Buckle up folks, it’s time to decode the power of debt service ratio! This magic ratio might not look like a big deal but it could play the lead role in your mortgage reduction ambitions. The main takeaway here? Get a handle on your debt service ratio, and you may be well on your way to owning your castle outright.

Decoding the Importance of Debt Service Ratio in 2024 Mortgage Reduction

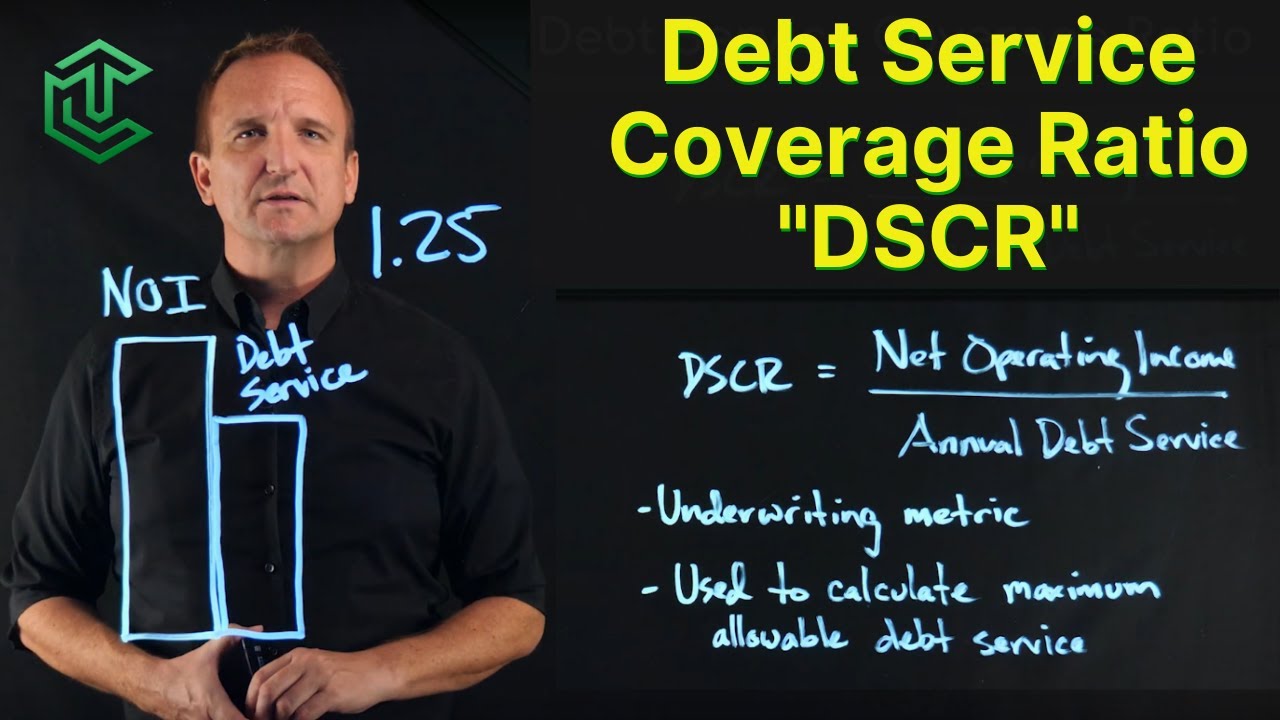

The debt-service coverage ratio, aka Dscr, calculates the cash flow available to pay current debt obligations. Simply put, this magic number reveals to investors and lenders if a company has enough income to pay the piper, otherwise known as its debts.

For a bit of cocktail party trivia, this debt service ratio is calculated by dividing your net operating income by your total debts, including interest and principal. But a DSCR of less than 1 means a negative cash flow, which is a sure sign the money tree needs more water. Understanding the nuts and bolts of DSCR is fundamental to financial planning and, crucially, mortgage reduction.

The Debt Coverage Ratio and Its Role in Assessing Mortgage Health

Just a bit deeper, the debt coverage ratio is your new favorite mini financial health check. Investopedia, the window into the finance world, says “it’s the net operating income divided by total debt service”. Think of it as your business’s cholesterol level – we all know too high or too low can stem trouble!

That’s why it’s essential to keep an eye on your debt coverage ratio when managing your mortgage. For example, a property with a DCR of 1.5 has ample income to pay for annual debt and operating expenses. Plus, it has a 50% cushion over this figure – and who doesn’t appreciate extra padding!

| Subject | Details |

|---|---|

| Definition of DSCR | Debt-Service Coverage Ratio (DSCR) measures a firm’s available cash flow to cover its current debt obligations. It depicts whether a company has sufficient income to pay off its debts. |

| Calculation of DSCR | DSCR is calculated by dividing the Net Operating Income (NOI) by the total debt service, which includes principal and interest. |

| Meaning of DSCR | A DSCR of 1 means the NOI is exactly equal to the annual loan payments. 1.25 suggests the NOI is 125% or 1.25 times the amount of the annual loan payments. Anything less than 1 indicates a negative cash flow situation. |

| Interpretation of DSCR | A DSCR of 1.5 means enough income is generated to cover all annual debt and operating expenses, and an additional 50% income over these expenses. A phenomenal DSCR of 2.25 means the property will earn 225% more income than owed on outstanding debts. |

| DSCR Loan Requirements | Lenders usually require a DSCR in the range of 1.2 to 1.25. This implies that the property’s NOI should be at least 120-125% of the annual loan payments. |

| Importance of DSCR | DSCR provides key insights for lenders and investors into a company’s financial health and ability to cover debt obligations with its operating income. It influences financing decisions made by lenders. |

| Limitations of DSCR | While DSCR is a critical metric, it is not the only factor considered by banks or other financial institutions during the loan approval process. |

Embracing the DSCR Formula for Effective Mortgage Management

Given the wonders of DSCR, understanding the formula and its application in managing your mortgage is already half the battle won. So, the big reveal is that DSCR is equal to net operating income divided by debt service. What does this mean? It’s a simple tool to know if your income is higher than your debt. For example, a 2.25 DSCR says that a property is raking 225% more income than its debts. Now that’s a breath of fresh air in a forest of financial jargon!

DSCR Loan Meaning: Helping Your Mortgage Reduction Goals

So, you wondered what DSCR loan means? Well, it’s a fancy term to explain a simple concept. Essentially, the DSCR loan requirements look at the relations between a property’s net operating income (NOI) and the loan payments.

In layman’s terms, lenders want to see a DSCR of at least 1.2 to 1.25, implying the property’s NOI is at least 125% of the annual loan repayments. Mind you, lenders don’t look at DSCR in isolation to approve loans. Other factors such as your smile don’t count though!

First Strategy for Mortgage Reduction: Increasing Net Operating Income

Shouting “show me the money” is one thing, creating it is another. One of the most fundamental ways to reduce your debt service ratio and tackle your mortgage reduction goals is by increasing net operating income.

The secret recipe? Boost your income and trim your expenses. This could range from carving out an Airbnb suite in your property (hello, cash flow!) to wearing your grandmother’s vintage denim skirt at the office to cut clothing costs.

By beefing up your net operating income, you heap more cash into paying your debt service, which puts significant downward pressure on your favorite three-letter acronym, DSCR.

Second Strategy for Mortgage Reduction: Reducing Debt Obligations

The flip side to increasing revenue? Reducing debt obligations. Cutting back on take-outs, using a bike instead of Ubering, or swapping your latte for a homemade cappuccino can all shave your outgoings. Combine this with a careful audit of your debts – think credit cards, student loans, and car loans ‒ and you might just see your DSCR shrinking before your eyes.

Third Strategy for Mortgage Reduction: Smart Refinancing

So, you’ve probably heard your neighbor Joe harp on about refinancing and how it magically reduced his mortgage payments. Well, he’s not wrong! Smart refinancing is an ace strategy that can have a significant impact on your debt service coverage ratio.

Smart like a fox yet savvy as a hedgehog, refinancing might allow you to snag a lower interest rate that consequently decreases your monthly payment. Packed with saving potential, this move alone could see you toe-tapping your way to a dramatically reduced DSCR.

Fourth Strategy for Mortgage Reduction: Opting for Longer Term Loans

Who doesn’t like stretched-out deadlines? A less obvious but highly effective path to reducing your mortgage involves choosing longer-term loans. While it may feel counterintuitive, spreading payments over a more extended period can curtail your monthly outflow.

A smaller monthly payment means less financial pressure each month and a more manageable debt service. Oh, and your DSCR? Watch it shrink like a bad laundry day.

Fifth Strategy for Mortgage Reduction: Prepayment of Loan Principal

Prepayment means you’re putting extra money toward your loan, and it’s a powerful weapon in your mortgage reduction arsenal. Every penny you prepay reduces your principal, which in turn drops your interest and cuts down loan term.

So, if you find a pot of gold at the end of the rainbow or win big on ‘Who Wants to Be a Millionaire’, use it to prepay your loan. You’ll be pleasantly surprised at the drop in your DSCR.

Sixth Strategy for Mortgage Reduction: Maintaining High Credit Score

In the game of mortgages, the credit score is king, and a high one can be your secret weapon. Keeping your credit score on bench-pressing shape can open doors to lower interest rates, smoother negotiation, and easier loan approval – all beneficial to reducing your DSCR. So, pay those bills on time, keep debt minimal, and let your high credit score do the talking.

Seventh Strategy for Mortgage Reduction: Increase Property Value, Increase NOI

Ever considered increasing your property value? Property enhancements that boost your NOI while positively impacting your DSCR are worth the investment. A gourmet kitchen, an attic conversion, or even a coat of paint can add significant value to your property.

An investment in your property is an investment in improving your DSCR. It’s a win-win!

Harnessing the Power of the Debt Service Ratio: Your Way to a Mortgage-Free Future

Picture this: you, the sunset, and a life free of mortgage payments. Wow, right? It’s not a dream if you harness the power of the debt service ratio.

By small steps or giant leaps, start implementing the highlighted seven strategies. Increasing net operating income, reducing debts, smart refinancing, opting for longer-term loans, prepayment, maintaining a high credit score, and increasing your property value are tools in your mortgage reduction toolbox.

The beauty of managing DSCR effectively is not just in financial security. It’s a pathway to more control, reduced stress, and even a mortgage-free life in your vivid future. Now crank up your favorite movie on Flixtor.to, kick back and relax, knowing your financial future is in your hands.

What does 1.25 debt service coverage mean?

Ah, you’re curious about the 1.25 debt service coverage ratio, aren’t you? Well, in plain English, it means for every buck you earn, a quarter is surplus, after covering your debt obligations. Essentially, if you’ve got this ratio, you can service your debt and still have a little something left over. Not too shabby!

How do you calculate debt service?

Now, to calculate debt service, it’s as easy as adding up your annual principal, interest and any lease payments. In other words, you’re tallying up what you’re coughing up annually for debt—pretty simple, right?

What is a 1.5 debt service ratio?

Now, a 1.5 debt service ratio, that’s a different kettle of fish. It means for every dollar of income you have, only around two-thirds is tied up in debt repayment. Definitely more breathing room there!

Is 2.25 a good debt service ratio?

As for the 2.25 debt service ratio, oh boy, that’s a pretty solid ratio in the grand scheme of things. It means for every dollar you’re making, you’ve got less than half of that earmarked for debt repayment. Pretty nice, huh?

What is a good debt service coverage?

A “good” debt service coverage ratio would usually fall between 1.15 and 1.35 – giving you some wiggle room after debt obligations. Anything higher gives lenders more confidence, so bear that in mind!

What is a bad debt service coverage ratio?

On the flip side, a “bad” debt service coverage ratio would be anything under 1. This means your income isn’t covering your debt repayments, which is definitely a sticky wicket.

What is the 55% total debt service ratio?

The 55% total debt service ratio simply means 55% of your gross income is going towards servicing your debts. Any higher and it might be time to tighten the belt a bit.

How do you increase DSCR ratio?

Want to increase your DSCR ratio? Pay off debt, increase income, or both! Piece of cake.

What is the debt service coverage ratio for a mortgage?

For mortgages, the debt service coverage ratio can vary. Generally, you’d want it to be 1 or higher to impress those lenders.

What is too high for debt service ratio?

Too high for a debt service ratio? That’d be anything over 36%. You don’t want to be drowning in debt, right?

What is a debt service coverage ratio of 1.2 to 1?

A debt service coverage ratio of 1.2 to 1 means you have 20 cents left over for every dollar you earn after your debt repayments. It’s alright, but could stand to be better!

What is the best ratio for debt ratio?

The best ratio for debt ratio is certainly subjective. But commonly, most folks say it’s around 36%.

Can I live in a home bought with a DSCR loan?

Now onto DSCR loans – good news! You sure can live in a home bought with a DSCR loan. Just remember, it’s all about managing those repayments, mate!

Is 7% a good debt-to-income ratio?

Is 7% a good debt-to-income ratio? You bet your bottom dollar it is! It indicates you’ve got your debt under control.

Do all banks offer DSCR loans?

Finally, do all banks offer DSCR loans? Sadly, no. But don’t lose heart. It’s always worth researching different lenders to find the right fit for you.