Homeownership is not just about having a roof over your head—it’s also a critical player in your financial health. And when we talk about financial health, the pulsating heart of the conversation often beats to the rhythm of home equity, a term frequently tossed around yet not always fully grasped by many. “What is equity in a house?”, you might ask. It’s the golden ticket that can grant you financial opportunities or serve as an emergency fund in pinch-me situations. Understanding the nuances can be the difference between simply living in a house and truly making it work for you financially.

What is Equity in a House: The Bedrock of Financial Health

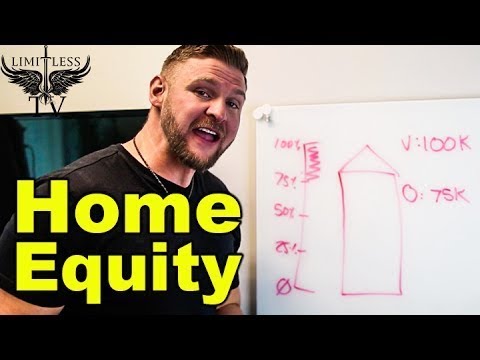

Picture this: Equity is the difference between the chunk of change your house is worth and what you still owe on your mortgage. If you’re sitting on a home that’s worth $300,000 and you owe $150,000, congratulations—you’ve got $150,000 in equity, giving you a pretty sweet 50 percent stake in your investment.

Equity isn’t just an abstract concept; it’s your slice of the pie, your piece of the financial cake! The beauty of it? Your money is tied up for now, but it’s readily accessible when needed. Someone boasting a loan-to-value ratio (LTV) of 50% or less is in an enviable position, considered equity rich.

Having high equity isn’t just about feeling financially buff—it’s about being strategically positioned. Say it’s time to dip into that equity, though. Where do you start? Well, you might look into home equity Loans, dabble in home equity Lines Of credit ( Helocs ), or consider cash-out refinancing. Each option opens a door to those tightly held funds without the need to sell your sanctuary.

The Inner Workings of Home Equity: How Does Equity Build Over Time?

Building equity is like nurturing a seedling—it needs time, a conducive environment, and proper care. So, how does equity work? As you chip away at your mortgage, it’s like filling up a piggy bank; every payment is more equity in your pocket. Pair this with the ever-swinging property value pendulum, and you’ve got a dynamic dance of dollars. Think of it as a financial choreography where you’ve got to nail your steps.

- Pay down the principal, and your equity goes up.

- Sit back as the neighborhood becomes the next big thing, and watch your equity rise with those property value waves.

- On the flip side, take a hit in the housing market, and your equity could shrink faster than a cheap cotton shirt in the wash.

Calculating your individual slice of the equity pie means staying acutely aware of these factors. A proactive approach here doesn’t just happen—like Mike Myers masterfully crafted his film career, it takes knowledge and strategy.

| Category | Details |

|---|---|

| Definition | Equity in a house is the portion of the property’s value that the homeowner actually owns, free of any liens or encumbrances. |

| Calculation | Equity = Current Market Value of Home – Remaining Mortgage Balance |

| Example 1 | If the current home value is $200,000 and the outstanding mortgage is $150,000, the equity is $50,000. |

| Example 2 | For a home worth $300,000 with a mortgage balance of $150,000, the equity is $150,000, which is 50% of the home’s value. |

| Equity Rich | Generally refers to a homeowner with a loan-to-value ratio (LTV) of 50% or less. |

| Importance of Building Equity | Increases financial leverage, potential to borrow funds, long-term wealth, and profit upon selling the home. |

| Ways to Utilize Equity | – Home Equity Loans: Borrow a lump sum against the equity at a fixed interest rate. |

| – Home Equity Line of Credit (HELOC): A revolving line of credit with variable rates, allowing withdrawals as needed. | |

| – Cash-Out Refinancing: Refinance the mortgage for a higher amount than owed and receive the difference in cash. | |

| Benefits of High Equity | – Lower risk of being “underwater” on your mortgage. – Potentially lower interest rates for loans using home equity. – Increased borrowing power for home equity lines of credit. – Opportunity to eliminate private mortgage insurance (PMI) sooner. |

| Risks of Tapping into Equity | – Increased debt burden. – Risk of foreclosure if unable to repay. – Potential for reduced future sale profits. |

Calculating Your Share: What is Equity in a Home in Real Numbers?

Let’s put on our math caps and boil down the details. When we talk about what is equity in a home, we’re doing some simple subtraction:

Suppose Judy has paid off $250,000 of her $300,000 mortgage. With her home’s value skyrocketing to $500,000, she’s now rolling in a cool $250,000 of equity. Keep in mind that tapping into this money isn’t like using an ATM; it involves financial decisions and sometimes, costs.

The Financial Leveraging Powerhouse: Utilizing What is Home Equity

Harnessing your What Is home equity is akin to wielding a financial wand—it can conjure up cash when you need it. But exactly how to unlock this magic is an art in itself.

The trick is knowing when to pull these levers. Like finding a rare target Promo code 2023, it’s about timing and making an informed play.

Pulling Back the Curtain: What is Equity in a House for Investors?

Now, let’s peer into the realm of real estate investors. For them, equity isn’t a quiet savings account—it’s a dynamic tool to finance their next move. It’s about buying, growing, and flipping—turning homes into ladders to financial peaks. Savvy investors leverage their equity to snatch up new properties faster than you can say Paros Hilton nude (metaphorically, of course).

By cashing out on equity through refinancing or using it as collateral for an investment loan, these masterminds expand their portfolios, bolstering their capacity to capitalize on burgeoning markets from Mcallen To Harlingen.

Guarding Your Castle: Protecting and Growing Your Home Equity

Sure, your home is your castle, but in the realm of equity, it’s also your treasury. Here’s how to protect and fatten up that financial fortress:

Consider this: a splendid pool might seem alluring, but will it pay off in equity? Sometimes, it’s the less glamorous touch-ups, like insulating the attic or updating your HVAC system, that truly crank up the value.

Beyond the Obvious—Unexpected Ways to Leverage Home Equity

Picture yourself surfing beyond the breakers—there’s an entire ocean of less conventional ways to use home equity if you’re willing to paddle out:

Exploring non-traditional paths requires the right mix of boldness and brainpower. Daring yet calculated moves can pave the way for a future as bright as a dance floor at a ’70s disco!

Conclusion: Unlocked Potential—The Road Ahead with Home Equity

Peering through the keyhole, we see how ripe with possibilities home equity is. The journey to what is equity in a house is more than a mere accumulation of numbers—it’s about wielding this powerful asset to carve out the financial life you envision.

Remember, as we unlock these secrets, we’re not just looking to stash away funds or bleed them dry—we’re plotting a course for a more secure and financially fruitful tomorrow. So, take this knowledge, keep up with your payments, and watch the market tides; equity, after all, is your silent partner in this wealth-building dance.

By offering valuable insights on how does equity work and what is equity in a house, MortgageRater.com hopes to be the compass that guides you through the complex landscape of home finances. So here’s to turning the lock, opening the door, and stepping confidently into a braver, bolder financial future with equity as your trustworthy ally.

Discovering the Nuts and Bolts of What Is Equity in a House

Ever wonder if your house could be more than just a cozy shelter? Let’s dive into the world where your home moonlights as a piggy bank! The question “what is equity in a house?” might sound as thrilling as watching paint dry, but buckle up—things are about to get interesting.

Home Equity: The Treasure Hidden in Your Walls

Think of your home as a giant Monopoly property. Every mortgage payment is like passing ‘Go’ and collecting $200—except it’s not play money, it’s a slice of your home’s value. Home equity is the difference between what your home is worth and the amount you owe on your mortgage. So if your home is worth a cool quarter-million, and you owe $150,000, you’re sitting on $100,000 of equity. That’s real money which could be doing anything from chilling out to waiting for you to cash it in!

Growing Your Equity Garden

Now, let’s chat about how you can grow that equity. Picture your mortgage payments as watering your financial garden. With each payment, you water a little more, and over time, watch that equity blossom! But remember, it’s not just your payments doing the heavy lifting. If your neighborhood becomes the next big hotspot—boom—your home’s value might skyrocket. That’s right, while you’re enjoying that new espresso bar on the corner, your equity is doing a happy dance.

“Equity” Doesn’t Spell “Free Cash,” But It’s Close

Woah, hold your horses! Before you start dreaming of swimming in a pool of dollar bills like some cartoon tycoon, remember that tapping into equity isn’t free. Yes, you can borrow against it for a lovely home reno or to pay for your kid’s education, but it’s not a bottomless piggy bank. It’s more like taking a loan from your future self. Knowing “what is equity in a house” is cool, but making smart moves with it? That’s genius.

The Plot Twist: When the Debt Curtain Falls

Hold onto your hats because here’s a twist: Equity can be a bit of a drama queen when it comes to debt. Yikes! If there’s less left on the mortgage, more equity is strutting around. But remember, life’s finale can change the final act. Wondering What Happens To Your debt When You die? It doesn’t just vanish like a ghost! It can affect the equity in your home. If you’re dreaming of leaving a nest egg for your loved ones, ensuring that your debt doesn’t play the villain is vital.

A Parting Nugget of Wisdom

By now, you’re probably a mini-expert on “what is equity in a house.” Just remember, like a good wine, equity tends to get better with time. So, be patient, make smart choices, and before you know it, you’ll have a nifty nest egg. So the next time someone asks about home equity, you can proudly say, “It’s the hidden treasure in my abode—and I’m the savvy pirate steering the ship!”

Who knew the secrets of home equity could be this captivating? Go ahead, share your newfound knowledge, and watch as your friends marvel at your financial savvy!

How does the equity in a home work?

– Think of home equity like a piggy bank—it’s the part of your home you truly “own,” you know? As you pay down your mortgage or as your home’s value goes up, your equity grows. It’s like adding more coins to your piggy bank, except it’s bigger and doesn’t rattle!

What is a good equity to have in a house?

– Well, there’s no one-size-fits-all answer here, but having at least 15-20% equity is a good start. That’s the sweet spot for many lenders if you’re aiming to refinance or take out a loan.

How do you take equity out of your home?

– Alright, so you want to get your hands on some of that equity cash? You’ve got options like a home equity loan or a HELOC (that’s a home equity line of credit, by the way). Or, refinancing with a cash-out option can do the trick, too—just remember, you’re borrowing against your home!

Is it good to have equity in your home?

– Absolutely! Having equity is like having a financial ace up your sleeve. It can boost your net worth and be your safety net when the going gets tough with finances.

Is pulling equity out of your house a good idea?

– Pulling equity out of your house isn’t something to jump into without thinking it through. Sure, it can be a lifesaver in a pinch or for big investments, but remember, it’s tied to your home. So, weigh the pros and cons carefully!

Do you have to pay back equity in your home?

– You betcha! Taking out equity isn’t a giveaway—it’s more like a loan against your home. So, if you go for a home equity loan or a HELOC, be ready to make those payments back with interest.

What happens to equity when you sell your house?

– When you sell your house, the equity is the portion of the money you get after settling up the mortgage balance. Think of it as the grand finale of a show, where you reap the rewards of your investment!

How soon can you take equity out of your home?

– Hold your horses! Generally, lenders like to see that you’ve owned your home for at least a year before they’ll chat about home equity loans or HELOCs. Patience is a virtue, right?

How much equity can I borrow from my home?

– How much equity you can borrow depends on a few things, like your lender’s rules and your financial health. But a common rule of thumb? Lenders might let you borrow up to 85% of your home’s equity. Just keep in mind it’s not free money—it comes with strings attached.

Should I use my equity to pay off debt?

– Using your equity to wipe out debt can feel like hitting the reset button on your finances. But, it’s not a no-brainer. Crunch the numbers and consider if the lower interest rates are worth the long-term commitment to paying off your home.

Can I get equity out of my home without refinancing?

– Yep, you can get a home equity line of credit without going through a full-on refinance shindig. It can be less of a hassle and might save you some dough on closing costs.

What is the cheapest way to get equity out of your house?

– The thrifty way to tap into your equity? A no-frills home equity line of credit might have lower upfront costs compared to full refinancing or a second mortgage. Still, don’t forget to peek at the interest rates and fees.

Do you ever lose equity in your home?

– Your home equity isn’t exactly a runaway train—it’s more stable than that. But, if your home value dips or you take out a loan against it, it’s true, your equity could take a hit.

Does my mortgage go up if I take out equity?

– When you grab some of that equity, your mortgage balance stays the same—unless you’ve gone down the cash-out refinance route. But remember, the devil’s in the details, so check those loan terms!

Is it better to have home equity or cash?

– Now, there’s a debate for the ages! Home equity is like having a nest egg under your roof, while cash is king for immediate needs. Sit down and chew over your financial goals to figure out which works better for you.

How can I use the equity in my home to make money?

– Think of that equity as seed money—it can help plant the seeds for future growth. You could use it to invest, start a business, or make home improvements that boost your property value. Just don’t put all your eggs in one basket!

How does home equity work for dummies?

– Home equity, in a nutshell, is the share of your home you actually own. Imagine your home’s value is a pie – every mortgage payment is a tiny slice you get to keep for yourself. More slices, more pie for you!

What is the monthly payment on a $100 000 home equity loan?

– Time for some quick math: a $100,000 home equity loan, depending on the interest rate and term, could set you back a few hundred bucks monthly. But hey, every lender’s different, so shop around for the best deal.

How soon can you take equity out of your home?

– Whoa, déjà vu! Like I said earlier, you’ll typically need to give it a year before you think about borrowing against that equity. It’s like letting a good wine age—you want your investment to mature.