Deciphering the Loan Estimate: A Primer for Prospective Homebuyers

Understanding the Loan Estimate: The Foundation of Your Mortgage Journey

Alright folks, let’s get down to brass tacks. If there’s one document in the massive pile of paperwork that homebuying involves that you really need to wrap your head around, it’s the Loan Estimate. Imagine it’s the map you clutch on a cross-country trek; it’s that important.

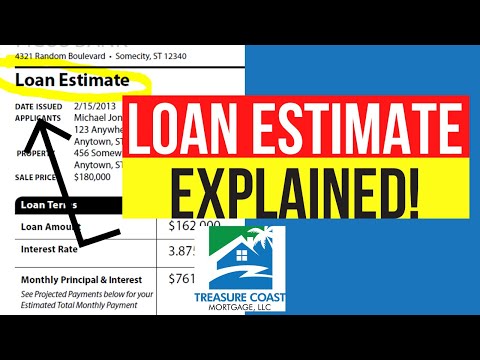

The Loan Estimate (LE) is the first genuine peek into the mortgage offers you can expect from lenders. It’s a three-pager that sizes up one lender against another, giving you the power to make a savvy decision. Plus, it’s the foundation upon which you can lay the bricks of your financial planning. Think of it as the key that unlocks the door to understanding your mortgage.

Anatomy of a Loan Estimate: Key Sections Explained

Let’s dissect that Loan Estimate, shall we? Each section is there to offer clarity and keep things transparent, so you’re not caught off guard later. It lays out the loan terms, projected payments, and those closing costs that can surprise the best of us. Don’t let the numbers and legal jargon intimidate you; we’ll go through it with a fine-tooth comb.

The Loan Estimate Breakdown: Navigating the Numbers

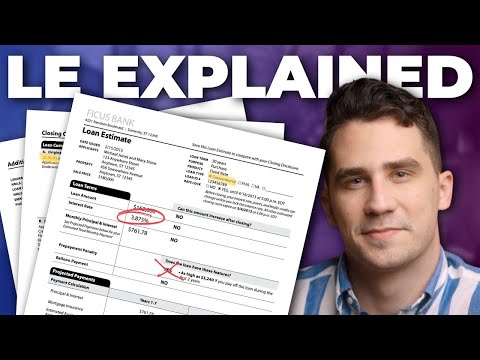

Loan Terms: Interest Rates, Balances, and Prepayment Penalties

Hop onto the ‘Loan Terms’ wagon and let’s talk turkey about interest rates, your loan balance over time, and those often glossed-over prepayment penalties. Here’s the skinny – getting a handle on whether you’re looking at a fixed-rate or an adjustable-rate loan can be as crucial as choosing the right home. They say the devil is in the details, and they’re not kidding.

Projected Payments: Plan Your Budget with Precision

The ‘Projected Payments’ section isn’t just there to make the document longer; it’s your crystal ball into the future of your finances. It gives you the low-down on your payment schedule and how your costs might rise due to changes in insurance or property taxes. Getting this right is like acing a test; it feels so good because you’re prepared for the curveballs life might throw at you.

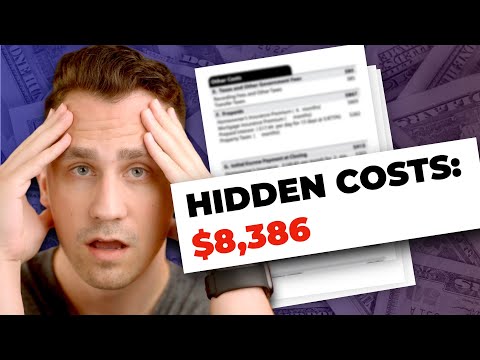

Costs at Closing: Understanding Closing Cost Details

Closing costs can be like a box of assorted chocolates – you never quite know what you’re going to get. The ‘Closing Cost Details’ section breaks down the bitter and the sweet of lender fees, third-party charges, and little extras that add up. But fear not; with a little homework, you can cut some of these costs down to size and sweeten the deal for yourself.

| **Loan Estimate Component** | **Description** | **Relevant Information** |

|---|---|---|

| Lender Information | Identifies the lender providing the Loan Estimate. | – |

| Borrower Information | Includes borrower’s name, Social Security number, and property address. | Address of the home you’re financing; Social Security number. |

| Loan Term | Duration of the loan (e.g., 30 years, 15 years). | – |

| Purpose | The purpose of the loan (e.g., purchase, refinance). | – |

| Loan Type | Specifies the type of loan product (e.g., fixed, adjustable). | – |

| Loan Amount | Total amount borrowed. | Loan amount requested. |

| Interest Rate | Proposed interest rate for the mortgage. | Estimated interest rate; may change daily. |

| Monthly Payment | Estimated monthly payment, including principal and interest. | – |

| Prepayment Penalty | Indicates if there is a penalty for early loan payoff. | Required by law to be disclosed. |

| Balloon Payment | Indicates if a large lump-sum payment is required at the end of the loan term. | – |

| Estimated Closing Costs | Summarizes all costs required to close the loan. | Must be within 10% of the amount shown on the LE by law. |

| Estimated Cash to Close | Total estimated cash needed for closing, including down payment. | – |

| Projected Payments | Breakdown of payment estimates over time, including any changes. | Information on how the interest rate and payments may change. |

| Estimated Taxes and Insurance | Monthly estimates for property taxes and homeowner’s insurance. | These are estimates; actual costs might differ. |

| Other Costs | Appraisal, title search, surveys, taxes, and other fees. | Any upfront credit report fee is typically the only permissible charge before issuing a Loan Estimate. |

| Total Interest Percentage (TIP) | Total amount of interest that you will pay over the loan term as a percentage of your loan amount. | – |

| Uses | Allows borrowers to compare different loan offers and ask the lender questions. | Use it to review terms and clarify anything that looks different from expectations. |

| Expiry | Loan Estimate expiration date. | Typically valid for 10 business days from issuance date. |

| Proceed | If borrower decides to move forward, lender will request additional financial information. | Receipt of Loan Estimate does not equal loan approval or denial. |

| Accuracy of Estimate | Aim to be as accurate as possible, with a legal requirement to be within 10% of final costs. | At Homebuyer, estimates are aimed to be close to 100% accurate; remember numbers are not exact upfront. |

Behind the Numbers: Analyzing the Impacts of Your Loan Estimate

Calculating the Long-Term Costs: Interest Rates and APR

Diving deep into the numbers, we find the interest rate, snug alongside the Annual Percentage Rate (APR). You might wonder why two rate types are trying to grab your attention. Simply put, the APR pulls back the curtain to show the real cost of the loan, considering fees and other costs. Understanding this difference can save you a bundle over the long haul.

Comparing Loan Estimates: A Strategic Approach

Now you’re armed with multiple Loan Estimates, looking sharper than 007 in a tuxedo. It’s time to play them against each other. Look beyond just the monthly payment and interest rate; dig into lender fees and the nitty-gritty of loan features. Always remember: knowledge is power, and this is your power play.

Additional Considerations: Beyond the Basic Loan Estimate

Added Fees and Riders: The Fine Print that Affects Your Wallet

When it’s time to talk about added fees and riders, you’ll need to squint at the fine print that might not jump out on the first read. Do yourself a favor and prod lenders about these sneaky costs. It’s the financial equivalent of making sure there’s no monster under the bed – just peace of mind.

The Loan Estimate in Context: Market Trends and Rate Locks

Understanding the Loan Estimate isn’t just about the here and now; it’s about how the winds of the market can sway your mortgage deal. That’s where the concept of rate locks slides into the picture. They can be your best friend in a volatile market, making sure your good deal doesn’t fly south before you close.

The Loan Estimate and Government Regulations: Staying Informed

Understanding Your Rights Under the TRID Rule

Have you heard of the TRID rule? It’s a bit like the financial world’s Constitution – setting the stage for transparency and borrower empowerment. Don’t glaze over; this stuff is important. It champions your right to receive clear and understandable Loan Estimates. Square up to this info to make sure you’re getting the fairest shake.

The Loan Estimate and Consumer Protections: Know Your Legal Safeguards

There’s a clutch of consumer protection laws out there, guarding your back when it comes to Loan Estimates. Brush up on these regulations, because when it comes to mortgages, you’re not just shopping for homes; you’re shopping for justice, fairness, and a square deal.

From Loan Estimate to Closing: The Journey of Home Financing

The Loan Estimate as a Negotiation Tool: Leveraging Your Knowledge

Breaking news! Your Loan Estimate is more than just a piece of paper; it’s a bona fide negotiation tool. Like a sharp-witted lawyer in the courtroom, find ways to use the intricacies of the LE to chisel down your terms. Real-world stories abound where knowing the nooks and crannies of an LE has turned the tables.

Transitioning from the Loan Estimate to the Closing Disclosure

Remember that the Loan Estimate is just the opener to this show. The big act is the Closing Disclosure, the grand finale of your home financing journey. Like matching socks, you want your Loan Estimate and Closing Disclosure to look pretty similar, give or take. Differences here could mean surprises there, and not the good kind.

Empowering Your Homebuying Experience with a Clear Loan Estimate

Common Mistakes and How to Avoid Them: Insights from Industry Experts

Grab a chair and let’s talk turkey about the common slip-ups even the smartest homebuyers make; not comparing enough LEs or glossing over the fine print can lead to a real pickle. But armed with insider know-how, you can steer clear of these pitfalls, turning your LE from a riddle into a roadmap.

The Future of Loan Estimates: Emerging Trends and Technologies

So, what’s on the horizon for LEs? Will artificial intelligence give us a history rewrite? Industry whispers say ‘yes’. Emerging trends and tech are set to make Loan Estimates sleeker, more intuitive, and friendlier for the homebuyer of tomorrow. It’s a brave new world, packed with possibilities.

Conclusion: Mastering Loan Estimates for Homebuying Success

Recap: The Critical Role of Loan Estimates in Homebuying

Let’s take a moment for a recap, shall we? The Loan Estimate isn’t just fancy paperwork; it’s a homebuyer’s first love in the world of mortgage lingo. It shapes your understanding, guides your decisions, and protects your wallet.

The Proactive Homebuyer: Next Steps After Gaining Loan Estimate Proficiency

Now that you’re schooled in the art of the Loan Estimate, you’re ready to face the real estate coliseum like a gladiator. Keep up the good fight with ongoing education and engagement in personal finance and real estate matters. The world is your oyster, and your Loan Estimate is the pearl of the homebuying process. Stay sharp, stay savvy, and happy house hunting!

Demystifying the Loan Estimate for Homebuyers

Buying a home is like hopping on a rollercoaster, complete with ups, downs, and that woozy feeling when tackling financial jargon. But don’t fret! We’ve brewed up a blend of fun trivia and killer facts that’ll perk you up like a cup of Joffrey’s coffee on a Monday morning. Let’s dive into the world of Loan Estimates, shall we?

A Quick Credit Pep Talk

Before we chat about Loan Estimates, here’s a nugget for you: lenders love seeing a credit score that’s fit and trims—a bit like dreaming of a tight butt without hitting the gym. A top-notch score can get you stellar loan terms. Wondering if you can boost credit score overnight like a fairy godmother waving her wand? While it’s not instant magic, there are ways to give your credit that extra pump.

What’s This Loan Estimate You Speak Of?

So, onto the main act: the Loan Estimate. It’s your financial story’s prologue—the one where you learn exactly what costs you’re signing up for with your mortgage. It breaks down interest rates, payments, and all the nitty-gritty details. Think of it as a behind-the-scenes look at your loan terms before you say “I do.”

Uncover the Secrets within Pages

Imagine if every poppy in a field had its unique vibe—well, every page of your Loan Estimate does too! Page one spotlights the basics like loan terms, projected payments, and closing costs. Let’s flip to page two, where you’ll find an itemized list of all the cash you’ll shell out. Now, land on page three, where you can compare offers, mull over the Costs at Closing, and determine if you’re getting a good deal. It’s like a treasure map, only instead of “X marks the spot, it’s numbers, lots of numbers.

Decoding the Lingo

Tackling a Loan Estimate can feel like deciphering an alien dialect. Terms like “prepayment penalty” or “balloon payment” might have you scratching your head. And hey, what about “lien”? Sounds scary, doesn’t it, like a jungle beast? Relax, it’s just a legal term for the lender’s right to keep possession of property belonging to another person until a debt owed by that person is discharged. But remember, knowing the lingo is the key to being a savvy borrower.

The Plot Twist: Can It Change?

Well, here’s a twist: some parts of your Loan Estimate can change before you reach the grand finale—the closing day. However, others are locked tighter than Fort Knox. Remember that adjustments can occur, and if they do, you might need a Loan Modification. It’s akin to rewriting a chapter of your book to get a happier ending with your mortgage terms.

Fun Fact Time!

Let’s sprinkle some trivia into the mix. Did you know that the concept of loan estimates hasn’t been around since the Stone Age? The journey from the quill-and-ink lending contracts of yore to the Loan Estimates today would make a fascinating chapter in the artificial intelligence history books. From handshakes over verbal agreements to smart systems prepping your paperwork, lending’s come a long way, baby!

In Closing: The More You Know…

Becoming a homeowner is a huge deal. It’s like a dance, and you don’t want to step on any toes. A Loan Estimate is the lead partner guiding you through the complex moves of mortgages. Now, with these gems of knowledge up your sleeve, you’ll be stepping with confidence. Remember, the more you know, the smoother the home-buying waltz!

So, don’t let the Loan Estimate scare the living daylights outta you. Embrace it like your favorite dance move, and you’ll own that dance floor—I mean, your new home—in no time. Keep those trivia bits and facts in your back pocket, and you’ll shine brighter than a diamond in a rhinestone world. Happy house hunting!

How many days is a loan estimate good for?

– A loan estimate isn’t set in stone, but it’s got legs for at least 10 calendar days. That’s how long the interest rate is locked in, giving you a bit of wiggle room to decide if that mortgage fits like a glove or if you should keep window-shopping.

How accurate are mortgage loan estimates?

– While mortgage loan estimates aren’t bang-on-the-money exact, they’re usually within shooting distance. Think of them as a ballpark figure—not as precise as a laser-measured blueprint, but close enough to give you a solid sense of what you’ll be shelling out.

What is in a loan estimate?

– Think of a loan estimate as your financial roadmap—it lays out the nuts and bolts of your loan, including the interest rate, monthly payment, and a breakdown of closing costs. It’s like a treasure map for your mortgage, minus the “X” marking the spot.

Are loan estimates free?

– You bet your bottom dollar loan estimates are free! It’s like a sneak peek at what you’ll be paying for your dream home before you dive into the deep end of the mortgage pool.

How soon can you close after loan estimate?

– Once you’ve got your loan estimate, hang tight—it’s like the starter’s pistol in a race. You’ll need at least seven business days after receiving it to rev your engines, but the actual closing can happen as soon as the lender gives the green light, typically a few weeks to a month later.

What is the 3 7 3 rule in mortgage?

– The 3-7-3 rule in mortgages is like a lender’s recipe—they’ve got 3 days after your application to serve up a loan estimate, a 7-day waiting period after you get it before you can cozy up to the closing table, and then they’ve got to dish out the closing disclosure 3 days before the big signing ceremony.

What is the 7 day rule for loan estimate?

– The 7-day rule for loan estimates is like a financial breather—it means after getting your loan estimate, there’s a week-long waiting period before you can tip-toe down the aisle to the closing table.

Does a loan estimate mean you are approved?

– Hold your horses—getting a loan estimate doesn’t mean you’re in the clear just yet. It’s more like getting a first date; you’re in the running, but it’s not the same as a walk down the aisle (a.k.a. full approval).

What happens after receiving loan estimate?

– After you get a loan estimate, it’s not just sitting pretty; you’ve got homework. This is when you review the costs, terms, and fine print—think of it as checking under the hood before you take the car off the lot.

Why is my loan estimate so high?

– If your loan estimate seems sky-high, don’t sweat it too much. It might be because the lender’s being extra cautious, padding the numbers to cover their bases—the same way you might order a size up just to be sure something fits.

Who prepares the loan estimate?

– Who whips up your loan estimate? That’d be your lender, acting like a financial chef mixing all the ingredients of your loan details into one dish to give you the full flavor of what you’re diving into.

What fees Cannot change on a loan estimate?

– In the mortgage world, some fees on your loan estimate are as locked in as a bear hug—things like your lender’s origination charge. They can’t change unless there’s a major switcheroo in your loan deets.

Can you negotiate a loan estimate?

– Can you negotiate a loan estimate? Well, sorta. It’s not as easy as haggling at a flea market, but there’s room to wiggle on some of the costs. Be bold—ask the lender if they can sweeten the deal!

What happens if lender does not provide loan estimate?

– If a lender drags their feet and doesn’t hand over a loan estimate, it’s a no-go for your home buying journey. They’ve gotta give it within three business days of your application; if they don’t, they might be taking a walk down a regulatory hall of shame.

How many loan estimates should I get?

– You’re not stuck with the first loan estimate that lands in your lap. It’s wise to shop around and scoop up at least three to five estimates. That way, you can compare apples to apples and snag the best deal for your dream home.

What is the 7 day rule for loan estimate?

– The 7-day rule is like a mandatory cool-off period—it means you’ve got a week to chew over your loan estimate before the mortgage wheels can start turning towards closing.

How long is a lender quote good for?

– When a lender quotes you terms for your mortgage, it’s a bit like catching lightning in a bottle—usually good for 10 to 30 days. But keep in mind, rates can be as fickle as the weather, so a locked rate has a shorter shelf life.

What is the 3 day rule for Trid?

– The 3-day rule for TRID is like a final countdown—kids, cover your ears—it requires lenders to give you the closing disclosure three business days before you sign on the dotted line. It’s your last look before you say “I do” to that mortgage.

What is the 3 day rule for respa?

– Same tune, different lyrics: the 3-day rule for RESPA sings along to the same beat as TRID—saying “Stop! Look and listen!” before you finalize your mortgage, making sure you get that closing disclosure with time to spare.