 30 year fixed mortgage rates. With “what time is Trump’s arraignment” headlines potentially shaking things up, we’re reminded of the global stage’s influence on our humble abodes.

Economic forecasts, tinged with the wisdom of international economists, hint that today’s rates are as sweet as it gets. Sure, there could be a rate hike around the corner, but if you can lock in a low rate now, it might just be smarter than a fifth grader preparing for the spelling bee championship.

How to Plan for Potential Rate Changes

Speaking of spelling bee champs, let’s spell out some savvy financial moves. If you’re a paddle-your-own-canoe kind of person, strategize for future refinancing. Debate making those extra payments and arm yourself with tips from money management pros. They’re the financial equivalent of a Swiss army knife – full of useful advice for any scenario.

The Role of Government Programs in 30 Year Fixed Rate Mortgages

Now, don’t forget Uncle Sam’s role in all this! Government mortgage programs like FHA loans and VA loans offer alternatives with typically lower rates or different requirements. These can be life-savers, like a floatie in deep water.

And keep those ears perked for new proposals or legislation. Policy analysts are always stirring the pot on sustainable housing initiatives that make the American Dream more reachable and we don’t mean in the do it For state kind of way.

Conclusion: Making an Informed Choice on 30 Year Fixed Rate Mortgage Rates

In summing up this mortgage rate rollercoaster, it’s worth stressing the golden opportunities present in today’s historic lows. As you sail into the mortgage horizon, let expert recommendations be your North Star in navigating these waters.

And remember, innovative strategies are the name of the game for prospective homebuyers in 2024’s market. Whether it’s cashing in on guilt grief, channeling your inner Billy Dee williams cool, or engineering your financial future with the precision of a Rachel Bradshaw tune, it’s about making choices in harmony with the times.

Homeownership is still the American Dream, dressed in brick and mortar. Understanding current 30 year fixed rate mortgage trends is key to unlocking its door. So, go ahead, be the maestro of your financial symphony, and let’s make this historic low note in mortgage rates the beginning of your housing success story.

Exploring the Peaks and Valleys of 30 Year Fixed Rate Mortgage Rates

Did you know that, once upon a time, delving into the figures of 30 year fixed rate mortgage rates was almost as unpredictable as guessing “what time is Trump’s arraignment”? While we’ve seen historically low rates in recent times, which have many prospective homeowners clicking their heels, the mortgage landscape hasn’t always been this rosy. Rates have ridden a rollercoaster, influenced by economic shifts, policy changes, and global events, each leaving its unique mark on the financial canvas.

A Stroll Down Memory Lane

Jump back a few decades, and you’d have seen interest rates that would’ve given today’s buyers a case of the heebie-jeebies. Imagine locking in a rate that rivals your grandma’s age; that was the reality in the early ’80s when rates soared to double digits! Now, if you’re curious about 30 year fixed mortgage rates today, you’ll find figures that seem like a bargain-bin steal in comparison. It’s a head-scratcher, all right, considering that in the past, a mortgage could munch away at your finances like a starved Pac-Man.

From Sky-High to Historical Lows

Now, hold onto your hats, because here’s where it gets wild. The journey of 30 year fixed rate mortgage rates has been anything but dull. If today’s rates were a digital clock, they’d be blinking an unprecedented low time that would prompt a “Well, butter my biscuit!” from anyone who’s paid attention over the years. It’s fascinating to consider that securing a mortgage today could have you skipping to the bank with extra dough for those rainy-day funds or splurge-worthy vacations.

Sure, tracking mortgage rates might not stack up to the suspense of not knowing “what time is Trump’s arraignment,” but there’s an undeniable thrill in capturing a low rate that feels like winning the financial lottery. So, next time you’re pondering over those alluring 30 year fixed rate mortgage rates, remember you’re participating in a slice of history, hopefully on the sweeter side of the pie!

What is the interest rate on a 30 year fixed right now?

– Hunting for the scoop on the current interest rate for a 30-year fixed mortgage? Look no further, friend! While the rates are always in flux, snatching a real-time quote from a lender is your best bet to pin down the exact figure. Remember, though, the numbers don’t lie—even a slight uptick or downshift can make a big difference in your pocketbook.

What are 30 year mortgage rates today?

– “So, what’s the deal with 30-year mortgage rates today?” you ask. Well, you’ve hit the nail on the head—checking in with lenders is key because rates are like mood rings, changing color with market conditions. A quick chat with your local loan officer will give you the lowdown on today’s rates.

What is current fixed mortgage rate?

– When it comes to the current fixed mortgage rate, it’s sort of like asking about the weather—it can change at the drop of a hat! So, pop over to a lender’s site or give them a buzz; they’ll fill you in on the latest rates quicker than you can say “fixed-rate mortgage.”

Is 3.25 a good mortgage rate for 30 year?

– Oh, 3.25% for a 30-year? Flashback to pre-2020 when that was considered primo—like finding a four-leaf clover! As the whispers from March 27, 2020, go, 3.25% was close to the bottom of the barrel. So if you’re hanging onto a rate like that, give yourself a pat on the back!

Are mortgage rates expected to drop?

– Will mortgage rates take a nosedive anytime soon? Wouldn’t we all love a crystal ball for that one! Unfortunately, predicting interest rates is as tricky as a carnival guessing game. They could dip, but then again, they might not. Staying in the loop with financial forecasts is your best defense against rate rollercoasters.

Are interest rates going down in 2024?

– Peek into the future, and will interest rates be falling in 2024? That’s like trying to nail Jell-O to a wall; no one’s really sure! Economic conditions, policy changes, oh—they’ll all have their say. Might as well toss a coin or check in with expert analyses for a more educated guess!

Are 30-year mortgage rates dropping?

– Are we seeing 30-year mortgage rates on the descent? Well, it depends on when you peek. Like a yo-yo, rates can bob up and down with economic tides. Keeping an eye on trusted financial news could clue you in on whether it’s a dip or a dive.

What will mortgage rates be in 2024?

– The million-dollar question: What will mortgage rates look like in 2024? If we had a time machine, we’d be all over that answer. For now, though, it’s anyone’s game. Economic chatter and expert predictions might offer some breadcrumbs to follow.

What is the lowest 30-year mortgage rate ever?

– Curious about the rock-bottom, lowest ever 30-year mortgage rate? Once upon a not-so-distant past, rates flirted with historic lows. Although it’s a see-saw game, history had its magic moment with rates that had folks dancing in their living rooms.

Can you negotiate a better mortgage rate?

– Can you talk your way into a better mortgage rate? You bet your bottom dollar! Haggling with lenders can be like a trip to the farmers’ market—sometimes, you just gotta charm the socks off the seller. A strong credit score and a healthy down payment are your fresh produce in this bartering game.

What is best mortgage rate today?

– On the hunt for the best mortgage rate today? The early bird gets the worm, and the savvy shopper scores the sweet deal. Comparisons are your best friend—flit from lender to lender like a butterfly and see who’ll give you the nectar of low rates.

Is it better to have a longer fixed rate mortgage?

– The million-dollar question: is a longer fixed-rate mortgage the bee’s knees? Well, if stability is your jam and you’re not planning on moving faster than a hot potato, locking in a rate that won’t budge for years might just be your cup of tea.

Is FHA always 3.5% down?

– “Always” is a strong word, but when it comes to FHA loans, 3.5% down has become the talk of the town. There’s not much wiggle room there; it’s like saying pumpkin pie needs cinnamon—it’s just part of the recipe!

Will mortgage rates go down to 3 percent?

– Rumors of mortgage rates hitting the sweet spot of 3 percent again are like whispers of a hidden treasure—exciting, but no guarantees. Stay tuned, though; the market has its moods, and who knows, we might just hit the jackpot!

What if I lock in a rate and it goes down?

– Locked in a rate and then—bam!—it drops? Talk about a twist in the plot. Don’t sweat it, though; some lenders have a float-down option, sort of a “get out of jail free” card. But heads up, it often comes with ifs and buts, so read the fine print!