Owning a home is like holding the keys to your personal kingdom, but with great castles come great responsibilities—and perhaps the most significant of these is your monthly mortgage payment. It’s not just a simple figure, but a composition of various elements that, when understood, can make the road of homeownership far less daunting. Let’s dive deep into the essentials that encompass the mortgage payment realm, shall we?

Decoding Your Monthly Mortgage Payment: More Than Just a Number

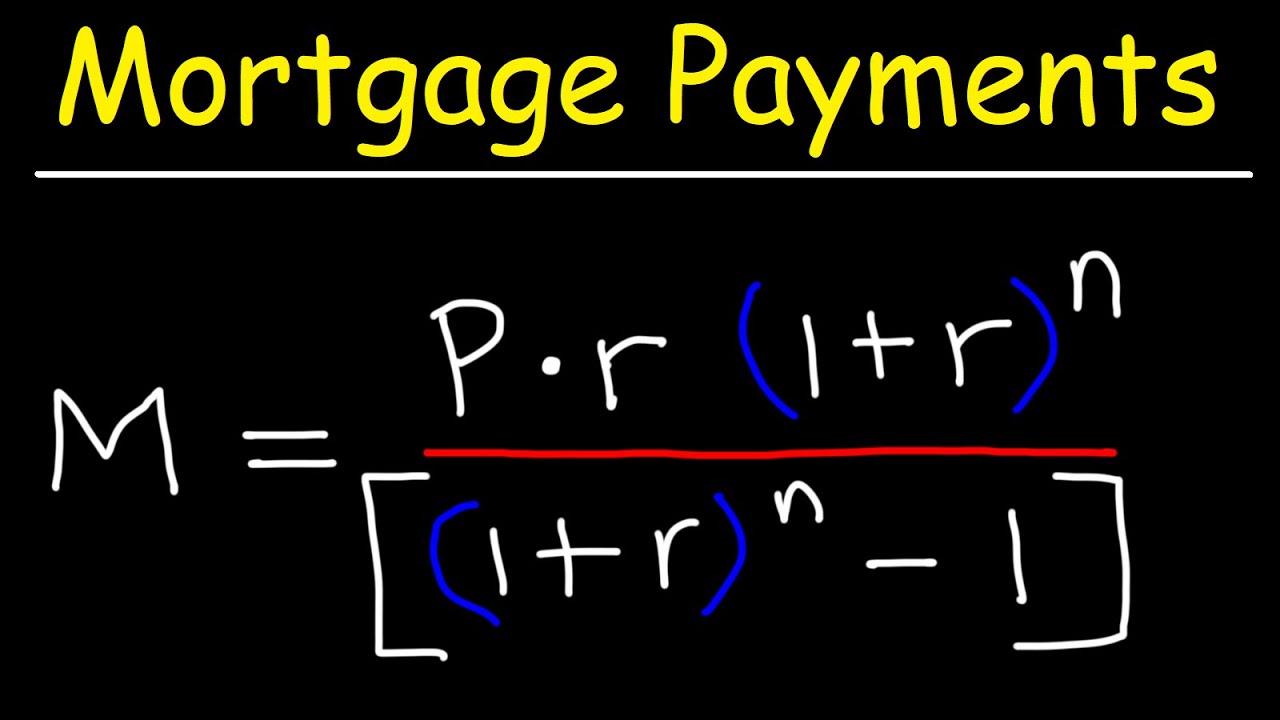

If you think your mortgage payment is a single drop in the financial bucket, think again! It’s actually a cocktail—mixed with crucial ingredients that blend to secure your stay in your humble abode. The typical monthly mortgage payment includes loan principal, loan interest, taxes, and insurance. In simpler terms, imagine your mortgage payment is like a pie, with each slice representing a different cost that’s served on the regular.

Your loan term is like a time machine for your payments—the 15-year vs. 30-year debate is a classic. Here’s the scoop: opting for a 15-year mortgage means a pricier tag on your monthly dues, but over time, you’ll pay less interest and gain full ownership earlier. Punch in a 30-year term, and voilà, your payments shrink, but you’ll pay more in interest over the long haul.

Interest rates can make or break your monthly dues—they’re the bosses of the payment world. How so? Let’s paint a picture: snag a $300,000 mortgage at a 6% APR, and we’re talking about $2,531.57 monthly for 15 years. Choose a 30-year plan, and you’re looking at $1,798.65, exclusive of the escrow ensemble that hops onto your bill, which varies based on where your castle sits and who’s got it covered.

The Inescapable Reality of Interest Rates on Mortgage Payments

Ever wondered about the wizardry behind interest rates? It’s not just market whims—they’re calculated with a combo of national economic trends, your financial story, and a pinch of lender’s secret sauce. It’s like knowing the recipe can help you serve up the best deal on your plate.

Take a trip down memory lane, and you’ll spot how interest rates and mortgage payments have been doing the tango over time. The dance has had its ups and downs, and savvy homeowners track the rhythm to snap up rates when they hit the right note.

To lock in that golden rate, it’s all about timing and a tight grip on your credit, darling. It’s the ace up your sleeve that makes future payments predictably pleasant. Ever heard of a mortgage note? Think of it as your autographed agreement to repay the loan, which turns sweeter with a dandy interest rate.

| Component | Description | Example Calculation (15-Year Loan) | Example Calculation (30-Year Loan) | National Averages (2023) |

|---|---|---|---|---|

| Loan Principal | The amount of money you’re borrowing to pay for the home. | $300,000 / 180 months | $300,000 / 360 months | Average mortgage amount varies by region. |

| Loan Interest | The cost you pay to the lender for borrowing the principal. | 6% APR on $300,000 | 6% APR on $300,000 | Average APR rates change with the market. |

| Property Taxes | Local taxes charged by your municipality or county. | Varies by location | Varies by location | Often calculated as a percentage of the home’s assessed value. |

| Homeowners Insurance | Insurance covering possible damage to your property. | Varies by location and insurer | Varies by location and insurer | Average costs differ by state and home value. |

| Monthly Payment | Total sum of the above components | $2,531.57 | $1,798.65 | National average is $1,768; median is $1,532 (excludes escrow). |

| Escrow | An account held by the lender containing funds for taxes and insurance | Varies by escrow requirements | Varies by escrow requirements | Varies heavily based on home’s location and associated costs. |

Escrow Accounts: The Unsung Heroes of Mortgage Payments

Raise a toast to the underrated stars of the mortgage show—escrow accounts! They quietly safeguard your back, ensuring that property taxes and homeowner’s insurance don’t rain on your parade.

So how does this unsung hero get its number? Your lender peeks into the future, estimates your tax and insurance bills, and then divides that by twelve. Some years your escrow plays perfect pitch, but others it’s like an orchestra out of tune, and adjustments must be made, either in your wallet’s favor or otherwise.

The Yin and Yang of escrow accounts boil down to this: they impose discipline—no late fees haunting your dreams. However, it could cramp your style if you prefer handling your money solo—it’s about weighing what’s sweet and what’s sour for you.

Early Mortgage Payment Strategies and Their Long-Term Impact

Fancy slashing years off your mortgage commitment and saving a truckload of cash in interest? Early payment plans might just be your financial superpower.

Here’s the lowdown: jazz up your mortgage jam with extra payments—the potential savings are huge! You can strut down the bi-weekly path, a little sleight of hand that essentially sneaks in one extra payment a year; or you could go all out with lump-sum payments—big, bold, and downright impactful.

Real-life stories are like nuggets of wisdom. Imagine knocking a few years off the mortgage calendar and having enough dough to swing into retirement like a champ. That’s the power of paying extra—a story worth telling at your housewarming bash.

Navigating Mortgage Payment Changes and Challenges

Now, don’t think the mortgage road is always smooth. There are potholes, my friend—adjustments from those pesky ARMs, tax hikes, and shifts in insurance costs.

To keep your financial ship afloat when these waves come crashing, you’ve got to wear the captain’s hat. Stash some cash for a rainy day, and keep a weather eye on the horizon for any changes that could tweak your mortgage payment. It’s wise to be ready to adjust your sails.

Should a storm hit and catching up with payments becomes tougher than a two-dollar steak, know that options exist for homeowners in distress. There are safety nets woven by lenders and government programs designed to catch you before you fall.

Conclusion: Mastering Mortgage Payments for Financial Success

So, there you have it—the five key notes to the mortgage payment symphony. Remember, your monthly slice isn’t just a number; it’s as intricate as a four-layer cake. Crunch those rates and scoop a deal that’s sweeter than your grandmother’s apple pie. Fluff your escrow knowledge like a seasoned financial chef, and cook up a plan to pay early, reaping savings as rich as a fudge brownie.

Use this wisdom to spin the wheels of informed decisions and build a strategic plan that’ll cement your footing on the property ladder. You’re not just a homeowner—you’re the commander of your financial future. Harness these insights and let them guide you toward long-term stability and the joy of shaping a space that’s truly your own.

And whenever you feel like browsing for some tech upgrades for your new castle or need a little boost of motivation, remember that a world of resources, like the latest in tech & gear or a hearty serving of inspirational Quotes, is just a click away. Maybe, on a lighter note, explore the weird Barbie phenom or indulge in some lit erotica audio as a cheeky reward after number-crunching those payments. And when you need to reconnect with your mortgage matters, simply hop onto your Nbkc mortgage Login and be the maestro of your mortgage once again.

Understanding the nuances of your mortgage payment isn’t just about keeping a roof over your head—it’s choreographing the dance for your future’s security. Let the rhythm of knowledge guide you, and may your homeownership journey be as rewarding as the dreams that built it.🏡

Unwrapping the Mystery of Your Mortgage Payment

Did You Know? It’s Not Just Principal and Interest!

When we talk about a mortgage payment, you might think it’s as straightforward as paying back what you borrowed, plus a little extra for the bank’s trouble, right? Well, hold your horses! There’s a bit more to it than just that. Sure, you’ve got your principal – that’s the chunk of change you borrowed to buy your humble abode. Then, there’s interest, the lender’s way of saying, “Thanks for borrowing our dough.” But wait, there’s more! Your payment often includes things like taxes, insurance, and sometimes even homeowners association fees. So every month, you’re not just chipping away at what you owe; you’re also taking care of the nitty-gritty details that keep your home sweet home truly yours.

A Point in the Right Direction

Alright, so you’ve heard about mortgage Points, but do you know how they fit into the grand scheme of your mortgage payment? Imagine you’ve got a fairy godmother who, instead of turning pumpkins into carriages, gives you the chance to lower your interest rate. That’s kind of what paying for “mortgage points” is like. It’s upfront cash that you can fork over to snag a lower interest rate, which can save you a bundle over the life of your mortgage. Dive deeper into the world where points aren’t just for games with a peek at how mortgage points( can make a major play in managing your mortgage payment.

Amortization: Not as Scary as It Sounds

Now, here’s a word that might send shivers down your spine: amortization. Sounds like something out of a boring math textbook, right? But hold your ponies, because understanding this can save you from a lot of head-scratching. Amortization is just a fancy term for the schedule that shows you how each mortgage payment chips away at your debt over time. In the beginning, it’s a slow dance with interest taking the lead. But as time ticks on, you and your principal start to tango, with more of your payment attacking the amount you borrowed.

The Early Bird Gets the Savings

Ever heard the phrase “the early bird catches the worm”? Well, in the mortgage world, the early bird gets the savings! If you make your mortgage payment before the due date, you strut to your own beat – you’re actually reducing the amount of interest you’ll pay over the loan’s lifespan. And if you’re feeling extra snazzy, throwing in an extra payment now and then (make sure it goes toward the principal) can have you doing the financial freedom dance years ahead of schedule.

Break It Down Now!

Hang tight, because we’re about to break it down – your mortgage payment, that is. Did you know you could potentially make bi-weekly payments instead of the standard monthly ones? Yup, you heard that right. By splitting your monthly payment in half and paying it every two weeks, you sneak in an extra payment each year. That’s right, 26 half-payments add up to 13 full ones. And what does that mean for you? You could shave years off your mortgage and save a pretty penny on interest. Talk about a smooth move for your wallet!

So there you have it – the scoop on your mortgage payment, served up with a side of trivia and a dollop of strategy. By understanding the ins and outs of what goes into that monthly charge, you can dance your way to mortgage mastery and potentially big savings. Keep strutting your savvy stuff, and you’ll be on your way to owning your piece of the American Dream outright! 🏠💃🕺

What mortgage payment means?

Alrighty, let’s crack these down one at a time!

What is mortgage payment on 400 000?

What mortgage payment means?

Well, in a nutshell, a mortgage payment is the bread and butter of homebuying; it’s the regular installment you shell out to the bank or mortgage lender for the cash they fronted you to snatch up your digs. It’s usually a monthly affair that includes part of your loan’s principal, interest, taxes, and sometimes even insurance!

How much is a typical mortgage payment?

What is mortgage payment on 400 000?

Oh boy, dive into the numbers and you’ll see that a mortgage payment on a $400,000 loan can vary wildly. It depends on your interest rate, loan term, and down payment. But let’s say you’ve landed a 30-year loan at 4% interest; you could be staring at a monthly mortgage payment around $1,900, give or take.

How much is a mortgage on a 300k house?

How much is a typical mortgage payment?

Talk about a loaded question! The “typical” mortgage payment is like a chameleon, always changing colors based on loan size, location, and interest rates. In the US, you might see averages hovering around $1,500 a month, but as we all know, average doesn’t always mean typical for everyone.

What happens if I pay an extra $600 a month on my mortgage?

How much is a mortgage on a 300k house?

For a $300k house, your mortgage payment’s gonna be riding on factors like interest rates, down payment, and loan term. To throw a ballpark figure your way, if we’re talking a 30-year term at 4% interest, you might be dangling a carrot of around $1,400 monthly.

Do you pay mortgage monthly?

What happens if I pay an extra $600 a month on my mortgage?

Whoa there, moneybags! Toss in an extra $600 monthly on your mortgage and you’re not just chipping away at the iceberg – you’re torching it! You’ll payoff your loan faster, slash the total interest paid, and be doing the mortgage-free happy dance sooner.

What house can I afford on 70K a year?

Do you pay mortgage monthly?

Yup, in most cases, you’ll be on the hook monthly for your mortgage payment. It’s like a monthly subscription to your very own home sweet home, minus the free trials and easy cancel button!

How much do you need to make to afford a $300 K house?

What house can I afford on 70K a year?

So, on a $70K yearly income, the house you can afford does the limbo under a few bars – debt, expenses, mortgage rates, and more. If we play by the rule of thumb, which says to not go over 3 times your annual income, you’re probably house hunting in the $210K range.

How much house can I afford if I make $120 000 a year?

How much do you need to make to afford a $300 K house?

To afford a $300K house without breaking the piggy bank, you’ll wanna be raking in around $60K – $70K a year. Of course, this depends on debts and other pesky expenses but generally, keeping your mortgage payments below 28% of your monthly income is the goalpost to shoot for.

Why are mortgage rates so high?

How much house can I afford if I make $120 000 a year?

Raking in $120,000 a year? Nice! You could typically afford a house that’s up to $360,000 to $480,000, sticking to the tried-and-true income rule of thumb. Just remember, the devil’s in the details of your debt-to-income ratio and other fun financials.

Can I buy a house making 40k a year?

Why are mortgage rates so high?

One word: inflation. When the cost of living shoots through the roof, the peeps at the Fed get antsy and hike up interest rates to cool things off. It’s a cocktail of economic factors that can sometimes leave us feeling a bit stiffed by the mortgage rates.

What’s the average mortgage payment 2023?

Can I buy a house making 40k a year?

Absolutely! If you’re making $40k a year, you’re not out of the homebuying game. Just keep your eyes peeled for a house that fits snugly into your budget, which might be somewhere in the $120k ballpark, factoring in debt and other monthly expenses.

What credit score is needed to buy a $300 K house?

What’s the average mortgage payment 2023?

In 2023, we’re all over the map, but if we had to pin down an “average” mortgage payment, it would be waltzing somewhere around $1,500 to $2,000. However, with interest rates doing a tango recently, it’s best to keep a keen eye on current trends.

What credit score do I need for a 300000 mortgage?

What credit score is needed to buy a $300 K house?

Aiming for that $300K house? You’ll want a credit score that’s humming a tune of at least 620 to get a traditional loan. But if you’re dreaming of the best rates, shoot for a score that’s crooning in the 700s.

How to pay off 300k mortgage in 5 years?

What credit score do I need for a 300000 mortgage?

To grab a $300,000 mortgage, lenders generally want to see your credit score singing at a 620 minimum. But for the sweetest deal, you’re aiming for a credit score that’s hitting those high notes above 700.