Achieving a balanced monthly mortgage payment is key to financial stability and long-term homeownership success. In this comprehensive guide, we’ll explore factors influencing monthly mortgage payments, effective strategies for managing them, and compare top mortgage providers to aid your decision-making.

Understanding Your Monthly Mortgage Payment in 2024

Your monthly mortgage payment is more than just a recurring bill; it’s the cornerstone of your financial journey as a homeowner. With the national average monthly mortgage payment hitting $2,390, understanding the intricacies of this pivotal expense is crucial. Roughly 51% of homebuyers are now grappling with mortgage payments of $2,000 or more, a significant jump from just 18% two years ago. As daunting as this may seem, we’re here to offer actionable tips to help you manage and optimize your monthly payments effectively.

Top 7 Strategies to Optimize Your Monthly Mortgage Payment

1. Choose the Right Mortgage Term

The term of your mortgage dramatically impacts your monthly payments. A 30-year fixed-rate mortgage, for instance, might spread payments over a longer period, making each installment lower compared to a 15-year term. On the downside, you’ll end up paying more interest over time with a longer term. Conversely, a shorter term means higher monthly payments but less interest paid over the life of the loan. For instance, on a $400K mortgage with a 7% fixed rate, a 15-year loan requires a $3,595 monthly payment, whereas a 30-year loan demands $2,661 monthly.

2. Lock In a Low Interest Rate

Interest rates fluctuate based on market conditions, significantly affecting your monthly mortgage payment. Locking in a low fixed interest rate can save you thousands over the life of your loan. Compare offers from leading lenders to ensure you get the best deal available. Securing a favorable rate is essential for minimizing your monthly payment.

3. Make a Larger Down Payment

A higher down payment reduces your principal loan amount, subsequently lowering your monthly payments. For example, paying 20% down on a $300,000 home reduces the loan size to $240,000, cutting the interest you’ll pay over the years. It can also eliminate the need for private mortgage insurance (PMI), further reducing your monthly burden.

4. Consider an Adjustable-Rate Mortgage (ARM)

An ARM offers lower initial interest rates and payments compared to fixed-rate mortgages. However, these rates can fluctuate after the initial period, potentially increasing your payments down the line. If you plan to sell or refinance before the adjustable period begins, an ARM could be a strategic choice. It’s a gamble, but one that might pay off if you navigate it wisely.

5. Improve Your Credit Score

Lenders reward high credit scores with lower interest rates, thereby reducing your monthly payment. Review your credit report for discrepancies, and make timely bill payments while reducing outstanding debt. Over time, these efforts can significantly enhance your credit score, translating into lower monthly mortgage payments.

6. Refinance Your Mortgage

Refinancing involves replacing your existing mortgage with a new one, often at a lower interest rate. This can reduce your monthly payments and potentially provide better loan terms. Evaluate offers from various lenders to find the best refinancing options that suit your needs.

7. Utilize Mortgage Calculators and Tools

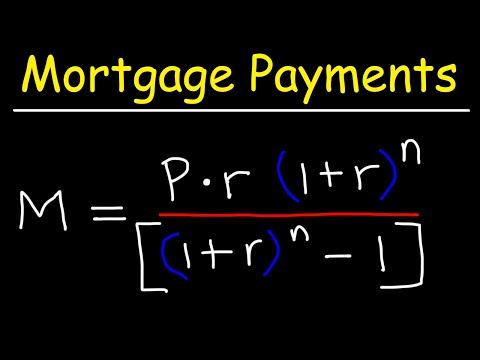

Leverage mortgage calculators to estimate your monthly payments, taking into account loan amounts, interest rates, and terms. These tools can provide a clearer understanding of your financial commitment and help you make informed decisions. For instance, use this monthly mortgage calculator to get a precise estimate of your payments.

| Category | Details |

| National Average | $2,390 per month (excluding property taxes and insurance) |

| Distribution of Payments | – 51% of homebuyers have payments of $2,000 or more |

| – Nearly 25% have payments above $3,000 | |

| Example: $400K Mortgage | 15-Year Loan @ 7% Fixed Rate: $3,595 per month |

| 30-Year Loan @ 7% Fixed Rate: $2,661 per month | |

| Affordability | With a $2,000/month budget, you may qualify for a home priced between $250,000 and $300,000 |

| Additional Costs | Property taxes and insurance are additional costs not included in the base mortgage payment |

| Market Trends | – Monthly mortgage payments have significantly increased from 2021 to 2023 |

| – Higher percentage of buyers now facing larger payments |

Factors Affecting Your Monthly Mortgage Payment

Property Taxes and Homeowner’s Insurance

Beyond principal and interest, property taxes and homeowner’s insurance significantly impact your monthly payments. Locations with high taxes, such as New Jersey, contribute to higher payments, while states like Alabama pose minimal tax impacts. It’s essential to factor in these costs when budgeting for your new home.

Private Mortgage Insurance (PMI)

For conventional loans, PMI protects lenders when down payments are less than 20%. Calculating PMI costs and exploring ways to eliminate this premium as your equity increases can save you between $70 and $150 monthly. A higher initial down payment or reaching 20% equity can help eliminate PMI sooner.

Escrow Accounts

Many lenders require escrow accounts to cover taxes and insurance. While this ensures timely payments and prevents large annual bills, it also ties up part of your monthly payment. If you’re financially disciplined, consider options without escrow, freeing up monthly cash flow for other uses.

Comparing Monthly Mortgage Payment Plans: Real Examples

Quicken Loans (Rocket Mortgage)

With competitive fixed-rate and adjustable-rate offerings, Quicken Loans tailors mortgages to individual needs. Their streamlined online application and robust customer support make them a favorable choice for many.

Wells Fargo

Wells Fargo provides diverse loan products, including fixed, ARM, and jumbo loans. Their My Mortgage Gift program offers rewards, which can positively impact overall homeownership costs and monthly payments.

Bank of America

Bank of America caters well to various borrower profiles with versatile loan options. Preferred Rewards clients benefit from reduced origination fees and rate discounts, aiding in monthly payment affordability.

Chase

Chase’s comprehensive mortgage services feature rate discounts for existing customers, no set-up fees, and autopay discounts. Their user-friendly mobile app improves monthly payment management.

Beyond the Payment: Building a Strong Financial Foundation

While focusing on your monthly mortgage payment is critical, broader financial planning is equally important. Set aside emergency funds, aim for retirement savings, and maintain a balanced budget. This holistic approach fortifies your overall financial health and ensures long-term stability.

The Blueprint to an Affordable Monthly Mortgage Payment

Emparking on the right mortgage path in 2024 involves evaluating various strategies and lender options. By understanding loan terms, interest rates, credit scores, and using insightful tools, you can achieve manageable and predictable monthly payments. Remember, your monthly mortgage payment isn’t just a number; it’s a cornerstone of your homeownership journey. Make informed decisions today for a secure tomorrow.

To get started, check out our monthly mortgage payment calculator for tailored insights specific to your financial situation. Embrace these tips and strategies to navigate the mortgage landscape confidently in 2024.

Discover Fun Trivia and Interesting Facts About Monthly Mortgage Payments

The Origin of Monthly Payments

Ever wondered who kicked off the trend of monthly mortgage payments? It might surprise you that the idea of structured, monthly payments traces back centuries. Originally, properties were often sold with lump sum payments, which wasn’t too practical for most. Over time, lenders realized spreading payments out allowed more people to become homeowners. This nifty twist shifted the landscape and made property ownership much more accessible. For an interesting dive into the minds that shape our understanding of mortgages today, check out how Thomas Ray Gosling has influenced mortgage practices.

Beyond the Numbers: Fun Tidbits

Calculating that perfect mortgage plan can sometimes feel like a high-stakes puzzle. Did you know that an estimated 2 out of 5 people find computing their monthly payments more stressful than a high school math exam? If you’re in the majority who get jitters just thinking about interest rates and amortization schedules, using a handy monthly house payment calculator takes the guesswork out of the equation. It’s like having a pocket-sized financial advisor!

Quirky Facts That Surprise

Here’s a quirky tidbit: the name “mortgage” comes from Old French, meaning “death pledge.” No, it’s not as grim as it sounds! It simply reflected the idea that the pledge ends (dies) when the debt is fully paid or the property is taken away through foreclosure. Speaking of pledges, the Niswonger fund has been a beneficial touchstone for many seeking financial stability through sound mortgage options, making intricate financial dynamics a bit more navigable.

Tying It All Together

So you’re prepping for the journey of buying a home; a simple house design might be just what you need. Investing in properties doesn’t have to be overwhelming, especially when you’ve got resources to simplify the process. Tools like a simple house design( guide align with managing affordable mortgage plans. Didn’t catch that one? Helps plan the layout and finances in one go!

Taking these fascinating elements together makes the story of monthly mortgage payments not just numbers on a page but a vibrant thread in the tapestry of modern homeownership. Whether you’re new to the home-buying game or just love an engaging trivia detour, the history, tools, and quirks behind those monthly entries on your bank statement have a tale worth telling. And well, if mortgage talk ever feels too stiff, remember diversions like comparing Adderal Vs meth or a dramatic read about a shot out 4 can add a little spice to your day!

What is a typical mortgage payment per month?

The average mortgage monthly payment in 2023, without including property taxes and insurance, is $2,390. Keep in mind that half of all homebuyers pay $2,000 or more every month, which is a significant jump from recent years.

Is $2,000 a month mortgage high?

A $2,000 monthly mortgage payment isn’t considered high anymore. Around 51% of homebuyers face payments of $2,000 or more each month, so you’re right in the middle of the pack.

What is the monthly payment on a $400,000 mortgage?

For a $400,000 mortgage, if you have a 7% fixed rate, your monthly payment would be $3,595 on a 15-year loan or $2,661 on a 30-year one. Remember, these amounts don’t include insurance or property taxes.

How much is a $2000 a month mortgage?

With $2,000 a month to spend on your mortgage, you can likely afford a home priced between $250,000 and $300,000. Other financial factors will affect your exact budget too.

Is $3,000 a high mortgage payment?

A $3,000 mortgage payment is relatively high, but many homebuyers are paying these amounts. In fact, nearly a quarter of homebuyers have payments over $3,000.

What is a good monthly payment for a house?

A good monthly payment for a house should fit into your overall budget without causing financial strain. Most experts recommend that your mortgage payment not exceed 28% of your monthly income.

How much house can I afford if I make $70,000 a year?

With a $70,000 annual salary, you can probably afford a home priced between $250,000 and $300,000, assuming a reasonable down payment and other debts.

How much house can I afford if I make $90000 a year?

Earning $90,000 a year, you might be able to afford a home between $300,000 and $400,000. This range depends on things like debt, down payment, and interest rates.

How much house can I afford if I make $45000 a year?

Making $45,000 a year, you might afford a home priced around $150,000 to $200,000. Don’t forget to account for other payments like insurance and property taxes.

How much income do you need to qualify for a $400000 mortgage?

To qualify for a $400,000 mortgage, a good rule of thumb is that you need an annual income between $90,000 and $100,000, depending on your debt and credit score.

How much income do you need for a 350K house?

For a $350,000 house, an annual income in the range of $80,000 to $90,000 should be enough, though individual financial situations will vary.

How much house can I afford with $10,000 down?

With $10,000 down, the amount of house you can afford depends heavily on your income and monthly expenses. Generally, you can afford more house with a larger down payment, but you might be looking around $100,000 to $150,000.

How much house can I get for $1500 a month?

For a monthly mortgage payment of $1,500, you may be looking at homes priced between $150,000 and $200,000, depending on the loan terms and interest rates.

How much house for $3,500 a month?

With $3,500 to spend monthly on your mortgage, you can afford a more expensive home, possibly between $500,000 and $600,000, depending on the loan conditions and your other expenses.

What income do you need for an $800000 mortgage?

For an $800,000 mortgage, you’d typically need an annual income around $180,000 to $200,000, keeping in mind this can fluctuate based on down payments, credit scores, and other debts.