Unlocking the Fundamentals of dscr Debt Service

When you’re swimming in the deep end of the mortgage pool, staying afloat means understanding every ripple and wave. One such ripple is the Debt Service Coverage Ratio (DSCR), a financial metric as crucial to lenders and investors as a lighthouse is to sailors. So, what’s the big deal with dscr debt service?

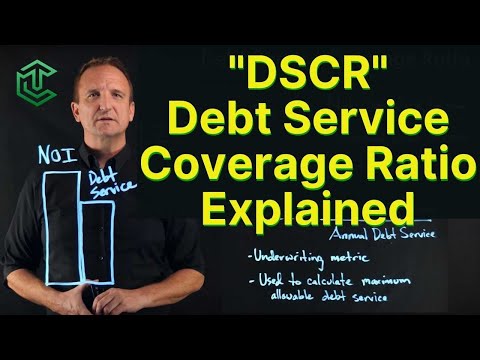

DSCR measures a property’s ability to cover its debt obligations with its income. Think of it as the financial health check-up for your investments. A DSCR of more than 1 means your property’s income can comfortably give your debts a well-deserved smackdown, paying them off without breaking a sweat. But if it’s less than 1, that’s when the alarm bells start ringing. It’s like trying to fill a leaking bucket — eventually, you’ll run out of water.

To get into the nitty-gritty, calculating DSCR involves dividing the property’s net operating income by its total debt service. Imagine you’ve got a net operating income of $120,000 and a total debt service of $100,000 for the year. Simple math tells us your DSCR is a solid 1.2. Not too shabby, right? It means your property is earning enough guacamole to spread on your debt obligations and have a little left over for a toast.

Expert Strategies to Optimize Your Debt Coverage

Roll up your sleeves; it’s time to buff up your dscr debt service to a dazzling shine. We’re talking practical, sleeves-rolled-up approaches here. For starters, enhance your property’s income. This could be as simple as increasing rent where the market Allows or adding revenue streams like laundry facilities or parking fees. It’s like squeezing every last drop of juice from an orange; you want every bit of income you can get.

Now, let’s take a page from the business big leagues. Companies with stellar dscr figures didn’t get there by accident. Some introduced new services that bumped up their income stream, while others renegotiated their debt terms for lower interest rates. In the wild world of mortgages, these tactics are akin to finding an oasis in a desert.

Improved debt coverage doesn’t just look good on paper; it’s your golden ticket to more favorable loan conditions. Lenders love a safe bet, and a healthy dscr says you’re as reliable as they come. Think of it as the financial equivalent of a four-leaf clover.

| Descriptor | Explanation | General Guideline |

| Total Debt Service (TDS) | The total cash needed to cover all debt obligations for the year. | Should not exceed 40% of your income. |

| Components of Total Debt Service | Interest, principal, sinking fund, and lease payments. | Included in the calculations for TDS. |

| DSCR (Debt Service Coverage Ratio) | A measure of a property’s ability to cover its debt obligations. | A DSCR over 1 indicates adequate coverage. |

| Interpretation of DSCR | – DSCR of 1.2: can cover debt 1.2 times over. | – DSCR < 1 suggests insufficient coverage. |

| – DSCR < 1: Debt obligations exceed income. | ||

| Importance of DSCR to Lenders | High DSCR lowers the risk for lenders. | A higher ratio is preferred by lenders. |

| Debt Service on Balance Sheet | Includes short-term debt and current part of long-term debt. | Reflected in the current liabilities. |

| Gross Debt Service (GDS) | Portion of income spent on housing expenses. | Should not exceed 30% of your income. |

| TDS vs GDS | TDS includes housing expenses and other debt payments; | TDS is more encompassing than GDS. |

| GDS only includes housing expenses. | ||

| Impact of Debt Obligations | The need to service debt affects financial flexibility. | Higher obligations may restrict operations. |

The Inside Track on dscr Debt Service for Property Investments

In the real estate realm, dscr debt service is as crucial to success as prime location. Here, dscr operates with its own set of rules. For instance, income is often backed by long-term leases, which adds a comforting level of predictability to the equation.

Real estate investment moguls like Blackstone and Brookfield Asset Management have this down to an art. They keep their dscr levels as trim as an athlete in the prime of their career, ensuring they can withstand market downturns without stumbling. These firms treat their dscr figures as sacred, making calculated maneuvers to optimize income and manage debts with the precision of a chess grandmaster.

But the real estate market is a fickle beast, and trends can tip the scales of dscr quicker than you can say “housing bubble.” A sudden spike in interest rates, for instance, can crank up your debt service costs, while a cooling market might dampen your income streams. Mastering the dscr here requires a vigilant eye and a hand steady enough to navigate through the storms.

Navigating dscr in Difficult Economic Climates

It’s no secret that when the economy sneezes, the property market catches a cold. In tough times, a company’s dscr can get as shaky as a leaf in a hurricane. But it’s not all doom and gloom. Some economic smartypants seamlessly adjust their sails to the gale-force winds by doing things like refinancing debt or tightening operational belts.

For example, during the 2008 financial crisis, resilient companies that had focused on maintaining strong dscr figures before the crash were markedly more stable. Their secret sauce was a combination of conservative debt management and a laser focus on sustaining income, proving that when it comes to dscr debt service, the best offense is a solid defense.

Comparatively, during times of economic bloom, companies with healthy dscr levels ride the wave of prosperity with the grace of seasoned surfers, leveraging their financial standing to nab prime investment opportunities. They’re like the guests who arrive early to a buffet: they get the first pick of the feast.

Advanced dscr Debt Service Techniques for the Seasoned Investor

For those who have trodden the investment pathway for miles, there are shrewd dscr manipulation tactics as inventive as a master magician’s sleight of hand. These are the strategies whispered about in the corridors of investment summits, where seasoned players sharpen their edge.

Put on your wizard hat and consider, for example, taking a surgical approach to debt restructuring. This is not about hacking away at debt with a broadsword but rather using the scalpel to carve out better terms, extend loan periods, or even consolidate debts to snag a more favorable rate.

The likes of financial gurus such as Ray Dalio stress the importance of a robust dscr in making informed investment decisions. It’s not just about the numbers, but reading between the lines; identifying opportunities where an improved dscr can unlock higher investment echelons.

Analyzing industry data could reveal patterns that the untrained eye might miss. It’s like uncovering a hidden treasure map where X marks the spot for successful dscr management. This could be the deciding factor between a meager return and a triumph.

Conclusion: Mastering dscr Debt Service for Long-Term Success

Well, folks, the secrets of the dscr debt service are out of the bag. This metric isn’t just a number cruncher’s daydream—it’s the bedrock of mortgage mastery. From the basic understanding of its workings to the complex strategies deployed by the big fish in the property pond, dscr is the thread that weaves through the tapestry of investment success.

Whether you’re braving the unruly seas of the economic climate or fine-tuning your debt management strategies, remember that in the grand scheme of things, a robust dscr is your financial compass. It can point you towards safe harbors or warn you of impending storms.

So go ahead, embrace these strategies and sharpen your skills. With dscr debt service mastery, you’re not just surviving the mortgage landscape; you’re thriving in it, building a fortress of financial well-being that even market fluctuations can’t penetrate. Your future self will thank you – and perhaps throw a parade in your honor through the streets of Financial Successville.

Unlocking the Mysteries of DSCR Debt Service

When it comes to mastering DSCR debt service, you’re not just crunching numbers—you’re embarking on a financial adventure. Get ready to dive into the world of debt service coverage ratio and discover secrets that are more intriguing than figuring out why you’d ever sleep With step mom!

A Homebuyer’s BFF: DSCR Demystified

Now, if you’re knee-deep in the How To buy a home process, you’ve likely heard of DSCR. In simple terms, it’s the measure of cash flow available to pay current debt obligations. Think of it as the trusty sidekick for lenders—it helps them to suss out if your pockets are deep enough to handle the mortgage without breaking a sweat.

The Scoop on Net Operating Income

Let’s gab about Net Operating Income (NOI), shall we? NOI is to DSCR what peanut butter is to jelly—a perfect match. But remember, to get an accurate NOI, every asset needs an Assessed definition. It goes beyond the market value, looking at the income potential and the expenses. And, yep, that includes that old depreciating jalopy—because things that depreciate are like a backwards race—they’re losing value as they chug along the fiscal track.

DSCR and the Art of Financial Surveys

Wanna define survey in DSCR terms? It’s like a treasure map for lenders, except instead of ‘X’ marking the spot, it’s a financial questionnaire that leads to the promised land of loan approval. Surveys can be about as fun as a trip to the dentist, but they’re key to ensuring everyone is on the same financial page before diving into a loan.

Wire Fraud Alert!

When dealing with DSCR debt service, talking What Is wire fraud isn’t just Debbie Downer talk—it’s a real threat, folks. It’s like the boogeyman of the financial world, snatching your hard-earned cash during transactions. So, keep your peepers peeled and stay vigilant, because wire fraud walks quietly but carries a big stick.

The Fashionable Financier

Ever thought managing DSCR debt service could be as on-trend as Sandals For Women Walmart? Well, think again! Keeping a close watch on your debt service is about as vital as finding that perfect pair of comfy yet chic sandals for a summertime stroll—both aid in your journey to happiness, albeit in very different ways.

When Life Collides with Debt

Navigating DSCR debt service can sometimes feel like you’re in need of “gerber collision & glass”. Why? Because just when you think you’ve got your finances ‘auto’-piloted, life can crash into your best-laid plans, leaving you in need of some serious repairs. The trick is to not just look at your current ability to pay, but to buckle up for future bumps in the road, too.

Remember, whether you’re trying to grasp the ins and outs of DSCR debt service for your own piece of real estate heaven, or just to sound super smart at parties, these tips and trivia will have you covered. Who knows? Conquering your DSCR could become your next favorite hobby, right up there with scouting for deals at Walmart or avoiding dubious late-night internet searches. Happy financial adventuring!

What is total debt service in DSCR?

What is total debt service in DSCR?

Hold your horses! Before diving into the nitty-gritty of DSCR, let’s clear up what total debt service is. In the world of DSCR, it’s all about the cash that’s needed to stay on top of your current debt obligations—that’s the interest, principal, you know, the whole shebang that you’ve gotta pay over the next year. We’re talking short-term debt and the quick slice of long-term debt that’s coming due. Think of it as your debt’s dinner bill that needs settling within the year.

What is a 1.2 debt service coverage ratio?

What is a 1.2 debt service coverage ratio?

A 1.2 debt service coverage ratio? Now, that’s what you call a bit of breathing room! It means a property’s income isn’t just skating by—it’s got enough dough to cover its total debt service 1.2 times over for the year. Assuming those debts don’t grow like a weed, it’s a comfortable cushion that tells lenders, “Yep, this one can handle the heat!”

What is included in debt service?

What is included in debt service?

When we say debt service, we’re opening Pandora’s box of all cash that’s due for debts. This isn’t just your average Joe’s loan payments; it includes interest, principal payments, Party A promising to pay Party B, and yes, even those lease payments that can’t be forgotten. Whether it’s for bonds, bootstrapping businesses with term loans, or that nudge-nudge working capital—debt service covers the whole enchilada.

What is a good debt to service ratio?

What is a good debt to service ratio?

Whew! A good debt service ratio is like a comfy blanket—it’s snug but not too tight. Generally, it’s a good rule of thumb to keep your Gross Debt Service (GDS) below 30% of your income, and your Total Debt Service (TDS) under 40%. That way, you’re not drowning in debt, and you’ve still got room to juggle life’s curveballs.

How do you calculate debt service?

How do you calculate debt service?

Alrighty, let’s roll up our sleeves and crunch some numbers! To calculate debt service, add up all the minimum payments you’ve got for the coming year—your interest, principal, the obligatory sinking funds, and lease payments. It’s time to get friendly with your calculator because you’ll tally every penny that’s dedicated to extinguishing those debts!

Is total debt service the same as total liabilities?

Is total debt service the same as total liabilities?

Oh, not so fast—total debt service and total liabilities are two different beasts. Total debt service is laser-focused on the cash you need to pay off debt within the year, while total liabilities are the big picture—all the debts and obligations, both short-term and long-term, that you’re on the hook for. So, think of total debt service as a snapshot, and total liabilities as your whole photo album.

Is 2.25 a good debt service ratio?

Is 2.25 a good debt service ratio?

Wowza, a 2.25 debt service ratio? That’s not just good, it’s like having your cake and eating it too! It means your income can cover your debt payments twice over, with a cherry on top. It’s music to lenders’ ears and a neon sign that you’re managing your debts like a pro.

What does a DSCR of 1.2 mean?

What does a DSCR of 1.2 mean?

A DSCR of 1.2 is like having a life vest while swimming—you’re comfortably afloat. It says loud and clear that for every buck of debt you have, you bring in $1.20 in income to cover it. Lenders give a thumbs up because it shows you’re more than making ends meet without breaking a sweat.

Can you get a DSCR loan with no money down?

Can you get a DSCR loan with no money down?

Hmm, a DSCR loan with no money down is like finding a unicorn—it’s a rare find! Most lenders want some skin in the game and often require a down payment, proving your commitment to the investment. Yet, in the world of creative financing, anything’s possible—if you can convince a lender you’re good for it. Good luck with that!

What is a good DSCR for rental property?

What is a good DSCR for rental property?

For rental properties, a good DSCR hovers around 1.25 to 1.30, but hey, the more, the merrier! This sweet spot tells lenders you’re not just squeaking by; you’ve got extra cheese for the unexpected costs that love to pop up when you’re a landlord.

Does DSCR include taxes and insurance?

Does DSCR include taxes and insurance?

You betcha, DSCR includes taxes and insurance. These aren’t your run-of-the-mill expenses; they’re part of the operating costs that you have to cover before you can say you’ve got enough to pay down your debt. So, don’t leave ’em out, or your calculations will go sideways!

What is minimum DSCR?

What is minimum DSCR?

The minimum DSCR is like the limbo stick at a dance party—how low can you go before it’s a no-go? Lenders typically set the bar at 1, a.k.a. break-even, where your income and debt service are playing tug-o-war at equal strength. But here’s the deal—most want some comfort room, so they’ll hunt for a DSCR of at least 1.25 before shaking hands.

What does a DSCR of 1.25 mean?

What does a DSCR of 1.25 mean?

If you’ve nailed a DSCR of 1.25, you’re ahead of the game by a quarter. For every dollar of debt you owe, you’ve got $1.25 in income to slap it down. It’s the green light lenders look for; it means you’re not just scrounging for pennies but actually stashing some away for a rainy day. Pretty comfy, huh?

Is a DSCR loan a good idea?

Is a DSCR loan a good idea?

Hmm, is a DSCR loan a good idea? Well, if you’ve got your ducks in a row, it can be a smart move. It’s a go-to for investors who want to snag a property based on its income potential, rather than their personal finances. Just remember, it’s no free lunch; you’ll need solid rental income to make the cut.

How do you increase DSCR ratio?

How do you increase DSCR ratio?

Looking to pump up your DSCR ratio? It’s all about fattening up your income or slimming down expenses. Hike up those rents where you can, cut costs without skimping on service, and voilà, your DSCR starts to climb. And hey, if you can refinance to lower payments, you’re golden!