Understanding the Role of a Mortgage Principal and Interest Calculator

Navigating the murky waters of mortgage options can feel overwhelming. Luckily, a mortgage principal and interest calculator emerges as a beacon of clarity. These calculators aren’t just tools for determining your monthly payments—they break down how much of each payment goes toward the principal versus the interest. Knowing this helps you understand the true cost of your mortgage over time.

Essentially, a mortgage principal and interest calculator helps you budget more effectively and make informed decisions. It illuminates the path to financial stability by highlighting how different variables, like interest rates and loan terms, affect your payments. By providing a comprehensive breakdown, these calculators let you strategize and adjust your payments, potentially saving you thousands in interest over the life of the loan.

Whether you’re buying your first home, refinancing, or just curious, these calculators are indispensable tools, giving you a clear view of your financial landscape.

Top 5 Mortgage Principal and Interest Calculators in 2024

With a sea of options available, pinpointing the best mortgage principal and interest calculator can be quite the task. To ease your search, we’ve zeroed in on the top 5 calculators for 2024, based on functionality, user-friendliness, and accuracy.

1. Bankrate Mortgage Calculator

The Bankrate Mortgage Calculator rises to the top with its comprehensive features and ease of use. It’s a go-to for both buyers and refinancers, thanks to its detailed amortization schedules and the ability to input extra payments. This feature is gold for seeing how additional contributions can nip interest payments in the bud and shorten your loan term.

2. NerdWallet Mortgage Calculator

The NerdWallet Mortgage Calculator boasts a user-friendly interface that adds a visual twist. It’s ideal for first-time buyers trying to wrap their heads around their financial commitments. You’ll appreciate how straightforward it is, especially if numbers aren’t your thing.

3. Zillow Mortgage Calculator

The Zillow Mortgage Calculator shines with its integration of real-time market data, providing users with up-to-date interest rates. This tool is a gem for those wanting accurate data aligned with current market conditions. It’s a breeze to use and offers detailed payment breakdowns, simplifying your mortgage management.

4. Mortgage Calculator.org

If you’re after a traditional tool, Mortgage Calculator.org pulls no punches. Known for its no-nonsense approach, this calculator offers a range of features such as tax and insurance estimations. It caters to serious buyers looking to get a full picture of their financial obligations.

5. Chase Mortgage Calculator

The Chase Mortgage Calculator integrates seamlessly with its banking services, making it a solid pick for existing Chase customers. It offers customized loan options and pre-qualification directly through the tool, making your mortgage journey smoother.

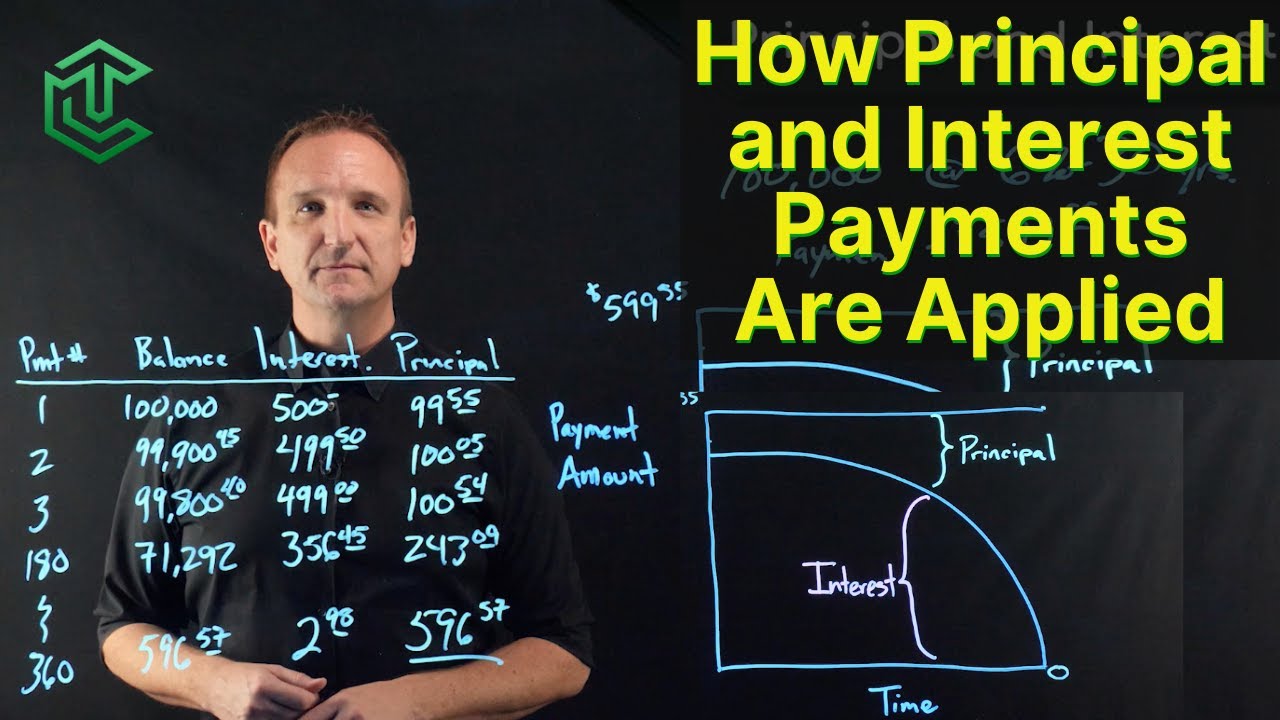

| Feature | Details |

| Purpose | Helps calculate monthly mortgage payments, including the breakdown of principal and interest over the loan term. |

| Key Steps for Calculation | 1. Convert annual interest rate to a monthly rate by dividing by 12. |

| 2. Multiply the loan amount by the monthly interest rate to find the monthly interest payment. | |

| 3. Subtract the monthly interest payment from the total monthly payment to determine the monthly principal payment. | |

| Tipping Point | The moment when you start paying more principal than interest. For a 30-year loan at a fixed rate of 4%, this point is more than 12 years into the loan. |

| Principal Payment Proportion Over Time | – After 1 year: 31% of the payment goes toward principal. |

| – After 10 years: 45% of the payment goes toward principal. | |

| – After 20 years: 67% of the payment goes toward principal. | |

| Example Calculation | Loan Amount: $500,000 Interest Rate: 7.1% Loan Term: 30 years Monthly Payment: $3,360.16 Annual Payment: $40,321.92 |

| Features | – Breakdown of monthly payment into principal and interest. |

| – Annual summary of total payments made. | |

| – Identification of the tipping point in the loan term. | |

| Benefits | – Provides a clear understanding of monthly financial obligations. |

| – Helps in planning long-term finances with an awareness of the shifting balance between interest and principal payments. | |

| – Useful for comparing different mortgage options and interest rate impacts. |

Key Features to Look for in a Mortgage Principal and Interest Calculator

Choosing the right mortgage principal and interest calculator isn’t only about ease of use—it’s about understanding the essential features that will help you make well-informed decisions.

1. Accuracy and Up-to-Date Information

A reliable calculator must pull the latest interest rates and allow for various loan options, like fixed-rate and adjustable-rate mortgages. Accurate inputs ensure your monthly and long-term payments are correctly forecasted, laying a solid foundation for your financial planning.

2. Amortization Schedule

An exhaustive amortization schedule is non-negotiable. It details how each payment impacts your loan’s principal balance over time, giving you a month-by-month breakdown. This feature is crucial for visualizing your loan’s trajectory and planning effectively.

3. Extra Payment Options

Look for calculators that enable extra payments. Being able to input additional contributions shows you how much interest you could save and helps you strategize to pay off your mortgage quicker.

4. User-Friendly Interface

A straightforward, clean interface can make or break a tool’s effectiveness. The last thing you need is to wrestle with a confusing layout when you’re trying to calculate critical financial data.

5. Comprehensive Loan Breakdown

Seek calculators offering detailed breakdowns of each payment component: principal, interest, taxes, and insurance. This transparency helps you plan your budget down to the last detail, ensuring you’re not caught off-guard by unexpected costs.

How to Maximize Your Mortgage Principal and Interest Calculator

To get the most mileage out of your mortgage principal and interest calculator, you need more than just the basics. Here are a few advanced strategies:

1. Scenario Analysis

Run multiple scenarios with different loan amounts, interest rates, and payment terms. This exercise helps you grasp the impact of changing variables and prepares you for multiple financial outcomes. If rates soar or plunge, you’ll be ready.

2. Regular Updates

Interest rates and home prices aren’t static. Revisit the calculator periodically to update your figures. This habit keeps your financial planning current and relevant. A historical view of mortgage interest rates can also be enlightening, showing trends and helping you predict future movements. For more on mortgage rate history, consider checking out mortgage interest rates history.

3. Utilize ‘What If’ Strategies

Use ‘what if’ scenarios to gauge potential savings from making extra payments. This feature can show you how minor adjustments might shave years off your loan term and save you a mountain in interest.

4. Connect with Professionals

The insights you gain from the calculator can form the basis for discussions with mortgage advisors. Armed with data, you’ll be better positioned to ask the right questions and get the best advice on your mortgage journey. For personalized strategies, consult with financial experts linked to Jill Warrick.

Wrapping Up: Making Informed Decisions with Confidence

Choosing the best mortgage principal and interest calculator can significantly influence your journey toward financial clarity and stability. By using the top tools discussed in this review, you can navigate your mortgage landscape with precision and confidence. These calculators aren’t just numbers games—they’re tools for crafting a well-structured financial plan. Embrace these tools, experiment with different inputs, and take control of your financial future today. By leveraging the insights from these calculators, you can approach mortgage advisors with confidence and ensure that you’re making decisions aligned with your financial goals.

Whether you’re a first-time buyer or a seasoned homeowner, making the right choice with a mortgage principal and interest calculator can make a world of difference. Dive in, utilize these resources, and empower yourself to manage your mortgage smarter and more effectively. For additional tools, explore our in-depth mortgage rate calculator, or get specific with our handy mortgage Payments calculator.

So, why wait? Unveil the power of these calculators and set yourself on the path to a secure financial future. By taking proactive steps now, you’re building a foundation that will support you for years to come. Get started today, make informed choices, and step into a brighter financial future with confidence!

Mortgage Principal and Interest Calculator: Fun Trivia and Interesting Facts

Surprising Origins

Did you know that the concept of mortgage principal and interest calculations dates back centuries? While today’s digital tools like a mortgage payment estimator make things a breeze, early homeowners relied on handwritten ledgers and laborious math. Imagine calculating your monthly mortgage payment with just a pen and paper—talk about dedication!

The Calculator Powerhouse

Ever wonder who some of the masterminds behind these mathematical tools are? One notable name is de Guzman, a renowned figure in the financial sector who has contributed to the development of more user-friendly mortgage calculators. Thanks to experts like de Guzman, complicated math is simplified, making homeownership attainable for more people.

Balancing Finance and Life

In our fast-paced world, finding balance is key, and tools like mortgage principal and interest calculators help maintain that balance. Believe it or not, even some of the best short Ted talks touch on how managing finances efficiently can reduce stress and improve life quality. It’s fascinating how such a seemingly mundane tool can unlock better life management strategies.

A Less Known Connection

Interestingly, managing money wisely can also play a role in family dynamics, especially in more challenging situations. For instance, resources like Your child addict You can do discuss the importance of financial stability in supporting loved ones through tough times. The ability to accurately calculate and plan mortgage payments can provide a secure foundation during such times.

In summary, mortgage principal and interest calculators are more than just digital number-crunchers. They are rooted in history, simplified by experts, and their use can even touch lives in unexpected ways.

How do you calculate principal and interest on a mortgage?

To calculate principal and interest on a mortgage, first convert your annual interest rate to a monthly rate by dividing by 12. Then multiply your loan amount by this monthly interest rate to find your monthly interest payment. Finally, subtract your monthly interest payment from your total monthly payment to get your monthly principal payment.

At what year in a 30-year mortgage do you pay more principal than interest?

You begin paying more principal than interest on a 30-year mortgage with a fixed rate of 4% after more than 12 years into the loan. This is known as the tipping point.

How much of my mortgage payment goes to principal?

After the first year of making mortgage payments, 31% of your payment goes toward the principal. By the tenth year, around 45% goes to the principal, and by the twentieth year, about 67% of your payment is applied to the principal.

How much is a mortgage on a $500,000 house?

For a $500,000 mortgage with a 30-year term and a 7.1% interest rate, the monthly payment is $3,360.16. Over a year, this amounts to $40,321.92 in combined principal and interest payments.

Is it better to pay down principal or interest?

Paying down the principal is generally better because it reduces the overall amount of interest you will pay over the life of the loan, which can save you a significant amount of money.

How to calculate loan interest and principal?

By paying an extra $200 a month on your mortgage, you can reduce the principal faster, which will shorten the length of your loan and decrease the total amount of interest paid.

What happens if I pay an extra $200 a month on my mortgage?

Making two extra mortgage payments a year on a 30-year mortgage can significantly reduce the loan term, often by several years, and you’ll pay much less in interest over the life of the loan.

What happens if I make 2 extra mortgage payments a year on a 30-year mortgage?

Extra payments will typically go to the principal unless specified otherwise. Check with your lender to ensure how extra payments are applied.

Do extra payments automatically go to principal?

It’s generally better to put extra money toward the principal rather than escrow. Paying extra on the principal reduces your overall interest burden over the life of the loan.

Is it better to put extra money towards escrow or principal?

Paying extra principal on your mortgage is usually worth it as it reduces the balance owed more quickly and decreases the total interest you will pay over the life of the loan.

Is it worth paying extra principal on mortgage?

If you make a large principal payment on your mortgage, your principal balance reduces, potentially shortening the loan term and saving you a significant amount of interest over time.

What happens if I make a large principal payment on my mortgage?

To buy a $500,000 house, a credit score of at least 620 is typically needed, although higher scores can qualify for better interest rates.

What credit score do you need to buy a $500,000 house?

Predicting interest rates can be tricky, but some experts believe rates could stabilize or decrease slightly in 2024. However, this is speculative and depends on various economic factors.

Will interest rates go down in 2024?

For a $500,000 mortgage, lenders usually require that your monthly house payments (including principal, interest, taxes, and insurance) don’t exceed 28-30% of your gross monthly income, translating to a necessary annual income of around $120,000 to $150,000, depending on other debts.

What income do you need for a $500000 mortgage?

To calculate principal and interest, follow these steps: convert the annual interest rate to a monthly rate by dividing by 12, then multiply this rate by the loan amount for the monthly interest payment, and subtract this interest payment from the total monthly payment to get the principal.

How do you calculate principal or interest?

The formula for calculating monthly mortgage payments involves the loan amount, the monthly interest rate, and the loan term. An online mortgage calculator or speaking with a lender can clarify your specific situation.

What is the formula for the principal of interest?

To determine how much interest you pay each month on your mortgage, take your annual interest rate, divide it by 12 to get the monthly rate, and then multiply your current loan balance by this monthly rate.