As we cast our eyes over the horizon of home financing, the 30-year mortgage rates today take center stage in the theater of real estate. They whisper stories of opportunity to intuitively savvy homebuyers and spell out a tale of attention-worthy trends for those poised to take part in the great American dream of homeownership. So, let’s delve into the crux of understanding, predicting, and navigating the 30-year mortgage rate now and in the months to come.

Understanding 30-Year Mortgage Rates Today: A Benchmark for Homebuyers

A 30-year fixed-rate mortgage is the most traditional way to finance a home. You lock in a rate and your payments stay constant over three decades, barring any changes in property taxes or insurance costs. But what are the 30-year mortgage rates today? Well, honey, just like your favorite old nickelodeon Shows, they’re a comfortable classic, but let’s see how they’re doing now.

Historical Context of 30-Year Fixed Mortgage Rates

Brief Recap of the Past Decade’s Rates

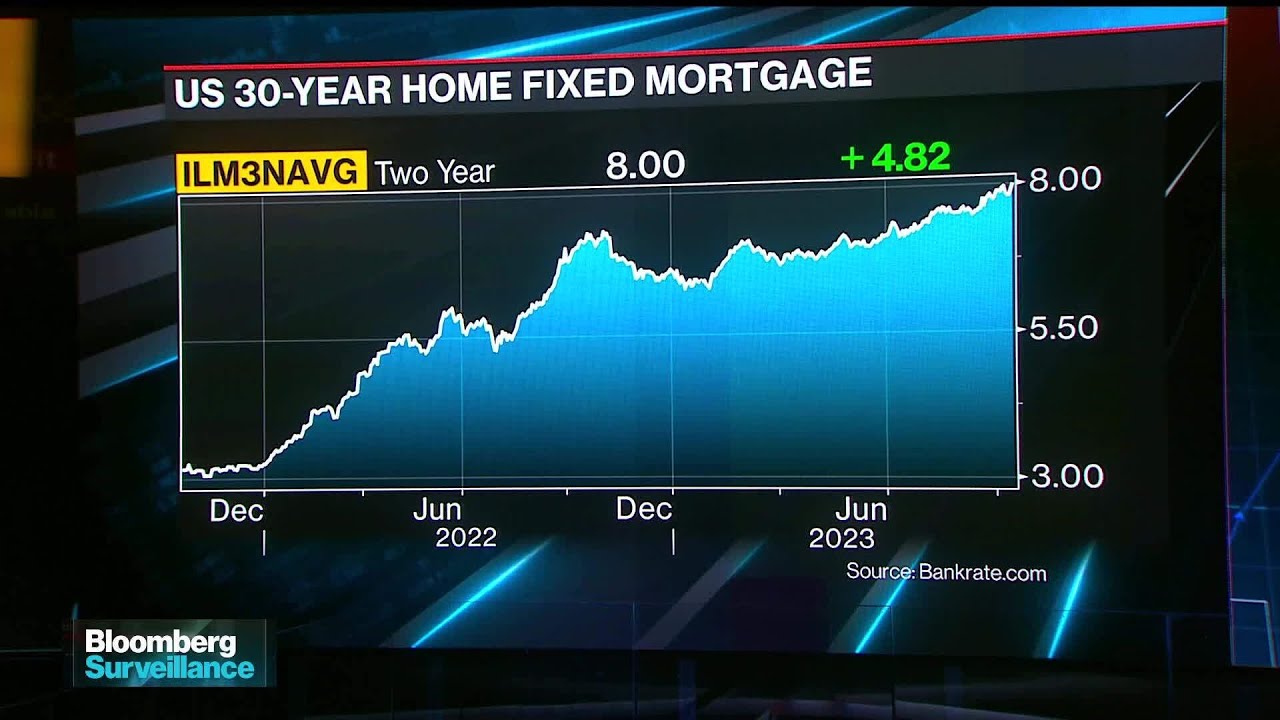

The past decade has been a roller coaster, with rates hitting historic lows and surprising us with unexpected spikes. Since June 2021, 30-year rates fluctuated between heart-fluttering lows around 3% to more robust figures pushing past the 6% boundary.

The Economic Events That Shaped Today’s Rates

Recessions, pandemics, and fiscal policies have played pivotal roles in the unfolding drama of mortgage rates. The financial policies that unfold to combat these events have significantly influenced the trajectory of these rates.

Comparing Past Peaks and Troughs

Every homeowner’s dream was the record low rates seen in the years following the 2008 financial crisis. Fast forward to 2023, the pandemic’s economical ripples saw lower-than-low rates, but the pendulum has swung upwards recently, making it clear that the landscape of 30-year mortgage rates is constantly evolving.

| **Date** | **30-Year Fixed Mortgage Rate** | **Notable Events** | **Forecast/Observations** |

|---|---|---|---|

| June 2021 | Varies (Historical Rate) | Benchmark historical period | Rates were lower compared with 2024 |

| February 12, 2024 | 6.55% | Lowest rate since this date | Decrease from peaks in late 2023 and early 2024 |

| March 8, 2024 | 6.55% | Current average rate, a seven-month low contrast to 6.10% before the new year | Rates are predicting a generally downward trend |

| October 2023 | 7.59% (15-year rate mentioned) | 15-year rates at their highest since 2000 | Reflects the peak of recent rate increases |

| Q1 2024 | 6.9% (Projected) | Mortgage Bankers Association (MBA) Mortgage Finance Forecast | Predicted gradual decline in rates starting in 2024 |

| Q4 2024 | 6.1% (Projected) | According to the February MBA Mortgage Finance Forecast | Forecasted to keep decreasing through the rest of the year |

| July 2024 | Projected rate cut | Financial market predictions | Expectancy of the first interest rate cut |

| Q1 2025 | Below 6% (Projected) | MBA forecasts rates to fall below 6% | Continued downward trend |

| End of 2025 | 3.74% (Financial Market Prediction) | Financial markets anticipate this rate by the end of 2025 | Significant expected decrease in mortgage rates |

The Current Landscape of 30-Year Mortgage Rates

Analysis of Today’s Economic Indicators

Today’s rates are like a flavorful stew with various ingredients—the Mortgage Bankers Association forecasts rates dipping by the end of the year to a savory 6.1%.

Federal Reserve Policies Impacting Current Rates

The Fed’s actions are akin to the maestro of an orchestra, where a single move can crescendo or diminish the music of the markets. The anticipation of interest rate cuts is like fans waiting for the release of Lizzie Broadway’s next performance; it’s expected to be a show that could sweeten the deal for prospective homeowners.

Role of Inflation and Employment Data

Inflation, sweetie, can either be a homeowner’s foe or an ally. When inflation rate whispers rise, they can lead the Fed to pull the reins on the economy. Employment numbers play in tandem, as solid job growth can sustain or even increase the rates.

Top Lenders Offering Competitive 30-Year Mortgage Rates Today

Wells Fargo: A Closer Look at their Rate Offerings

As solid as an old oak, Wells Fargo provides stable and competitive rates. Their 30-year mortgage rates today offer a mix of reliability and affordability, something that’s just as desirable as a Kayla Wallace feature in an indie film.

Chase Bank: Analysis of Mortgage Products and Services

Chase is like the Isaac Hempstead wright of banks—multifaceted and offering more than meets the eye. Their 30-year mortgage rates can be customized with various points and fee structures to fit different financial scenarios.

Quicken Loans: Comprehensive Review of Rates and Customer Service

Quicken Loans, quick and efficient, provides one of the best online mortgage experiences. They’ve used technology and top-notch customer service to present rates that are as enticing as catching up on old Nickelodeon shows for a dose of nostalgia.

Local Credit Unions: How They Compete with Bigger Banks

Don’t overlook the small but mighty credit unions. They often offer rates that are just as competitive, if not more so, than their giant counterparts. Like a hidden gem, they’re worth exploring for a sweet average 30-year mortgage rate today.

Factors Contributing to the Best 30-Year Mortgage Rates

The Influence of Credit Scores on Interest Rates

Let’s get real—your credit score is like your high school GPA; it opens doors or slams them shut. A stratospheric score can land you rates as alluring as Pornubes controversial appeal, while a lower one may leave you yearning for better.

Down Payment Requirements and Their Impact

Just like having the right gear before ascending a peak, the larger your down payment, the more solid your mortgage footing is.

Loan-to-Value Ratio: Understanding its Effect on Your Rate

Think of it this way: the more you invest in your own game upfront, the less risk the lenders shoulder, which can lead to better rates.

Expert Predictions for 30-Year Mortgage Rates in the Near Future

Insights from Top Financial Analysts

The soothsayers of finance, the economists, and your everyday analysts predict calmer seas ahead with rates potentially dipping below 6% by 2025.

Economic Forecasting and Rate Trends

Financial markets are buzzing with the same anticipation of a potential interest rate trim in July 2024, much like the buildup to a finale in your favorite series.

How Potential Homebuyers Can Prepare

This forecast is your cue to be vigilant—much like knights preparing for the next quest, potential homebuyers should sharpen their credit scores, save for down payments, and watch this space closely.

How to Lock in the Best 30-Year Mortgage Rates Today

Timing the Market: When to Act on Rates

Timing, dear homebuyer, can be just as crucial as the quality of a Lizze Broadway performance. Keep a hawk’s eye on rate fluctuations, and pounce when it hits your sweet spot.

The Importance of Rate Shopping and Comparisons

Don’t just settle, darling. Compare mortgage rates like you’re choosing your next binge-worthy show. Do your due diligence—rate shopping can save you thousands over the life of your loan.

Pre-approval Process: A Step Towards Securing a Low Rate

Suit up with a pre-approval letter as your shield against uncertainties. It demonstrates to sellers that you’re ready and able to buy, giving you the upper hand when negotiating your 30-year mortgage rates today.

Fixed vs. Adjustable: Deciphering the Right Choice for Today’s Market

Long-Term Benefits of a 30-Year Fixed Rate

Fixed rates are the classic vintage wine of mortgages—timeless and steady. They ensure consistent payments throughout the life of the loan, providing peace of mind in an ever-changing world.

Scenarios Where an Adjustable Rate Might Be Advantageous

Adjustable rates, however, could be your wildcard, playing out favorably if rates drop or if you plan to relocate before the fixed period ends.

Financial Planning Considerations for Both Options

Financial planning around mortgages is no less complex than plotting a Kiyosaki-esque investment strategy. Both options carry weight and should be considered carefully, in light of your long-term fiscal goals.

Regional Variations in 30-Year Mortgage Rates Across the U.S.

Comparing High-Cost vs. Low-Cost Regions

It’s not just about location, location, location, my dears. It’s also about rate variations. High-cost regions might cuff you with high rates, while other areas offer a veritable picnic basket of attractive rates.

States with the Most Favorable Mortgage Climates

Sunny states for 30-year mortgage rates today include areas with growing economies and stable job markets. They might just be the fertile soil for planting your homebuying roots.

How Local Economies Affect Mortgage Rates

The wax and wane of local economies can make a significant difference to mortgage rates, reminiscent of the tidal effects on the seashore. Sturdy economies often mean steadier rates, while a regional downturn can see them sway.

Innovative Mortgage Tools and Calculators for Today’s Homebuyers

Utilizing Online Resources to Estimate Monthly Payments

In an era where technology is as inseparable from our daily lives as breathing, use those smart mortgage calculators to your advantage. They’re the crystal ball to your future payments.

Software and Apps That Help in Interest Rate Comparisons

Harness the power of apps and software that liken to having a financial advisor in your pocket—they compare, deliver alerts, and could steer you towards locking in that golden average 30-year mortgage rate today.

Interactive Platforms for Real-Time Rate Tracking

Don’t underestimate interactive platforms offering real-time rate tracking, like a hawk soaring through the financial skies with its keen eyes set on movement below.

Real Estate Market Trends: Their Correlation with 30-Year Mortgage Rates

Housing Demand and Supply Dynamics

The tango between supply and demand in real estate has an intimate dance with mortgage rates. A shortage in housing supply with ongoing demand can cause rates to rise, while a surplus might see them relax.

Impact of New Construction on Mortgage Rates

New constructions add to the housing supply, and their proliferation can ease up the rates—like a laid-back Sunday morning easing into a bustling week.

Predicting Rate Movements Based on Real Estate Trends

Predicting rates based on real estate trends can be a tricky endeavor, yet understanding these dynamics is key. Anticipate and act wisely, like a grandmaster in a game of chess.

The Global Economy and Its Influence on 30-Year Mortgage Rates

International Events That Can Sway U.S. Rates

Global events, my friends, can ripple through economies, reaching U.S. shores and nudging those rates up or down. Think of it like distant thunder – you might not see it, but you’ll certainly feel its effects.

Exchange Rates and their Subtle Effects on Mortgages

The fluttering wings of currency exchange rates can gently move the rates, like a butterfly affecting the ecosystem around it.

Trade Agreements and Their Potential Impact on Home Loans

Trade agreements may seem far-off, but their influence can extend all the way to your mortgage rate. Keep an eye on them as you would a long-term investment.

Navigating the 30-Year Mortgage Rate Terrain: Tips for First-Time Buyers

Essential Advice for New Entrants to the Housing Market

To all the bright-eyed newcomers in the housing market: strap on your boots tight. It’s a journey. A solid credit history, a healthy down payment, and a hawk-like watch on rates will serve you well.

Programs and Assistance for First-Time Homebuyers

Research government and local assistance programs designed to help you gracefully enter the arena of homeownership.

Understanding the Long-Term Implications of a 30-Year Mortgage

A 30-year mortgage is more than a financial commitment – it’s a bond that will bloom and evolve over time, much like a lifelong relationship that requires dedication and understanding.

The Future of 30-Year Mortgage Rates: Innovations and Predictions

Technological Advances in the Mortgage Industry

Expect technology to revolutionize how we mortgage, from blockchain efficiency to AI-curated rate predictions. It’s a wave of innovation that’s as exciting as waiting for the next season of your favorite show.

Emerging Trends in Home Financing

Look out for alternative lending platforms and creative home financing that are breaking the traditional mold and crafting a new narrative in the world of 30-year mortgage rates today.

Educated Guesses on What the Next Decade Might Hold

As we gaze into the crystal ball, educated guesses hold whispers of potential rate stabilization, tech integrations in lending, and a more user-centric mortgage experience.

Making Informed Decisions in an Uncertain Market

The Role of Real-Time Data in Mortgage Rate Decisions

Real-time data empowers you with the precision of a surgeon, making informed decisions with up-to-the-minute accuracy in an uncertain market.

Balancing Risk and Reward in Today’s Economic Climate

Life, much like investing, is a game of risk and reward. Balance them with care and understanding—know when to hold steady and when to leap.

Strategies for Adapting to Volatile Interest Rate Environments

Like a chameleon adapting to changing colors, you too must be versatile, ready to pivot your strategies in response to the shifting tides of interest rates.

Final Thoughts: Navigating Today’s 30-Year Mortgage Rate Landscape

The journey through today’s 30-year mortgage rate landscape is much like a grand voyage at sea. It can be both exhilarating and daunting. As we summarize this expedition, remember that key insights such as the influence of economic events, credit scores, and global markets illuminate paths to the most valuable treasure—your home.

Remember, knowledge is power, dear homebuyer.

Armed with critical information, your journey towards acquiring that perfect mortgage rate should be navigated with confidence and acumen. It comes down to precise timing, thorough preparation, and the understanding that, in the world of mortgages, just like in life, the only constant is change. Stay sharp, stay informed, and may the winds of favorable rates set your sails towards the shores of your dream home.

Unveiling the Best 30-Year Mortgage Rates Today: Did You Know?

So, you’re hunting for the best 30-year mortgage rates today, huh? You might think mortgages are dryer than a desert, but boy, oh boy, have you got another thing coming! Let’s dive into some rip-roaring facts that’ll make you the most interesting person at your next dinner party.

Did you know that the concept of a 30-year mortgage only gained popularity after the Great Depression? Yup, before that, mortgages were a shot in the dark, often requiring a balloon payment that could burst your bubble real quick. When you’re eyeing up the 30 yr mortgage rates today, tip your hat to the creation of the FHA in 1934, which standardized the long-term mortgage to make homeownership more attainable. Imagine the sheer relief of not having to cough up the full house price after just five years!

Now, fast forward to the present day, when clicking your way to a mortgage is as easy as pie. A historical nugget for you: the first-ever online mortgage approval was given out quicker than you can say “Jack Robinson.” But, as quick as a rabbit, the internet has changed the game, making the process so slick that you can compare mortgage rates faster than brewing your morning coffee. Scouting the best 30 yr mortgage rates today has never been a smoother ride, thanks to technology.

Hold onto your hats, because here’s a head-scratcher—did you know our friends across the pond, those Brits and Europeans, typically favor shorter mortgage terms? They look at a 30-year commitment, and their jaws drop. Meanwhile, in the Land of Liberty, we embrace these longer terms like we do free refills at a diner—because more time can mean smaller payments, and who doesn’t love that?

Well, butter my biscuit, isn’t it fascinating how such a mundane topic as the best 30-year mortgage rates today can be peppered with titbits that are as tasty as grandma’s apple pie? So, the next time you’re knee-deep in discussions about these 30-year commitments, give ’em the old razzle-dazzle with these fun facts! Remember, whether you’re a rookie or a seasoned mortgage hunter, keeping tabs on the seemingly capricious ebb and flow of mortgage rates is crucial. After all, knowledge is power—and knowing just how far we’ve come could save you a pretty penny.

What is the average mortgage rate for 30 years right now?

Well, hang onto your hats, folks! The average mortgage rate for a 30-year fixed whopper, as of the latest buzz on March 8, 2024, is sitting pretty at 6.55%. It’s like a roller coaster, slightly less dizzying than the stomach-churning 7.59% peak we hit last October for the 15-year rates, but hey, we’re still riding higher than the cozy 6.10% we snuggled into right before ringing in the new year.

Are mortgage rates going down in 2024?

You betcha, mortgage rates have been yo-yoing, but the word on the street (and by street, I mean the Mortgage Bankers Association) is that rates are expected to gently slide down the scale, from a steep 6.9% early in 2024 to a more toe-tappable 6.1% by the last quarter. So, if you’re playing the waiting game, 2024 might just show you some love.

Are 30-year mortgage rates dropping?

Like a leaf slowly drifting to the ground, 30-year mortgage rates are taking their sweet time but are indeed expected to drop. With current figures already lower than the early February sizzle, we’re all keeping our fingers crossed for the fall to continue. Popcorn’s ready, folks; let’s watch this slow-motion drop together!

Will mortgage rates come down?

Seems like the winds of change are blowing, and they’re whispering “yes”! Mortgage rates are likely to shimmy on down with financial markets already placing their bets on a rate cut starting in July 2024. So roll up those sleeves, ’cause it looks like we’re heading for cooler mortgage rate waters.

Will mortgage rates ever be 3 again?

Ah, the good ol’ days of 3% mortgage rates—seems almost like a fairy tale now, doesn’t it? But, keep your chin up! With financial markets forecasting rates dipping to 3.74% by the end of 2025, that ‘once upon a time’ might just have a sequel. Never say never!

Who is offering the lowest mortgage rates right now?

Here’s the scoop: Who’s got the lowest mortgage rates is a bit like asking for the tastiest ice cream flavor—it can vary depending on where you’re at and what you’re after. But with rates predicted to sink, it’s a good time to shop around like you’re at a discount bonanza for the sweetest deal.

Will 2024 be a better time to buy a house?

Rolling out the crystal ball for 2024? Well, it’s looking like a potentially brighter time to buy a house, with mortgage rates showing signs of mellowing out. If you’re gathering your pennies, 2024 might just be your year to jump on the property ladder—just keep an eye on that forecast!

How low will mortgage rates go in 2025?

As we peek into 2025, it’s like we’ve hit the mortgage rate limbo—how low can they go? Word on the street is they could tango all the way down to 3.74% by year’s end. So, limber up, potential homebuyers; it’s time to see just how low those rates can bend!

Where will mortgage rates be in 2026?

Talking about 2026 mortgage rates is like predicting the weather—take a wild guess! But if the trend’s your friend, and we’ve seen them sliding down the slide, who’s to say the party won’t continue? Just be ready for anything, because, you know, life likes to throw curveballs.

What is the lowest rate ever for a 30-year mortgage?

Digging through the mortgage rate time capsule, the lowest rate ever for the ol’ 30-year fixed was an eye-popping, jaw-dropping 2.65% in December 2020. Can you believe it? That’s like unicorn-level rare!

What has been the lowest 30-year mortgage rate?

Oh, you’re tugging on my nostalgia strings now! The lowest-ever 30-year rate was a jaw-on-the-floor 2.65% back in the days of yore—December 2020 to be exact. Those were the days, huh?

What are the disadvantages of a 30-year mortgage?

Listen up, a 30-year mortgage can run into a few bumps in the road. First off, it’s a marathon—not a sprint—which means you’ll pay more interest over the long haul. Plus, with that longer term, your monthly payments are lower, but it’s like a slow ride on the interest carousel, where you don’t get off for a while.

Will mortgage rates go down in recession?

As certain as the sun rising in the east, generally, yeah, mortgage rates tend to play nice and go down during a recession—it’s like the one silver lining in a grey economy cloud. But, it’s not a guarantee, so don’t bet the bank on it!

Should I overpay my mortgage before interest rates rise?

Ah, the age-old question: to overpay or not to overpay. Well, if rates are lurking around the corner ready to jump, throwing some extra at your mortgage now could save you a pretty penny later. Just make sure it doesn’t pinch your wallet too hard in the short term.

What is the bank rate today?

The bank rate today? Well, that’s as variable as the flavors in an ice cream truck. With the constant ups and downs, you’d better check the latest financial forecasts or give your bank a ring-a-ding-ding for the most current rate. Stay frosty!