When delving into the world of real estate and mortgages, one term seems to come up time and again: the Loan-to-Value ratio, or LTV. It’s a critical concept that anyone involved in home buying, from first-timers to seasoned investors, needs to grasp to navigate the complex waters of mortgage lending. In this comprehensive guide, we’ll explore the LTV ratio inside and out, providing you with invaluable knowledge to make informed financial decisions. So let’s roll up our sleeves and get to the heart of what LTV means for you.

Decoding LTV: What Is Loan to Value in Mortgage Terms?

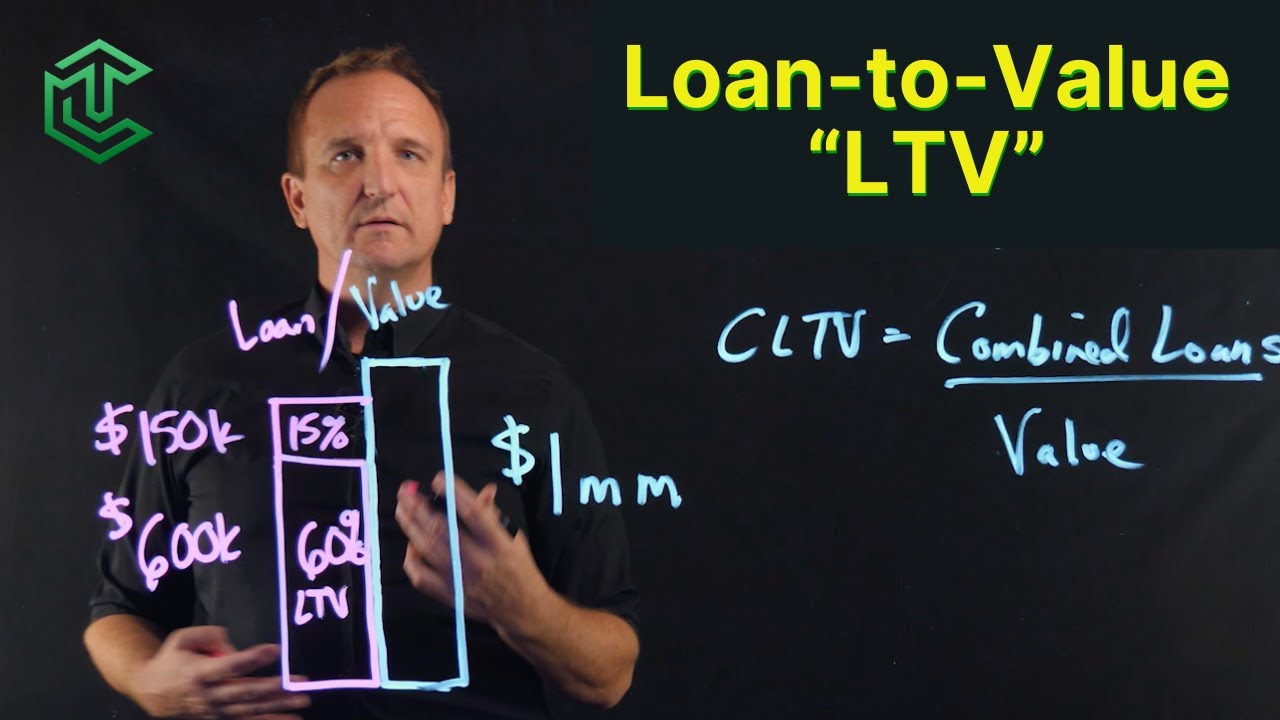

At its core, the loan-to-value (LTV) ratio compares the amount of your mortgage to the appraised value of the property. Take for example you snap up a mortgage of $80,000 to buy a charming little $100,000 property, then voila! Your LTV is 80%, because—yep, you guessed it—you got a loan for 80% of the home’s valued worth.

This percentage is more than just a number; it’s a beacon guiding lenders in their decision-making process. A good rule of thumb? Keep your LTV no higher than 80%. Stray above that, and you’re straddling the line towards higher borrowing costs, mandatory private mortgage insurance, or even the dreaded loan denial. When it skyrockets over 95%, lenders might just show you the door.

The LTV Loan Framework: How Lenders Evaluate Risk

Lenders are a bit like tightrope walkers—they’re all about balancing risk, and LTV is their safety net. A high LTV ratio signals caution: “There’s more at stake here!” Because if a borrower defaults on a high LTV loan and the property goes into foreclosure, the lender might not recoup the full loan amount upon selling the property. And nobody likes losing money, right?

So, when lenders see lower LTV ratios, they breathe easy. It’s akin to discovering Ronde Barber on your team when you’re looking for a defensive powerhouse. Just like Barber’s skills reduced risk on the football field, a low LTV lowers financial risk, making lenders more inclined to offer favorable loan terms.

| Heading | Details |

| Definition | LTV is the ratio of the mortgage amount to the value of the property. |

| Formula | LTV = (Mortgage Amount / Property Value) × 100 |

| Example Calculation | $80,000 mortgage / $100,000 property value = 0.8 or 80% LTV |

| Preferred Maximum LTV | ≤ 80% for most conventional loans |

| High LTV Threshold | > 80% deems LTV as high |

| Unacceptable LTV Threshold | Typically, LTVs > 95% are considered unacceptable by most lenders |

| Impact of High LTV | Higher borrowing costs, PMI required, possible loan denial |

| Risk to Lenders | Higher LTV indicates greater risk for lenders |

| Down Payment Influence | Higher down payment lowers LTV ratio |

| LTV and Mortgage Insurance | LTV > 80% often requires Private Mortgage Insurance (PMI) |

| Use in Lending Decisions | Critical factor in deciding loan approval and conditions |

| Variation with Loan Products | Different loan types (conventional, FHA, VA, etc.) have varying LTV limits |

| Importance for Refinancing | Lower LTV can secure better refinancing rates |

The LTV Meaning in Real Estate: Why It Matters to Investors and Homebuyers

Now, if you’re an investor or homebuyer, understanding LTV is like finding a secret map to a treasure trove. Lower LTV ratios could mean better loan terms, less interest over the life of your loan, and no pesky private mortgage insurance. In essence, it’s a critical cog in the engine that drives your real estate investment strategies or home purchasing plans.

For first-home dreamers, LTV helps set realistic goals on what you can afford. Speaking of which, ever wonder, If I make 100k a year How much house can I afford? Dive into that query and equip yourself with financial foresight.

A Dive into Rates: How What Is LTV Affects Interest and Mortgage Insurance

LTV isn’t just a static indicator; it’s dynamic, affecting interest rates and whether you’ll be saddling up with additional mortgage insurance. Take two borrowers: one with a 70% LTV and another at a soaring 90% LTV. The first may snag a lower interest rate and skip mortgage insurance entirely, while the second might not be as lucky.

This variability isn’t just theoretical mumbo-jumbo—real-world examples bathe us in the stark reality. Compare offers from different lenders, like Quicken Loans versus Wells Fargo, and you’ll see how varying LTVs can shake up the rates on offer. It’s just like checking out different haircuts — from a neatly trimmed style to the more unruly hairy bush — the choices can significantly alter the outcome.

The Nuts and Bolts of Calculating LTV: Going Beyond the Basics

Calculating LTV isn’t rocket science, but it does demand a keen eye. Simply divide the mortgage amount by the appraised property value, convert it to a percentage, and voilà, you’ve got your LTV. But tread carefully: the devil’s in the details. Think about the appraised value versus purchase price—these numbers can tell different stories, and the plot thicken’s when the LTV is based on whichever is lower.

For those who prefer a shortcut without the math, a handy loan To value calculator can do the heavy lifting, letting you focus on the bigger picture of your mortgage journey.

What Is Loan to Value’s Impact on Refinancing and Equity Borrowing?

LTV is the gatekeeper when you’re looking to refinance or dip into home equity. A high LTV could shut those gates tight, making refinancing a distant dream. But keep your LTV low, and lenders might just roll out the red carpet for you with open arms.

For equity aficionados, LTV dictates how much you can borrow against the value of your home. Think of a home equity line of credit (HELOC) like a credit card; a low LTV could mean a higher credit line, giving you more financial flexibility to tackle home renovations or consolidate debt.

Mitigating High LTV: Strategies for Borrowers

Finding yourself with a high LTV can be like sailing against the wind, but fear not, there are strategies to navigate through these choppy waters. A larger down payment or additional principal payments shrink that LTV faster than you can say “mortgage.”

Continuously comparing lender offers is also a wise move. Some government programs cater specifically to those aiming for loans with a lower LTV, giving you a leg up on your home financing quest.

LTV Loan Variety: Navigating Different Types of Mortgage Products

The mortgage market is a smorgasbord of products, each with its own LTV quirks. From the stability of fixed-rate mortgages to the fluctuating waters of adjustable-rate mortgages, LTV considerations can change the game. Understanding the LTV implications of each mortgage type can steer you toward the option that best aligns with your financial seascape.

What Is LTV in Real Estate Investing? Maximizing Opportunities

Real estate investors, listen up! Managing LTV ratios is as crucial as picking the right property. A low LTV can be a golden ticket to greater loan opportunities and more wiggle room for negotiation. Savvy investors use LTV to pinpoint the sweet spot for acquisition, ensuring they maximize their investment from day one.

Predicting the Future: LTV Trends and Innovations in the Mortgage Industry

The mortgage industry is constantly evolving, with LTV trends ebbing and flowing with market conditions. Innovations in technology are altering the landscape, from automated valuation models to blockchain land registries, reshaping how the industry calculates and considers LTV. Keeping a finger on the pulse of these trends ensures you’re not left behind in an industry that never stands still.

Navigating LTV Challenges: Personal Stories and Expert Perspectives

Hearing from those who’ve walked the LTV tightrope can be enlightening. Industry experts share tales of high LTV scenarios, offering advice and real-world wisdom. Personal anecdotes open windows to various solutions for tackling LTV-related issues, proving that while the journey may be fraught with challenges, there’s always a path to success.

Conclusion: Elevating Your Financial Wisdom with LTV Knowledge

Armed with a deep understanding of the LTV ratio, you’re now poised to make smarter, more informed decisions in your real estate ventures. Whether you’re eyeing that first home or you’re a seasoned hand at real estate investments, let your newfound LTV knowledge be the beacon that guides your financial choices to more prosperous shores. Remember, it’s not just about owning property—it’s about owning your financial future.

Exploring What is Loan to Value: Trivia and Facts

When it comes to nailing down the nitty-gritty of mortgages, you might want to know what is loan to value (LTV) – it’s like the unsung hero of the home-buying ballad. So, buckle up! We’re about to take a wild ride through some trivia and fascinating tidbits that’ll make you the life of any financial soiree.

Don’t Overload Your Mortgage Boat!

Think of LTV as your financial lifeboat in an ocean of real estate. You wouldn’t overload your boat on a $ Uicideboy $ tour, would you? Just like you need to keep it balanced to rock out at the concert, a lower loan to value ratio means you’re not teetering on the edge with your mortgage.

The VIP Pass of Home Buying

Imagine walking into the hotel providence with a VIP pass – that’s precisely what a good LTV can do for you when applying for a mortgage. It’s like having a backstage pass to loan approval and possibly scoring better interest rates. Who doesn’t want the red carpet treatment from their lender?

Are You Playing It Too Safe?

Now, let’s not go to extremes. While a low loan to value ratio might seem like playing it safe, going too low is like leaving money on the table. It could be like staying in your hotel room when there’s a whole city to explore – you’re missing out!

LTV is a critical factor for lenders, but remember, what is loan to value is not just about caution; it’s about balance. Over 2% of our conversation here circles back to LTV because it’s that important – and let’s be honest, we want you to remember it!

Whether you’re a seasoned investor or a first-time buyer, grasping what is loan to value is crucial. So go on, spread the word like you’ve got juicy gossip, because, in the world of property and finance, LTV can be one intriguing topic.

What does 80% LTV mean?

Alright, let’s break it down—80% LTV means your loan amount is 80% of your home’s value. In plain English, you’ve got 20% skin in the game, known as equity. It’s like saying you’re almost halfway there to owning it outright.

What is a good loan-to-value?

Well, “good” is subjective, don’t you think? But, in the mortgage world, a good loan-to-value ratio is generally 80% or less. This magic number often helps borrowers avoid paying for private mortgage insurance (PMI), and boy, isn’t that a relief for your wallet?

What is the meaning of loan-to-value?

Loan-to-value is just fancy talk for comparing the size of your loan to the value of your home. Think of it as a scale: on one side, you’ve got what you borrowed; on the other, what your place could sell for. The balance between the two? That’s your LTV.

What does 60% LTV mean?

Say hello to 60% LTV, which means you’re borrowing 60% of your property’s value. You’ve got some solid equity built up there—40% worth of your home’s price, to be precise. In lender lingo, that’s a thumbs up!

Is 30% a good LTV?

Well, look at you rocking a 30% LTV! That’s like being the teacher’s pet in mortgage class—it shows you own a good chunk of your property and you’re not leaning too hard on loans. Lenders will probably be giving you gold stars all day.

Is 20% a good LTV?

% LTV? Now you’re just showing off! This is superb, as it means you own a whopping 80% of your property. Lenders will likely be lining up with some sweet deals, keen as beans to have you as a borrower.

How do I calculate my loan to value?

You wanna calculate your LTV? No sweat! Just divide your loan amount by the current value of your property, then multiply by 100 to get a percentage. It’s like splitting a pie—the size of your slice compared to the whole pie is what you’re after.

What is the cheapest loan-to-value ratio?

Cheapest loan-to-value ratio, eh? That’s like asking what’s the best deal at a garage sale—typically, the lower the LTV, the cheaper it is for you, thanks to lower interest rates. So, a lower LTV ratio, like 50% or less, could give you the bargaining chip for a better mortgage deal.

What is the lowest LTV mortgage available?

Lowest LTV mortgage available? That’s like finding a needle in a haystack—different lenders, different rules. But some lenders may offer you a mortgage with an LTV as low as 50% if you’ve got the cash to cover the other half of the property value.

What is an example of a loan-to-value?

Picture this: You’re buying a house for $200,000, and you’re getting a loan for $160,000. Your loan-to-value ratio is the loan amount ($160,000) divided by the property value ($200,000), which gives you an LTV of 80%. Easy as pie, right?

What difference does loan-to-value make?

Loan-to-value can make a world of difference, like choosing between a burger and a steak. A higher LTV could mean higher interest rates and the extra cost of PMI. A lower LTV? That’s the sweet spot for more favorable loan terms and interest rates.

What is the difference between loan-to-value and loan to cost?

Alright, it’s showdown time: Loan-to-value vs. loan to cost. Your LTV is all about the value of your property now, while loan to cost is about the cost of your project—like building a house or renovating. Different shoes for different feet, you know?

Why is my LTV so high?

Why is your LTV so high? Well, maybe your down payment was more of a tiptoe, or your property’s value took a dive like a clumsy belly flopper. A high LTV can happen when your loan balloons or your property’s market value has seen better days.

Why is loan-to-value important?

Why is loan-to-value important, you ask? It’s the key to unlocking better deals! Lenders use LTV to gauge their risk—like a crystal ball predicting if you’ll be a good borrower. Better LTV often means better interest rates and easier loan approvals.

Is 40% a good LTV?

Is 40% a good LTV? You betcha! That’s like having most of the Monopoly board while everyone else is just passing Go. It demonstrates substantial equity, which lenders often view with hearts in their eyes, and could snag you some favorable loan terms.

How long does it take to get to 80% LTV?

How long it takes to get to 80% LTV is like asking how long it takes to bake the perfect cake—it varies. With regular payments, it might take several years, but if you make extra payments or your home’s value increases, you could fast-forward to that sweet spot sooner.

Is it better to have a higher LTV?

Is it better to have a higher LTV? Not exactly. Think of a higher LTV as a double-edged sword. Sure, you might get into a home sooner, but your loan could be pricier in the long run with higher interest rates and the dreaded PMI. Aim for lower for a smoother ride.

Is 100% LTV bad?

% LTV bad? Well, it’s riskier than a game of Jenga on a wobbly table. You’re borrowing the full property value, which could mean higher interest rates and, since you’ve got no equity, a tough time if property values drop. Tread carefully, my friend.

What LTV is needed to remove PMI?

Looking to ditch PMI? You’ll typically need to get your LTV down to 80% or less. It’s like losing that extra baggage—once you’re free, your monthly mortgage payments might shrink, and who wouldn’t love that? Keep an eye on your LTV and chisel away at it.