The financial world has been thrown into a tizzy! Why, you ask? Well, the Libor rate, that old staple of the finance industry, has been making some waves – and not the kind you’d want to surf on. Buckle up, because we’re about to take a wild ride through the nitty-gritty of the Libor rate’s tumultuous impact on the world of finance.

Unpacking the Libor Rate: An Overview

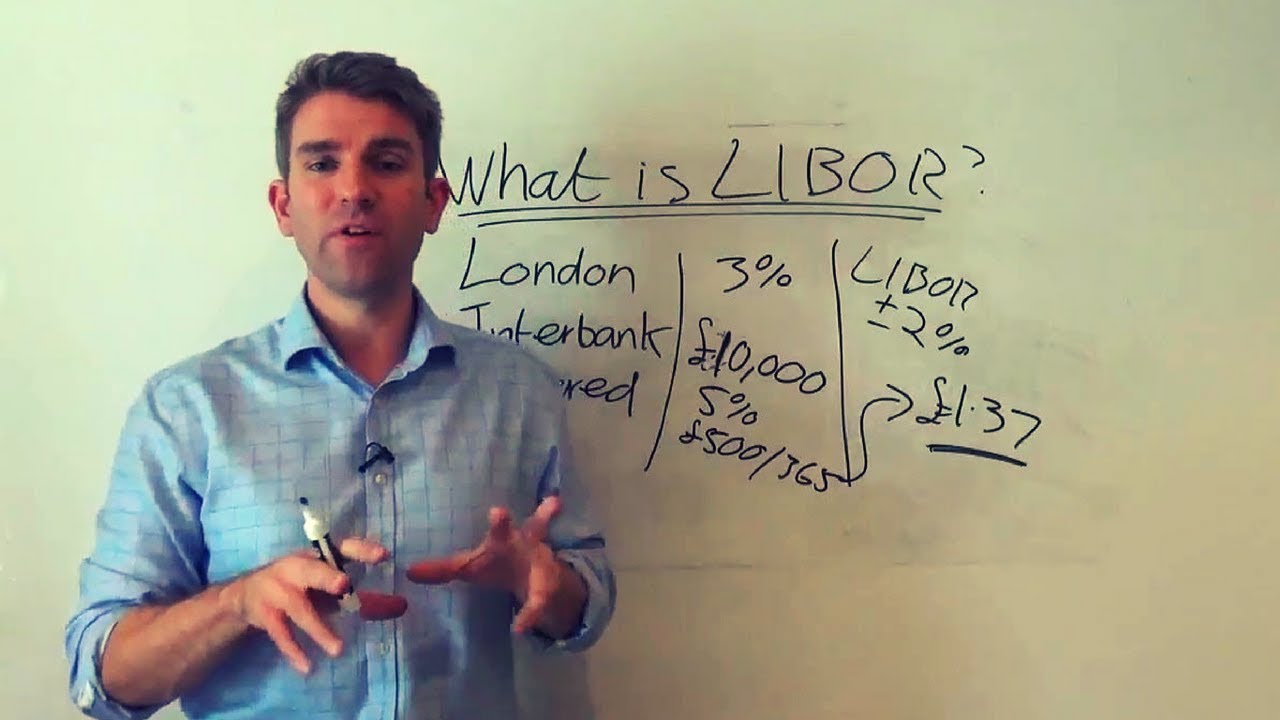

Let’s hit the rewind button and take it from the top. The Libor – or the London Interbank Offered Rate, for those who like to spell it out – has long been the gossip queen of the financial prom. One of the world’s most vital interest rates, the Libor was the go-to for banks setting out on their daily borrowing escapades.

The Libor rates, which include a plethora ranging from 1 Month LIBOR Rate at 4.73, to the 1 Year LIBOR Rate at 4.99, are more than just numbers; they’re stitched into the very fabric of global finance. Banks whispered their loan secrets to each other, and voilà, we’d get the average – more often than not, referred to in the singular even though there were 150 of them.

But wait, there’s more! The Libor also had this knack for showing up almost everywhere in finance, from mortgages to the mountainous world of corporate borrowing. Oh yeah, it was a big deal, alright – until it wasn’t.

The Rise and Fall of Libor Rates

Like a chart-topping hit, Libor rates once ruled the financial airwaves. That is, until they hit a tune no one wanted to hear – the rigging scandal. This earth-shattering revelation sent shockwaves through the financial industry, much like the impact of Elvis Presley in the world of rock ‘n’ roll. Banks had been fiddling with the figures, and wouldn’t you know it, that just doesn’t sit well with anyone.

The aftermath? A slick transition from Libor to alternatives like the SOFR – which you can check at Sofr rates today. It’s like swapping out your worn-out boots for a shiny new pair from Boot Barn. But this wasn’t just any old switcheroo; the implications were massive.

| Attribute | Details |

|---|---|

| Full Name | London Interbank Offered Rate (LIBOR) |

| Current 1 Month Rate | 4.73% |

| Current 3 Month Rate | 4.94% |

| Current 6 Month Rate | 4.97% |

| Current 1 Year Rate | 4.99% |

| Nature | Average of interest rates at which banks offer to lend unsecured funds |

| Importance | Benchmark for short-term interest rates worldwide |

| Cessation Date for USD | After June 30, 2023 |

| ‘Representative’ Status | Will no longer be considered ‘representative’ after May 30, 2023 |

| Criticisms | Manipulation, scandal, methodological issues |

| Replacement | Secured Overnight Financing Rate (SOFR) |

| Transition Date | June 30, 2023 |

| Historical Significance | Once a primary benchmark for short-term interest rates |

The Global Economy Post-Libor: An Analysis

Post-Libor, the world’s economies were like ‘now what?’ The United States said hello to SOFR, while Europe and Asia gave a big wave to their own new benchmarks. It was a mixed bag, really, like comparing the new rates to the old Libor ones was like looking at your iPhone trade-in value: exciting possibilities, but also a twinge of nostalgia for what was.

The Real Estate Turmoil Triggered by Libor Fluctuations

Let’s get real – when Libor rates went haywire, so did your Aunt Sally’s mortgage rates. You see, jumps in the Libor could send the housing market into a funk, kind of like when Disney announced Splash Mountain closing – unexpected and a bit chaotic.

But here’s the scoop: Industry gurus spilled the beans on the long-term drama caused by the Libor phase-out. Bracing for that impact was no Sunday picnic, I tell you.

The Corporate Debt Rollercoaster: Libor’s Influence

Big Corp Inc. had its days of wine and roses when Libor rates played nice. But when they didn’t? Let’s just say the corporate debt went on a rollercoaster that no one had the stomach for. Companies had to get creative, rewriting their playbooks to manage debts without the trusty Libor by their side.

Consumers at the Mercy of Libor Rates: A Deep Dive

Okay, here’s where it hits home. Imagine your student loan or that shiny credit card tethered to the whims of Libor. When the rate danced, so did your payments – not quite the dance party anyone signed up for.

But people got by, adapting to the shift from Libor like champions. They’ve got stories that could fill a book, ones that show just what it’s like when the financial rug gets pulled out from under you.

Banks and Financial Institutions Navigating the Libor Rate Transition

The big banks, like JPMorgan Chase and Barclays, had to shake up their systems faster than you could say What Does ops mean in text. They dove headfirst into the deep end of financial adaptation, all while the regulators circled like seagulls, ready to swoop in with policies and oversight that promised smoother skies ahead.

Libor’s Legacy and Lessons Learned for Future Financial Benchmarking

If nothing else, the Libor saga taught us a thing or two. Like making sure the financial market backbone – those oh-so-crucial benchmark rates – are transparent and fair. It’s all about integrity, folks, and steering clear of murky waters. A lesson learned, indeed.

The Tech Revolution in Finance: How Fintech Is Addressing the Libor Gap

Enter fintech, our knight in shining digital armor. These wiz kids are doing for finance what Jetpacks did for personal travel – propelling it into the future. They’re filling the Libor void with all sorts of fancy new tools and gadgets, reshaping what we thought we knew about financial products.

Markets in Transition: The Investment Landscape Without Libor Rates

Oh, and if you’re wondering how the stock market’s faring without good old Libor, well, it’s been a ride. Immediate impacts have jostled portfolios, but long-term? It’s like a new season in finance, with investment banks like Goldman Sachs and Morgan Stanley charting the course through these choppy, Libor-less waters.

Conclusion: The Future of Finance in a World Without Libor Rates

Looking back, the Libor debacle was a slap to the finance world’s face – a wake-up call to do better. Finance has adapted, sure, but it’s also morphed into a wild beast of its own making, filled with opportunities and challenges that would give the boldest of us pause.

Adjusting to a benchmark-less reality involves vigilance and adaptability, much like staying on top of real estate legalese (tip: catch up on Respa real estate or the truth in lending act for some reading pleasure). Our military folks have their backs covered with the service Members civil relief act, but all of us in finance? We’ve got to steer this ship together, with clear eyes and a full heart, ready to embrace the new finance frontier that awaits us.

The Unseen Waves of the Libor Rate

Well, here’s the scoop: the Libor rate isn’t just some stuffy financial term that makes you zone out faster than your phone loses value after a new release. Nope, this little acronym stands for the London Interbank Offered Rate, and let me tell you, it’s got its fingers in more pies than your grandma at Thanksgiving.

A Spicy Bit of History

Now, hold onto your hats, because the origin story of the Libor rate is spicier than a jalapeño. Way back in the ’80s, before everyone and their mom had an iPhone, banks needed a way to determine the interest rates for loans between each other. Enter Libor, the financial world’s answer to “How much is it gonna cost to borrow your dough?” It quickly became the go-to benchmark for everything from mortgages to student loans.

What’s in a Number?

But here’s where it gets dicey. Banks would call each other up, all casual-like, and ask, “Hey buddy, if I needed to borrow some cash, what’s the damage?” This chummy system was all based on trust—like swapping out your old phone for cash, you gotta trust you’re getting the right Iphone trade in value. Turns out, sometimes that trust got as bent as a spoon at a magician’s convention.

The Ripple Effect

Just when you thought this Libor rate thing couldn’t impact your life more than a viral cat video, think again! That tiny percentage influences trillions—yeah, with a ‘T’—of dollars in loans and financial products. It’s like when you’re trading in your iPhone; that rate determines if you’re walking away feeling like a champ or like you just lost a game of Monopoly.

More Power Than You’d Think

Okay, here’s a wild fact for you: the Libor rate had so much sway, it could mess with entire economies. I’m not just talking about a little hiccup—I mean full-blown “hold onto your hats and glasses” kind of turbulence. Just a teeny tweak in the Libor rate could mean the difference between splurging on that shiny new gadget or clutching your old phone tight, praying for a better trade-in value next time.(

And there you have it—the lowdown on the Libor rate and its shocking impact on our wallets and world. Sure, it might sound like just another bit of banker babble, but this bad boy pulls more strings than a puppeteer at a kids’ party. Keep your eyes peeled, because with Libor’s influence, you never know what might fluctuate next—just like the unpredictable resale value of your trusty iPhone.

What is current Libor rate?

– Hold your horses, the current Libor rate changes daily! You’re better off checking the latest financial reports or databases for the most up-to-date figures—these pesky numbers love to play hide and seek with investors!

What does LIBOR mean in finance?

– Ah, LIBOR! It’s like the financial world’s North Star, guiding the way. Standing for London Interbank Offered Rate, it’s what banks charge each other for short-term loans. It’s the big cheese in the world of interest rates, influencing everything from mortgages to student loans.

Is LIBOR going away in June 2023?

– Yep, you heard right! LIBOR’s taking a bow in June 2023. It’s set to hand over the reins to alternative rates after a long innings of steering the ship in the global financial markets.

Is Libor rate still used?

– Is the Libor rate still used, you ask? Well, it’s clinging on by its fingertips! While it’s not as popular as it once was, some loans and contracts are still dancing to its tune until it takes its final curtain call.

What is the difference between LIBOR and SOFR?

– If LIBOR and SOFR had a face-off—picture this: LIBOR’s the old-school lender in town, guessing rates over a cup of joe, while SOFR’s the new kid, crunching real transaction numbers. SOFR, short for Secured Overnight Financing Rate, is backed by cold hard cash deals and is less likely to cause a scene with rate manipulations.

Is LIBOR the same as interest rate?

– Is LIBOR the same as interest rate? Well, that’s like asking if a square is the same as a rectangle. LIBOR is an interest rate, but not all interest rates are LIBOR. It’s the big shot in a world full of interest rate players.

Why LIBOR is being discontinued?

– The curtain’s closing on LIBOR because it’s had a bit of a dark past, with some naughty banks messing with the rates. So the financial honchos decided it’s time for a cleaner, more reliable system. Out with the old and in with the new!

What is the highest Libor rate ever recorded?

– What’s the highest LIBOR rate ever recorded, you wonder? Back in the techie ’80s—1989 to be exact—LIBOR skyrocketed to a dizzy 11%. Those were wild times for the rate raconteurs!

Why is the Libor rate so high?

– Why is Libor rate so high, you ask? Well, it’s like a weather vane for bank trust issues. When banks get jittery about lending dough to each other, up goes LIBOR like a rocket. It’s all about confidence… or the lack thereof!

Who decides Libor rates?

– Who decides Libor rates, you might be pondering? A bunch of big-shot banks in London throw their two cents into the mix every morning. They say what they’d charge to lend out their loot, and voila! The daily Libor rate is born.

What will replace the USD Libor rate?

– As LIBOR takes its final bow, SOFR’s gearing up to take center stage in the USD corner. It’s like switching from a gas guzzler to an electric car—smoother and better for the environment… financially speaking, that is!

What is prime rate today?

– What’s the prime rate today, you’re wondering? Well, that’s a sticky wicket! The prime rate is also a bit of a chameleon, changing at the drop of a hat. A quick look at the latest financial news should give you the skinny.

What happens to my arm when LIBOR goes away?

– If you’re worried about your ARM when LIBOR goes into retirement—keep your shirt on! It’ll likely switch to a new index like SOFR. Just keep an eye on your loan agreement, and chat with your lender for the game plan.

What is the difference between LIBOR and prime rate?

– LIBOR vs. prime rate—is like comparing apples and oranges. The prime rate is what banks charge their best customers, while LIBOR’s what banks charge each other. Two different rates for two different crowds!

What is the dollar Libor rate in 2023?

– On the hunt for a dollar LIBOR rate in 2023? Well, it’s nearly kicked the bucket, but you might still catch a glimpse before it’s gone for good. Just remember it’s on its way out and getting replaced quicker than last season’s fashion.

What is the highest Libor rate ever recorded?

– You’ve got déjà vu—highest LIBOR rate, big question! It soared to the heavens at around 11% back in ’89. Those were the days when interest rates were on a roller coaster ride!

What is a prime rate today?

– You’re asking about the prime rate today—again? It’s a chameleon, always on the move. Best bet is to check the latest financial reports for the scoop. Don’t blink, or you might miss its next move!