The landscape of new mortgage rates is ever-changing, and as we march further into 2024, many homebuyers and refinancers are perched on the edge of their seats, asking one burning question: “Will new mortgage rates drop again?” Let’s sift through the economic signals, examine the pulse of the housing market, and listen to what the experts are forecasting. By the end of our journey, you’ll be equipped with a broad, informed outlook on new mortgage rates, giving you the insight to make savvy financial decisions—no crystal ball needed.

Understanding the Landscape of New Mortgage Rates in 2024

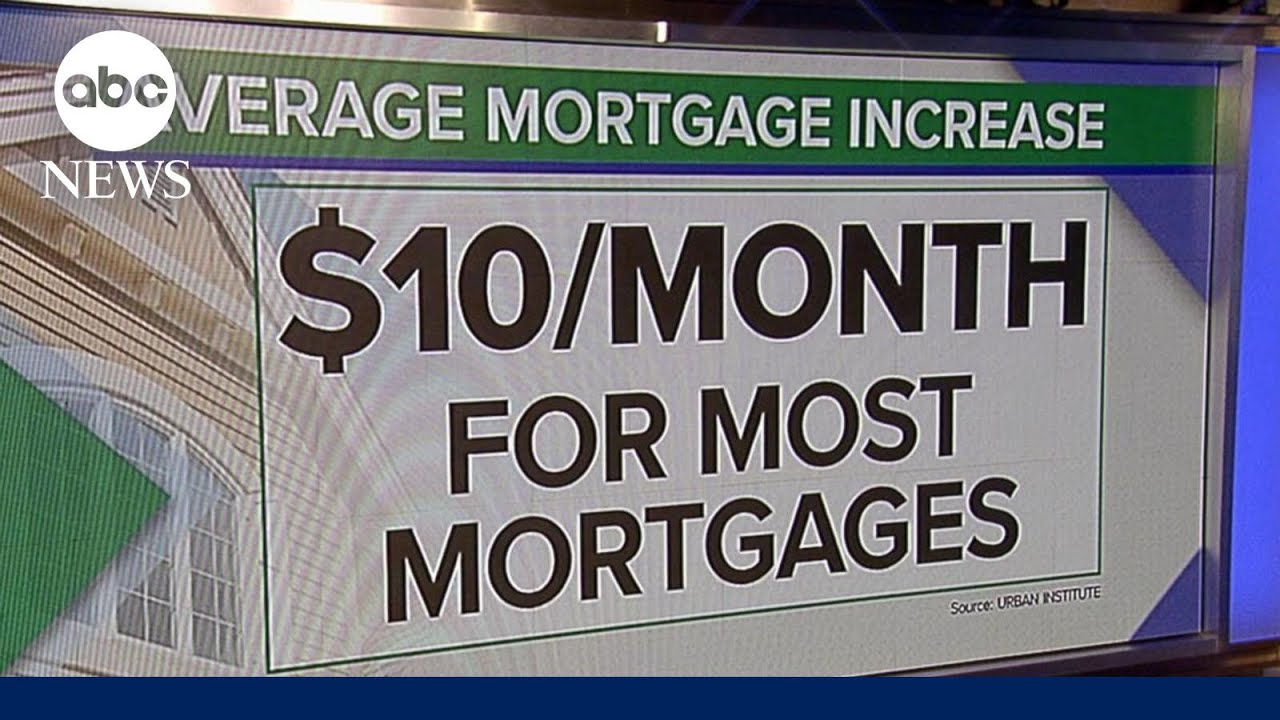

The current state of new mortgage rates in 2024 is akin to a roller coaster that’s had its fair share of ups and downs. Individuals peeking at their calendars while sighing at rate charts are seeing something that’s not quite a surprise. With inflation stubbornly gripping the economy, the prospect of finding those once-in-a-lifetime low rates seems slim. The buzz around new mortgage rates not returning to a cozy 3% anytime soon is sourced from an unpleasant combination of factors, with high inflation taking the lead like a persistent villain in an action flick.

Looking at the historical trail of breadcrumbs, mortgage rates have capered around in response to economic stimuli, showing us that calm waters can indeed surge into fierce waves. Over the past few years leading up to 2024, rates have been a reflection of the economic rigmarole—dipping during times of crisis and elevating as the Federal Reserve takes up arms against inflation.

Factors stirring the pot include the Fed’s interest rate hikes ushering in a tightening policy, all to quell the inflation that’s burning at a 40-year high. Consumer prices ballooning like a child’s party balloon means more expensive lending rates—no two ways about it. And it goes without saying, these rates are deeply intertwined with the health of the wider economy, from job numbers and GDP growth to global economic tremors.

Analyzing Economic Indicators Affecting New Mortgage Rates

Peering through the murky waters of economic indicators without getting cross-eyed is a feat, but it’s clear as daylight that factors like inflation, GDP growth, and employment rates sit in the driver’s seat. High inflation alone has the Federal Reserve in a bit of a bind, stringing up interest rates like fairy lights in an attempt to cool things down.

Economic gurus are keenly observing how the Fed’s stiff upper lip affects everything from your piggy bank to national spending patterns. As Mortgages interest dance to the tune of federal policies, it’s like a domino effect—either paving the way for stability or shaking investor confidence.

We’ve heard through the grapevine and expert analyses that trends tend to come in waves. Here we are, grappling with predictions that hinge on the ebb and flow of economic health. The fundamental truth, it seems, is that the fiscal magnifying glass is firmly focused on inflation and employment stats, teasing out insights that could hint at future rate movements.

| Lender | Loan Type | Interest Rate | APR* | Monthly Payment** | Points | Closing Costs*** | Features/Benefits |

| ———————— | —————— | ————–: | ——: | ——————: | ——-: | —————-: | ——————————————————————————————– |

| Bank A | 30-year Fixed | 5.250% | 5.350% | $1,104 | 0.5 | $2,500 | – Stable payments – No prepayment penalty |

| Credit Union B | 20-year Fixed | 4.875% | 5.000% | $1,320 | 1 | $2,200 | – Faster equity build-up – Lower total interest cost |

| Online Lender C | 15-year Fixed | 4.500% | 4.650% | $1,529 | 0 | $1,800 | – Lower interest rate – Shorter loan term – Pay off home sooner |

| Mortgage Broker D | 5/1 ARM | 4.125% | 4.875% | $969 | 0.75 | $3,000 | – Lower initial payments – Potential rate and payment increase after 5 years |

| National Bank E | Jumbo 30-year FR | 5.500% | 5.625% | $2,838 | 1.25 | $5,500 | – Financing for high-priced homes – Fixed-rate security |

| Community Bank F | FHA 30-year FR | 5.000% | 5.250% | $1,342 | 0.25 | $3,700 | – Lower down payment requirements – Great for first-time homebuyers |

| Savings & Loan G | VA 30-year FR | 5.000% | 5.150% | $1,342 | 0 | $1,500 | – No down payment for eligible veterans – No private mortgage insurance required |

Prospects of New Mortgage Rates in Response to Housing Market Dynamics

Now, pivot to the housing sector where the weather report on new mortgage rates hinges on the balmy and blustery trends of home supply and demand. Think of the housing market as a living, breathing entity with moods that swing—one day it’s all sunshine and buyer optimism, and the next could bring clouds of seller hesitance.

The real estate market doesn’t just sit pretty in its bubble; it’s actively shaping mortgage rates. When homes fly off the market faster than hotcakes, rates often twirl upwards. Conversely, when the For Sale signs start gathering dust, there could be a gentle pressure easing rates down.

Let’s not overlook the legislative dimensions here. If Uncle Sam pulls out a new policy rabbit from his hat that either boosts home buying or puts a damper on it, you can bet your bottom dollar that’ll ripple through to the national mortgage rates. It’s a give and take, really, as regulation shakes hands with market dynamics, affecting your wallet.

Financial Institutions’ Strategies and Their Influence on New Mortgage Rates

When the big kahunas like JPMorgan Chase and Wells Fargo scribble down their mortgage rates, they’re painting the big picture for the rest of us. These major banks are sort of like trendsetters at fashion week—they unveil their rates, and smaller banks and non-bank lenders take their cues for a walk down the runway.

Strategies vary like summer salads—some are fresh and zesty with competitive rates to lure in borrowers, while others are a bit more reserved, holding back for a market upturn. And let’s not sidestep credit unions, those kid brothers of the financial world, often offering a cuddlier touch with potentially more appealing terms.

It seems as though every financial institution has its secret sauce—a unique blend of loan products or promotions, like a whiff of Mega crush Crocs drawing in a crowd. These offerings add their own spice to the overarching trend of where mortgage rates might jog to next.

International Events and Their Impacts on New Mortgage Rates

Turn on the world stage, and it’s clear international events can be as influential on U.S. mortgage rates as a barista is to your morning perk-up. Think back to significant global shenanigans, and it’s evident—what happens across the pond or over the wall can send shockwaves to our shores.

The seesaw of current international skylarks and economic hullabaloos could nudge our rates in unexpected directions. Whether it’s geopolitical turmoil or overseas market upheavals, the U.S. housing market sits in the global nest—not an isolated island.

In this age of intertwined economies, the beat of the global drum does play a tune that domestic mortgage rates, intentionally or not, find themselves tapping their feet to. It’s an intricate dance, one we’re all part of whether we’ve got the rhythm or not.

Technological Advancements and Their Role in Shaping New Mortgage Rates

Trust technology to be the sleek, silent power player in the mortgage game. Fintech firms are stepping up their game faster than a teen on a prom date, leveraging everything from AI to big data to shake up the mortgage landscape. These tech titans are pushing traditional lenders to pick up their pace or risk getting left in the dust.

Imagine mortgages getting crunched through algorithms like sloppy Steaks, slicing and dicing data to predict and influence rates with a level of precision that’s nearly uncanny. It’s not science fiction; it’s the 2024 reality, where blockchain might just revolutionize the secure dance of mortgage transactions—and who knows how that’ll twist rates moving forward.

Potential Government Policy Changes and Predicted Effects on New Mortgage Rates

The wild card in the deck always seems to be Uncle Sam, with the potential to reshape the playing field overnight. With government policies lumbering through the legislative maze, those with a stake in the homes and hearths wonder how these potential changes might shake up their mortgage plans.

Policy whispers from the halls of power—whether from lawmakers, Treasury officials, or housing authorities—are worth tuning into. As they weigh the scales of housing finance’s future, so too do the hearts of rate-watchers flutter. It’s not so much reading tea leaves as it is keeping an ear to the ground for the drumbeats of policy change—ones that could very well send mortgage interest rates on a new trajectory.

Consumer Behavior and Its Impact on Future New Mortgage Rates

Turning the lens on ourselves, the everyday folks with dreams of white picket fences or chic city lofts, it’s clear our collective wallet has a voice. Debt levels soaring higher than the clouds, or savings stacking up like a bee’s honeycomb, can pull the strings on mortgage demand.

The social fabric of America is changing, with millennials finally closing their laptops and stepping into open houses, while baby boomers are opting for something snugger for retirement. These waves of demographic movement are like the tide affecting the shores of mortgage rates—from subtle shifts to potential tsunamis of change.

Future Economic Scenarios and Mortgage Rate Projections

Ever tried to predict the weather for next month? Well, economists do that for mortgage rates, speculating on whether we’ll need umbrellas or sunhats. With different scenarios painting pictures of growth or recession, these projections are as colorful as they are varied.

Some experts are sketching out graphs and charts like modern-day Picassos, offering visual projections of where rates might trot off to. It’s this blend of art and science that keeps the financial markets on their toes and has homebuyers either wringing their hands or rubbing them in glee.

Expert Opinions and Consensus on the Likelihood of a New Mortgage Rate Drop

Now, don’t just take it from me. Mortgage pundits, lined up like judges at a talent show, have their opinions on whether new mortgage rates will take another bow. The chatter ranges across the board—from bullish to bearish, with a side of reality checks.

It’s about sifting through the noise to find the expert opinions with substance. Like fans at a football game, they’ve got predictions and projections, but the scorecard is still a work in progress. Sure, the mood points to a less-than-rosy view on dramatic rate drops, but faith in the numbers and analysis is king.

Making Sense of It All: What to Expect with New Mortgage Rates

Taking a step back, it’s a mosaic of factors at play here, with each piece adding its own hue and texture to the larger image of where new mortgage rates might be heading. For homebuyers and owners, it’s about strategy—anchoring your sails and reading the winds to navigate these waters wisely.

Watch for the signs, be it from the Fed, the government’s policy deck, or the pulse of the consumer marketplace. Your best ally is information—unbiased, factual, and dissected with the precision of a seasoned pro.

Conclusion: Navigating a Shifting Landscape of New Mortgage Rates

So there you have it—a tapestry of intricacies shaping the future of new mortgage rates, woven from threads of fiscal policies, global events, and tech advancements. As you step through this shifting terrain, remember the importance of staying informed, being agile, and leaning into the winds of change.

Consider this article your compass, pointing towards informed decision-making. As we look to the horizon, it’s about embracing the ride, knowing that fortunes in the mortgage rate landscape are as fickle as spring weather. Stay keen, stay knowledgeable, and most of all, stay ready to turn insights into action.

A Glimpse Into the Crystal Ball: Will New Mortgage Rates Dip Once More?

As unpredictable as celebrity paths—take Presley Gerber, whose turn from fashion modeling to entrepreneurial pursuits turned heads—it’s tough to foresee where new mortgage rates will land in the future. But much like the young Gerber’s surprising career moves covered in this enigmatic profile, the world of mortgages keeps us on our toes. Speaking of surprises, did you know that the Bank of England was established way back in 1694, making it one of the oldest central banks in the world? Its creation was all about handling war debt, which is kind of a far cry from helping us finance our homes. But hey, origins matter, and mortgage rates have their own humble beginnings in the grand historical tapestry.

Intriguing Twists and Turns of Mortgage Rate History

Sure, discussing mortgage rates might not be as gripping as the latest thriller featuring Percy Hynes white, yet the history is filled with its own dramatic rises and falls. Much like the plot of a story appearing in this insightful article, the journey of new mortgage rates is nothing short of a roller coaster. Imagine this: back in the late 1940s, mortgage rates were around 5%. Fast forward to the early 1980s, and homeowners braced themselves as rates soared above a staggering 18%!

And while we’re musing over historical twists, did you know that the world’s very first recorded “mortgage” roughly dates back to Ancient Rome? Who would’ve thought that something as ancient as a Roman villa would plant the seeds for today’s complex financial systems? Picture a world without Sigourney Weavers iconic roles—a bit dull, right? Well, similarly, our financial world without the concept of Mortgages interest rates would be unrecognizable!

The future of new mortgage rates is as hard to pin down as a celebrity’s next move on the silver screen. And while we don’t have the scripts for what’s to come, one thing’s for sure: whether rates will drop again or not, keeping an eye on their trends is as crucial as tracking Sigourney Weaver’s illustrious acting career.( Understanding mortgage rate fluctuations can be as complex as predicting Oscar winners, but hey—that’s where the thrill lies, right? Stay informed, and you’ll be ready for action, just like one of Weaver’s fearless on-screen characters.

What is the interest rate on new mortgages?

– Look, the interest rate on new mortgages varies like the weather, but it’s safe to say they’re not exactly bargain-bin prices lately. With all the financial hoo-ha going on, rates are reacting faster than a cat on a hot tin roof. So, it’s best to check today’s rates ’cause tomorrow’s a whole new ball game.

What are the latest mortgage rates?

– Now, as for the latest mortgage rates, they’re like a roller coaster that’s been more up than down recently. You’ll wanna shop around, ’cause lenders are all over the map with their offers. But remember, the rate you nab is gonna depend on the ever-changing mood of the economy.

What is a good mortgage rate for 30 year fixed?

– A good mortgage rate for a 30-year fixed is kinda like Goldilocks’ porridge—everyone’s looking for that just-right number. It’s a moving target, so what’s hot today could be stone-cold tomorrow. Keep an eye on trends and haggle hard with your lender for the best deal!

Will mortgage rates go down to 3 again?

– Will mortgage rates ever slip down to a cozy 3% again? Well, don’t hold your breath. As much as we’d all love a time machine, the crystal ball’s hazy and—spoiler alert—it ain’t looking likely in the foreseeable future, especially with inflation being as stubborn as a mule.

Are mortgage rates expected to drop?

– Are mortgage rates expected to dip anytime soon? It’s a bit of a sticky wicket, with experts tossing their two cents around. But given the sky-high Inflation, it seems our wallets won’t be getting a break anytime soon. So, don’t bet the farm on a drop just yet, folks.

Will rates go down in 2024?

– And about the odds of rates taking a nosedive in 2024? Well, that’s the million-dollar question! The tea leaves are tough to read, and while we all wish for a happy surprise, the big brains say it’s as likely as finding a unicorn in your backyard, thanks to a pesky thing called Inflation.

Can I get a 30-year mortgage at 60 years old?

– Can a ripe young thing of 60 snag a 30-year mortgage? You bet your bottom dollar! Age ain’t nothing but a number, and lenders focus on the nitty-gritty like income, credit score, and down payment. So, if you’re 60 and ready to roll, go get that home sweet home!

Who offers lowest mortgage rates?

– Who’s dishing out the lowest mortgage rates? It’s a bit of a free-for-all with banks, credit unions, and online lenders duking it out. The trick is to play the field. Compare, contrast, and arm-wrestle them down to a rate that doesn’t make your wallet weep.

What is the lowest ever mortgage rate?

– What’s the lowest mortgage rate ever, you ask? Well, back in the good old days, rates dipped low enough to make your heart sing. Though we might not see the likes of that again, it’s still worth sniffing around for a rate that doesn’t hurt your feelings.

Is it better to buy a house when interest rates are high?

– Buying a house when interest rates are sky-high? Oof, that’s like choosing to walk the dog in a downpour! It’s a bit rough, but sometimes you’ve gotta do what you’ve gotta do. Just know that high rates mean pricier monthly payments, so weigh up whether it’s the right time for you.

Will mortgage rates ever drop below 5 again?

– The million-dollar question: Will mortgage rates ever sneak back below that 5% mark? No one’s got a crystal ball, but considering the current inflation kerfuffle, it’s about as likely as a snowball’s chance in July. Keep your fingers crossed, but maybe don’t hold your breath.

What is the interest rate today?

– And lastly, what’s today’s interest rate? In the fast and furious world of finance, rates are zippier than a squirrel on an espresso shot. So, do your homework, check today’s numbers, and keep your ear to the ground for the latest scoop.