Loan-to-Value Ratio: The Foundation of Your Mortgage Understanding

When you’re gearing up to dive into the world of home buying or refinancing, there’s one metric that stands tall, casting a long shadow on your mortgage journey—Loan-to-Value Ratio (LTV). So what’s the scoop on LTV? Simply put, it’s a handy-dandy tool for comparing the chunk of change your mortgage is gobbling up against the appraised value of your property. Think of it as the financial compass guiding lenders through the jungle of risk.

Why does LTV grab the attention of the mortgage industry bigwigs, you ask? It’s all about the Benjamins. LTV is the yardstick measuring the risk a lender faces when they hand over that pot of gold; a high LTV signals a red flag that they might be dancing closer to the edge of a cliff than they’d like.

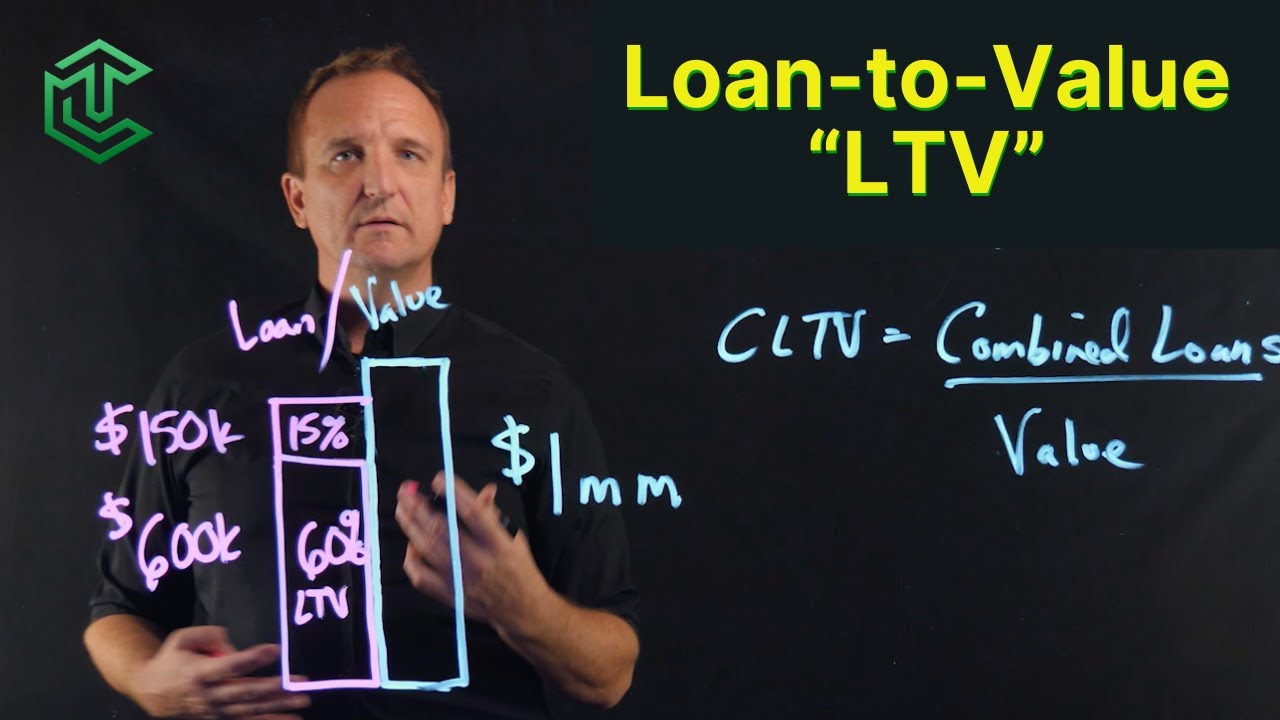

To get down to the nitty-gritty, here’s how you crunch those LTV numbers: take your current loan balance—it’s right there on your monthly statement or through your online account—and place it side by side with your home’s appraised value. Do a little dance, a simple division, and presto! Convert that result to a percentage, and you’ve got yourself an LTV ratio.

Unveiling the Loan-to-Value Ratio: Assessing Risk and Rates

The Loan-to-Value Ratio isn’t just a pretty face in the mortgage world; it’s the Swami, the crystal ball that lenders peer into when sussing out risk. The higher the LTV, the more the lenders might sweat, worried they’ll end up losing their shirt.

Now, bring in mortgage rates—the two are like peanut butter and jelly. A higher LTV often means a thicker spread of interest rates on your mortgage sandwich, and that can leave a sour taste in your wallet. Casting an eye on various case studies, it’s clear as day how that LTV figure is the magic number altering the interest rate landscape.

Consider Tim Riggins, a character known for taking risks on and off the football field. In real estate, his penchant for high LTVs might be as edgy as his demeanor, affecting his interest rates just like the plot twists in his storyline Tim Riggins.

| Aspect | Description |

|---|---|

| Definition | The LTV ratio measures the mortgage amount as a percentage of the appraised property value. |

| Calculation | LTV = (Mortgage Amount ÷ Appraised Property Value) × 100 |

| Importance in Mortgages | – Used by lenders to assess risk in lending. – Influences interest rates, loan terms, and necessity for private mortgage insurance (PMI). |

| PMI Relevance | – Required by most lenders for LTV ratios >80% to protect themselves in case of default. – Can increase overall borrowing costs for the borrower. |

| Ideal LTV Ratio | ≤80% to avoid PMI and secure better interest rates. |

| High LTV Consequences | – May lead to higher interest rates. – PMI typically required, increasing monthly costs. – Possible loan denial for LTVs >95%. |

| Benefits of Lower LTV | – Potentially lower interest rates and borrowing costs. – Higher chances of loan approval. – No need for private mortgage insurance. |

| Example Calculation | Home Value: $100,000 Mortgage Loan: $80,000 LTV: ($80,000 ÷ $100,000) × 100 = 80% |

| Reducing LTV | – Increase down payment. – Choose a less expensive property. – Pay down mortgage principal more quickly. |

| Current LTV Consideration | The LTV is not static; it can change over time as you pay down your mortgage or if the value of the property appreciates or depreciates. |

| Relevance to Refinancing | A lower LTV can result in better refinancing options, while a higher LTV may make refinancing more difficult or costly. |

| Impact on Equity | A lower LTV ratio indicates that the homeowner has more equity in the property, while a higher LTV suggests less equity. This equity can influence the ability to obtain home equity loans or lines of credit. |

Exploring Maximum Loan-to-Value Ratios: What Lenders Prefer

For a straight-as-an-arrow, safer-than-safe traditional mortgage, lenders tip their hats to an LTV of 80% or less. Cross that line, and you’re treading into high LTV territory where lenders start to get twitchy.

Let’s not forget those special loan programs out there—they have their own set of LTV desires, often allowing a little more wiggle room. And it’s not just in your neck of the woods; the international scene also has its take on what makes an ideal LTV, with variations as diverse as the cultures themselves.

Loan-to-Value Ratio Thresholds: The Path to Mortgage Insurance

Speaking of thresholds, if you waltz in with an LTV higher than 80%, lenders are gonna wanna strap a parachute onto that loan in the form of mortgage insurance. This is their safety harness, ensuring they won’t scrape their knees too badly if things go south.

Calculating those mortgage insurance costs can feel like doing a calculus problem backward, blindfolded. But it’s a necessary evil when dealing with a high LTV. Yet fear not! There are savvy strategies out there to wiggle out of those pesky insurance costs, and building up a more robust down payment is one such escape route.

The Loan-to-Value Ratio Effect on Refinancing Options

Refinancing can be as refreshing as a cool breeze on a hot summer day. But guess who’s there at the garden party? Our good old buddy LTV. A low LTV is like having an exclusive invite, giving you access to more palatable refinancing options and opening up the field to potentially pull out some cash.

Now let’s spin a yarn or two about real-life refinancing tales. Some homeowners hit the jackpot with a low LTV, slashing their rates and chuckling all the way to the bank. Others, saddled with a high LTV, find the door shut tighter than a jar of pickles.

Loan-to-Value Ratio and Equity Building: Strategies for Homeowners

Imagine LTV and home equity as dance partners, gliding across the ballroom floor. Build equity, and your LTV naturally dips, leading to a future where you can sidestep concerns like a female bodybuilder ducks a slow jab female bodybuilder.

So, what’s the secret sauce to knocking down your LTV? Throw extra dough at your principal like you’re making it rain at a birthday party. Or, if you fancy being a maestro of value, consider home improvements. Just make sure those are more like white dresses at a wedding than jeans at a black-tie event—they should add real value white Dresses.

Impact of Loan-to-Value Ratio on Real Estate Investments

Real estate investors, listen up! LTV matters to you too, like a well-oiled hinge on a treasure chest. It’s the scales of justice, balancing how much dough you’re borrowing against the property’s worth. Mastery of this balancing act means you could leverage more properties or protect your existing portfolio.

Advanced techniques like using LTV to strategize property flips, or securing additional equity lines for the rehab-savvy investor, are like knowing the secret handshake in the investment club.

Innovative Tools and Resources for Monitoring Your Loan-to-Value Ratio

Keeping an eagle eye on your LTV doesn’t mean poring over spreadsheets till the wee hours. Today’s savvy homeowners have digital arsenals at their disposal, with apps that track LTV tighter than a drum.

Don’t roll the dice on your property’s value; an occasional professional appraisal can lay down a royal flush on your LTV management strategy. And when should you reach out for a revaluation? When you smell a change in the wind—and have a hunch your property’s price tag has ballooned.

Loan-to-Value Ratio Variations in Different Economic Climates

Just like the weather, economic climates can make your LTV ratio as unpredictable as a game of Twister. Boo to recessions, which can bulge that LTV faster than a water balloon under a faucet. However, a housing market on the up-and-up? That’s like sunshine on your parade, trimming down your LTV and making mortgage lenders swoon.

Analysis of past bulls and bears shows that LTV patterns can be as cyclic as fashion trends—what goes around comes around.

Navigating Changes in Loan-to-Value Ratio Over the Loan Lifetime

Your mortgage’s lifespan can see more ups and downs than a roller coaster. And guess who’s riding shotgun? Mr. LTV. As you chip away at your loan, your LTV shrinks, too—except when the market hiccups, and suddenly, it’s puffed up again.

Anticipating these gyrations means you can tailor your mortgage strategy with military precision, keeping an eye out on whether prepayments will make your LTV behave or just kick the can down the road.

The Future of Loan-to-Value Ratios in the Dynamic Mortgage Landscape

As the mortgage terrain continues to morph, LTV remains firmly in the driver’s seat. With the winds of change blowing, we’re seeing predictive models for LTV that are so sharp, they could slice through uncertainty like a hot knife through butter.

Experts with crystal balls and fancy algorithms suggest that as LTV guidelines tighten or loosen their belts, they will continue to be a cornerstone in borrowing decisions.

Conclusion: Mastering Loan-to-Value Ratio for Financial Empowerment

Circle back to what we’ve unpacked, and you’ll be poised to make LTV your sidekick on the mortgage journey. Remember, you’ve got the reins—managing your LTV is akin to captaining your ship through calm and stormy seas alike.

Peering ahead, we see LTV’s role in mortgage decision-making continuing to evolve, adapting to the twists and turns like a chameleon on a color wheel. The bottom line is this: Understanding and mastering your Loan-to-Value Ratio equates to financial empowerment, leaving you sitting pretty on a throne of savvy homeownership.

Demystifying the Loan-to-Value Ratio

The ABCs of LTV: What’s the Buzz All About?

So, you’ve probably heard folks chattering about the “Loan-to-Value Ratio” or LTV, and you’re there scratching your head, wondering if it’s some secret code. Fear not, intrepid homebuyer! This nugget is your golden ticket. Simply put, the LTV ratio is the scale that lenders use to size up how much moolah they’re willing to lend you compared to the value of the property you’ve got your eye on.

Now, here’s a fun fact to chew on: Did you know that having an LTV that’s through the roof might make your lender a bit nervous, and could lead to a good ol’ chat with your friendly neighborhood Loan Officer? That’s right, higher the LTV, more the lender’s eyes widen!

Why It Should Matter to You

Hold your horses, partner! Before you ride into the sunset with that mortgage, understanding your LTV is like knowing the secret handshake at an exclusive club. Get this: if your LTV ratio is as high-flying as a kite, there’s a good chance you’ll be paying more than a penny for your thoughts. Lenders might look at you like you’re trying to buy a castle with a piggy bank and slap you with higher interest rates or, yikes, require you to snag What Is an insurance binder to keep things on the up and up.

Crank Up That Down Payment

Now, if you’re wise to the game, you’ll know that pumping up your down payment brings down that pesky LTV faster than a rodeo cowboy on a bucking bronco. More cash upfront? Lower LTV. Lower LTV? Sweeter the deal you’ll get on that loan term. Speaking of which, do you know how your “Loan Term” pops into this picture? You betcha, it’s the stretch you’ve got to pay back the dough. Nail that perfect harmony between LTV and loan term, and you’re dancing to a tune that’s music to the ears of lenders and your wallet.

Little House, Big Dreams

Imagine you’re dreaming smaller, say building a tiny house, where the stakes are as mini as the footprint. Guess what? LTV still matters! Whether it’s a tiny house or a towering mansion, that ratio’s got a hold on your financial future like a bear grip on a fresh catch. And don’t even think you can sneak by the eagle-eyed Loan servicer, who’s there to make sure your payments are slicker than a whistle.

Wrap-Up with Wisdom

Let’s bring it home now, folks! Understanding your Loan-to-Value Ratio isn’t just another hoop to jump through. It’s key to unlocking doors – quite literally! Keep that LTV as snug as a bug, and you’ll strut onto the mortgage scene ready to show ’em who’s boss. And remember, a Loan-to-Value Ratio that’s lower than low tide on a calm day could just be your ticket to the sweet life of affordable mortgage payments.

What is a good loan-to-value ratio?

Alrighty, let’s dive into the nitty-gritty of LTVs, shall we?

What does 80% LTV mean?

What is a good loan-to-value ratio?

Oh boy, a good loan-to-value (LTV) ratio typically falls at 80% or lower—it’s like hitting the sweet spot in the lending world. Lenders tend to smile a bit wider when they see these numbers because it usually means less risk for them.

How do you calculate your LTV?

What does 80% LTV mean?

So an 80% LTV? It’s pretty straightforward—it means you’re borrowing 80% of your property’s worth. The other 20%? That’s your skin in the game, your initial stake or down payment.

What does 60% LTV mean?

How do you calculate your LTV?

To calculate your LTV, grab your calculator and divide the amount you’re borrowing by the appraised value of the property, then multiply that by 100. Voila, you’ve got your percentage!

What is the average loan-to-value ratio in the US?

What does 60% LTV mean?

A 60% LTV—now we’re talking! This means you’re only borrowing 60% of your home’s value. You’re kind of a big deal with more equity, making you less of a risky business to lenders.

What is the cheapest loan-to-value ratio?

What is the average loan-to-value ratio in the US?

The average LTV ratio bounces around, but it’s often somewhere in the ballpark of 80%. Granted, this varies by area and other factors like market conditions.

Is 100% LTV bad?

What is the cheapest loan-to-value ratio?

Oh, the best deals? They’re usually snagged with the lowest LTV ratios. We’re talking 50% or even lower if you can swing it. This is when lenders might roll out the red carpet with killer rates.

Is 30% a good LTV?

Is 100% LTV bad?

A 100% LTV is like walking a tightrope—no safety net! This means you’ve borrowed the full value of your property, and while it’s not the end of the world, it’s definitely riskier.

Is 50% LTV good?

Is 30% a good LTV?

You betcha! A 30% LTV is fantastic. It’s like having a sturdy umbrella in a drizzle—you’re pretty much covered and looking good in the eyes of the lender.

What is the monthly payment on a $50000 HELOC?

Is 50% LTV good?

A 50% LTV? That’s half-way to owning your property outright, so yes, it’s generally considered a solid position, making most lenders tip their hats.

How much equity do I have if my house is paid off?

What is the monthly payment on a $50,000 HELOC?

Well, a $50,000 HELOC monthly payment can be as unpredictable as the weather. It hinges on the interest rate and your repayment plan. Some months it might just be the interest, other months more—if you want exact digits, best chat with your lender!

How much equity is in a home after 2 years?

How much equity do I have if my house is paid off?

If your house is paid off, well, do a victory dance because you’ve got 100% equity! That means the market value of your home is all yours for the taking.

Is 40% a good LTV?

How much equity is in a home after 2 years?

Equity after 2 years is like a mysterious treasure hunt—it all depends on how much you’ve paid off, how much your home’s value has appreciated or, fingers crossed, not depreciated.

What is a 40% loan to value mortgage?

Is 40% a good LTV?

Absolutely! A 40% LTV shows lenders you’re not messing around—you’ve got a fair chunk of equity, making you a lower risk and possibly scoring you a better deal.

Is 20% a good LTV?

What is a 40% loan to value mortgage?

A 40% loan-to-value mortgage means you’re only borrowing 40% of the property’s value, while you, the swanky homeowner, have the majority 60% equity from the get-go.

Is 30% a good LTV?

Is 20% a good LTV?

Is 20% LTV good?

You’re nailing it with a 20% LTV, it’s like being on solid ground. This is primo territory, potentially landing you some of the best interest rates out there.

Is 40% a good LTV?

What is an example of a 75% LTV?

For example, if you’re eyeing a home with a price tag of $300,000, and you’re getting a mortgage for $225,000, that’s a 75% LTV. You’ve just gotta come up with that remaining 25%, but hey, you’re three-quarters of the way there!