In a world where the ebb and flow of home buying interest rates affect the dreams and wallets of millions, a sharp spike can feel like a thunderbolt out of the blue. And let me tell you, with the latest numbers crunched and the statistics in, that’s precisely what we’re dealing with—a shocking 6% spike in home buying rates that has prospective buyers and the housing market reeling. Here at Mortgage Rater, we’re rolling up our sleeves, delving into the nitty-gritty of this trend, and offering pearls of wisdom so you can navigate this tide with the tenacity of a seasoned sailor.

The Current Climate of Home Buying Interest Rates

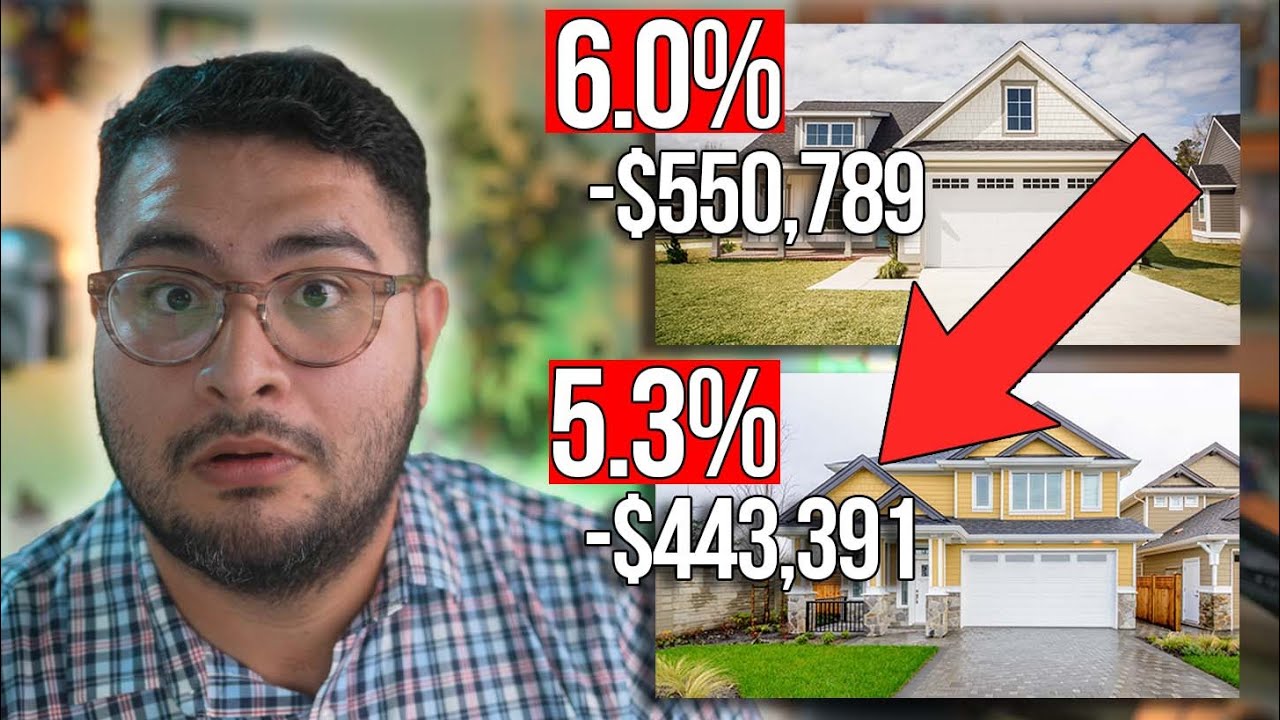

Recent data points to the most popular 30-year fixed mortgage averaging around 6.34% in January 2024, according to Zillow. If we pivot to 15-year mortgages, these hold a slightly kinder rate of 5.62%. These aren’t just numbers; they represent a significant shift in the home buying landscape, and understanding them could mean the difference between securing your dream home or being priced out of the market.

It’s like the good luck Charlie cast on a roller-coaster; we’ve been up and down over the years, hitting troughs and peaks at every turn. To put things in perspective, a cozy 3.25% rate was around the all-time low back in March 2020—a rate homebuyers would practically do cartwheels for today. The contrast to the current climb is stark, and with a 20-year high on our hands, we’re feeling the pinch.

Factors Contributing to the Jump in Home Buying Rates

Here’s where things get spicy—like a Chyna wrestler in the economic ring, inflation has body-slammed the market, and the repercussions are felt throughout the housing sector. Furthermore, the stock market’s mood swings and global events have been stirring the pot, creating a stew of uncertainty.

When the Fed steps into the ring, you know it means business. Interest rate hikes are their way of cooling down an overheated economy, but as the anvil drops, home buying interest rates feel the crush. These top-down decisions weave through the financial fabric of our nation, leaving nothing untouched.

| Category | Details |

|---|---|

| Current Average Rates (2024) | – 30-year fixed: 6.34% (as of Jan 2024, according to Zillow) – 15-year fixed: 5.62% |

| Historical Context | – A 3.25% rate is close to the historical low since 1972. – As of Mar 27, 2020, that rate was considered exceptionally good for a 30-year fixed mortgage. |

| Rate Forecast for 2024 | – Projections indicate a decrease to about 5.9%-6.1% for 30-year mortgages. |

| Impact of Economic Factors | – Increased inflation and Federal Reserve rate hikes have led to the highest interest rates in the past 20 years. |

| Strategy for Homebuyers | – Despite the high rates, the recommendation is to buy now and potentially refinance later when rates drop, in order to circumvent increased market competition expected in the forthcoming years. |

| Benefits of Lower Rates | – Lower total interest paid over the life of the loan. – Reduced monthly payments compared to higher rate loans. |

| Considerations for Refinancing | – Potential for lower interest rates in the future. – Refinancing can be advantageous when rates fall significantly below the rate of the current mortgage. – Closing costs and other fees need to be factored into the decision to understand the break-even point and overall savings. |

The Impact of 6% Increase Across Various Lenders

Not all waves hit the shore equally, and the same goes for lenders. Chase might nudge their rates sky-high, while Bank of America takes a subtler approach. Each institution charts their course through these tempestuous waters, which means doing your homework could unearth some golden opportunities.

The greenhorns looking to dip their toes in for the first time are in for a shock as the monthly payments pile up quicker than dirty laundry. Meanwhile, the old-timers with weathered maps and treasure troves of experience may find ways to sail smoother seas—or tap into resources like hunter Doohan bringing fresh perspective on navigating these challenges.

Comparing Today’s Home Buying Interest Rates to Previous Decades

Imagine a graph zigzagging like destiny 2 Servers on launch day, and you’ll get a sense of the ride we’ve had with interest rates. The stark reality of today’s climb compared to the gentler hills of the past is more than a curiosity—it’s a call to action.

Trends aren’t just for taylor swift outfit Ideas; they’re the bread and butter of economic analysis. By mapping past rates against the backdrop of economic narratives, we gain insight into the forces that drive the beast and learn how to ride it rather than being trampled underfoot.

How Different Regions Are Affected by Soaring Home Buying Interest Rates

Home buying interest rates don’t treat every backyard the same. The Northeast might be grappling with the cold embrace of higher rates more so than the Southwest, where the sun isn’t the only thing keeping things toasty.

In the big-smoke cities, the rate rise amplifies the already sky-high costs of urban living, whereas in the countryside, the shock might be dulled by the slower pace and lower baseline prices. Through case studies, we catch a glimpse of these varied regional heartbeats.

Future Forecasts: Can We Expect Further Escalation in Home Buying Interest Rates?

If only crystal balls were as easy to come by as current interest rates For Mortgages—but fret not. Even without mystical powers, economic forecasts are honed in on what to expect, helping you prepare whether the waters get choppier or calm prevails.

Market indicators are like the stars that ancient sailors navigated by—studying them can keep your ship on course. A downward tick in job growth, a spike in consumer goods—each ripple on the pond could signify a storm brewing on the horizon.

Strategies for Prospective Homebuyers to Navigate High Interest Rates

Don’t let the seas of change sweep you off your feet; it’s time to haggle and hunt like your future depends on it—because it might. Scour the horizon for fixed-rate vs. adjustable-rate mortgages that offer safe harbor from the tempest of escalating rates.

The market boffins have cooked up some clever concoctions for such a time as this. From rate locks to float-down options, there’s a roster of financial flairs designed to hitch your wagon to the stars, not to sinking stones.

The Behavioral Shift: Are Consumers Backing Off from Buying Homes?

With the uptick in home interest rates cranking up the pressure, some buyers are holding their horses, preferring to watch and wait. As belts tighten, the market rhythm shifts—diminishing the clamor in bidding wars and quelling the frenzy that previously defined the race for real estate.

Hit the sidewalks, and the story spills from the lips of hopeful homeowners, sharing tales of patience and strategy. Surveys and interviews unveil the mood on Main Street—tempered ambition in the face of financial gales.

The Bottom Line: What the 6% Rise Means for the Housing Market Overall

This isn’t just about how deep your pockets need to be; it’s about an ecosystem dance. The inventory wanes or waxes, prices rise or plateau, and the buyer’s power shifts from full-sail to half-mast as home buying interest rates chart new territory.

Conclusion: Riding the Wave of Higher Home Buying Interest Rates

The landscape’s altered, my friends, and with the winds of change comes a new map to navigate by. The insights we’ve shared today are your compass and sextant, designed to guide you through the mirage to the oasis of wise investment and a place to call home.

Uncertainty isn’t just a roadblock; it’s a potential goldmine for the bold. Seize the day, embrace the turbulence, and remember: even in a storm, there are treasures to be found—for those courageous enough to brave the waves.

In this rollercoaster of home buying interest rates, we at Mortgage Rater stand by your side, equipped with the charts and tools for a successful journey. As you face the swell of this 6% spike and traverse the changing tides, remember that knowledge is your anchor, and a strategic mind your rudder. Raise the sails, and set your course; we’re navigating these waters together.

Brace Yourselves: Home Buying Interest Rates Just Skyrocketed!

Well, butter my biscuit—have you heard the latest buzz? Home buying interest rates have done a wild jump, springing up a whole 6%! Now, before you go running for the hills, let’s dive into some engaging tidbits that’ll have you smarter than a whip on the topic.

When the Market Plays Hardball

Imagine you’re gearing up for the epic finale of your favorite online game, only to find the destiny 2 Servers down. That’s a bit how the housing market’s behaving lately. Just when you’re ready to step up to the plate and snag that dream home, BAM! Interest rates go through the roof.

Rates Higher Than a Cat on a Hot Tin Roof

But hold your horses! If you’re on the hunt for the most up-to-date news like current interest rates For Mortgages, you’re already one step ahead of the game. It’s like keeping up with the Good Luck charlie cast—you( gotta stay in the loop to know what’s what.

A Stitch in Time Saves Nine

Don’t fret if you’ve missed the memo on the hike. Quick action may cushion the blow. Locking in a rate pronto can be as rewarding as nailing that perfect Taylor Swift outfit idea for your next big outing.

Forewarned is Forearmed

If you think today’s rates are hotter than a pepper sprout, knowing the current Intrest rates—yep, the interest with a little spelling hiccup—will arm you better than a trivia champ at a bar quiz night.

The Plot Twist in the Market Saga

Ever since folks picked up on the rate rumble, it’s been like watching Hunter Doohan in a thriller—utterly unpredictable. But hey, that’s the thrill of the home buying chase!

From the Top Rope

Just like Chyna wrestler coming off the top rope with a signature move, these home interest rates have delivered a shocker that’s left us all a bit thunderstruck in the ring of home ownership.

So there you have it, folks—some fun and games mixed with the nitty-gritty. Whether it’s a spike in home buying interest rates or the latest installment in the ‘who’s who’ of celeb get-ups, keeping your ear to the ground is key. And remember, even when rates are doing the cha-cha, knowledge is power—or at least, it’s the next best thing to a crystal ball.

What is the current home interest rate?

– As of the latest buzz, if you’re hunting for a mortgage, the current average for a 30-year fixed ticked at roughly 6.34%, while the 15-year pals were looking at about 5.62%. Quite the numbers, huh? But hold your horses, these rates are as fresh as last week’s bread, straight from the Zillow ovens.

What is a good interest rate when buying a home?

– Alright, let’s cut to the chase, a good mortgage rate should feel like finding an extra fry at the bottom of the bag. With rates doing the moonwalk lately, snagging a rate around or below that sweet 6% mark is the new “good”. Remember when we swooned over 3.25% back in March 2020? Those were the days!

Are mortgage rates expected to drop?

– Are they dropping? That’s the million-dollar question! Word on the street—and by street, I mean financial gurus—is that 30-year mortgage rates could flirt with the 5.9% to 6.1% zone in 2024. But don’t play the waiting game too long; swoop in now and you might just outsmart the crowd by refinancing later.

Is 3.25 a good mortgage rate for 30 year?

– Is 3.25% your card at the rate casino? Ding ding ding — jackpot! Cast your eyes on the historic rate graph, and you’ll spot this little beauty near the all-time lows. If you snagged this gem for a 30-year fix, give yourself a pat on the back!

Who is offering the lowest mortgage rates right now?

– Scouring for the lowest mortgage rates, are we? Well, it’s a bit of a treasure hunt as offers shuffle faster than a Vegas dealer. You’ll want to comb through bank deals, credit unions, and online lenders, as they all clamor to dangle the juiciest carrot.

Will interest rates come down?

– Ah, the crystal ball question! Experts reckon we might see interest rates take a breather, but with inflation and Fed hikes strutting their stuff, don’t bank on diving back into the low tide waters just yet.

Will mortgage rates go down 2023?

– For those of you pacing in 2023, wondering if mortgage rates will take a nosedive, well, it’s a mixed bag of maybe’s. Economic wizards speculate a slight downtick, but remember, they don’t have a crystal ball, and neither do we.

Will interest rates go down in 2023?

– Peek into 2023’s interest rate crystal ball, and you’ll get a few hazy maybe’s. Some number crunchers are shooting winks at a potential dip, so keep your fingers crossed, but don’t hold your breath just yet.

Is 7% interest rate for house bad?

– On the 7% beat? It may feel like a cold splash of water to the face compared to the good ol’ days. But hey, context is king — in a market where rates are climbing the ladder, 7% might just be the new norm for a spell.

Will interest rates ever go back to 3?

– Will we be time-traveling back to the 3% wonderland? As much as we’d love to dust off our flip phones, the road back is like waiting for a bus in a thunderstorm — possible, but with chances as slim as a lottery ticket, given today’s economic shenanigans.

How low will mortgage rates go in 2024?

– Speaking of 2024, if you’re playing the long game, you might catch mortgage rates playing limbo between 5.9% to 6.1%. Of course, don’t take that to the bank just yet, ’cause, you know, predictions are as steady as a three-legged chair.

Will the mortgage rates go down in 2024?

– Will mortgage rates take a dip in the denim jacket year of 2024? The smart money’s looking at a little nudge south to the 5.9%-6.1% neighborhood. But then again, those numbers could swing like a porch door in the wind, so keep your eyes peeled and options open.

What if I lock in a rate and it goes down?

– So, you’ve locked in a rate and the numbers tumble the next day—ouch, right? But chill, it’s not a “game over” scenario. Talk with your lender; some might offer a one-time “float down” option if rates drop like hot potatoes, but it’s not a sure bet.

How to pay off a 30 year mortgage in 15 years?

– Wanna transform that 30-year ball and chain into a 15-year sprint? Start by pumping up your payments like it’s gym day — throw extra cash at the principal when you can. And don’t forget to refinance if rates take a siesta. It’s not a cakewalk, but hey, no pain, no gain.

Is 4.75 a good mortgage rate?

– The 4.75% rate might not be the belle of the ball, but given today’s rate rave, you could do a lot worse. Sure, it’s not the rock-bottom rates we’ve serenaded, but if you’re locked in already, it’s nothing to sneeze at.

Is 4.75 A good mortgage rate?

– Is 4.75% a good rate? Well, twist my arm; it’s not too shabby for the current climate! It won’t have you doing cartwheels, but you could end up with worse dance partners. It’s a bit like snagging a solid B on a pop quiz.

Is 2.75 a good mortgage rate?

– Pulling a 2.75% rate is like hitting a hole-in-one on a par 5 these days. If you’ve nabbed this unicorn rate, you’re surfing the mortgage wave like a pro — consider yourself in the VIP club of interest rates.

What is a 30 year fixed rate?

– Let’s break it down — a 30-year fixed rate is like that trusty old hatchback that gets you from point A to B over three decades. Lock in the rate, and it’ll stick with you through thick and thin, no surprises, no plot twists, just plain old consistency.

Why are mortgage rates so high?

– So, why are rates acting like a rocket? Two words: Inflation and Fed hikes are stirring the pot, and not in a good way. They’ve got rates hitting a 20-year peak, making it seem like the days of low-interest rates are just fairy tales now.