Managing a mortgage can feel like a juggling act between your dream home and your financial reality. And let’s face it, those gross monthly payment figures can serve up more surprises than a reality TV plot twist. But don’t let the numbers game catch you off balance. Understanding the ins and outs of gross monthly payment can be a game-changer in your pursuit of home sweet home.

The Untold Truth About Gross Monthly Payment and Financial Stability

Gross monthly payment is more than just a number on your bill – it’s the indicator light of your financial health. It’s the chunk of change you pay each month towards your mortgage, culled straight from your gross monthly income – that’s the cash you rake in before the tax man gets his share.

How Your Monthly Income Net Shapes Your Gross Monthly Payment Options

Your net income is the bread and butter of your mortgage game – it shapes what you can swing in terms of a gross monthly payment.

| Category | Description | Example Calculation |

|---|---|---|

| Definition of Gross Monthly Payment | The total monthly payment before any deductions. | N/A (This is a concept) |

| Relevance to Income | Based on gross monthly income before deductions. | Gross Monthly Income: $5,000 |

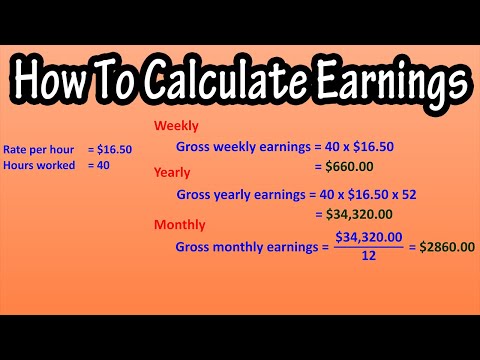

| Calculation from Salary | Divide annual salary by 12 to find monthly payment. | $60,000 annual salary ÷ 12 = $5,000 gross monthly |

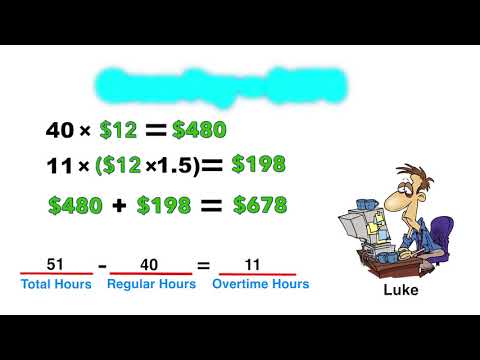

| Calculation from Hourly Wage | Multiply hourly wage by weekly hours, then multiply by 52 (weeks per year) and divide by 12. | ($22/hour × 40 hours/week) × 52 weeks/year ÷ 12 months/year = $3,813.33 gross monthly |

| Overtime Pay | Overtime pay is added to gross monthly pay. | 10 hours of overtime at $33/hour = $330 extra for the month |

| Gross vs. Net Pay | Gross pay includes all earnings before taxes and other deductions; net pay is after deductions. | Gross Monthly Income: $5,000 – Deductions: $1,000 = Net Pay: $4,000 |

| Importance for Mortgage Qualification | Lenders use gross monthly payment to calculate debt-to-income ratio. | Gross Monthly Payment: $5,000, Monthly Debt Obligations: $2,000, Debt-to-Income Ratio: $2,000 / $5,000 = 40% |

The Curious Case of Tax Implications on Your Gross Monthly Payment

It might not be as gripping as Mindhunters season 3, but the relationship between taxes and your gross monthly payment is a thriller in its own right.

Interest Rates and Their Sneaky Effect on Gross Monthly Payment

Interest rates: the stealthy ninjas of the mortgage world. They might not wear black, but boy, do they have an impact on your monthly payment.

The Pitfalls of Underestimating Insurance and Maintenance in Gross Monthly Payments

Ignoring the dull duo of insurance and maintenance is like skipping rehearsals for a Broadway show – you’re bound for a mishap when the curtains rise.

The Aftermath: When Gross Monthly Payments Morph Due to Adjustable Rates

Adjustable-rate mortgages (ARMs) – the chameleons of the mortgage zoo. One minute, they’re one color; the next, they’ve shifted entirely.

Does a Higher Gross Monthly Payment Equal Better Property Value?

Before you equate a hefty gross monthly payment with a ritzy property, remember: costlier isn’t always synonymous with value.

Conclusion: The Gross Monthly Payment Puzzle – Piecing It All Together

Navigating the gross monthly payment labyrinth calls for a balance of smarts, wit, and a smidgen of daring. It’s a riddle not unlike a tough How much Should Your mortgage be conundrum.

Take these revelations, weave them into your financial tapestry, and you’re not just an informed reader – you’re a mortgage maestro, set to conduct an opus of savvy home financing.

Unraveling the Mysteries of Gross Monthly Payment

Gross monthly payment – it’s like the drumroll before the big reveal, except this reveal is your wallet’s monthly date with your mortgage. But hold onto your hats, folks, because we’re about to dive into a treasure trove of trivia and jaw-dropping facts about that hefty slice of your paycheck!

Well, “Cut” My Bangs and Call Me Surprised!

Did you ever consider that learning How To cut curtain Bangs could actually teach you something about gross monthly payments? Stick with me here! Just like trimming those trendy tresses a smidgen too short can leave you wearing a hat for a week, just a small miscalculation in your gross payment can have you reaching for a financial cover-up. Accuracy matters, folks, whether it’s bangs or bucks!

It’s Not Just Old Faithful That’s Predictable

Taking a trip to the iconic Yellowstone Hotel( might lead to some unpredictable wildlife encounters, but there’s nothing wild about the predictability of a gross monthly payment. Once you lock it in; it’s steady-Eddie. No unexpected bear sightings here (phew)! Your payment stays the same, making budgeting as tranquil as Yellowstone’s majestic scenery.

Rule It or Lose It!

By now, you might have heard whispers about the 28/36 rule. This nifty financial guideline keeps you walkin’ on the sunny side of the street, ensuring your gross payment doesn’t munch more than 28% of your monthly income. Stick to this rule, and you’ll be just as cool as Monica Padman discussing her latest podcast episode.

Calculate Your Way to Victory

Don’t just throw a dart in the dark; use a home loan approval calculator to get a bullseye on what you can afford. It’s no crystal ball, but it sure gives you a clear peek into whether your gross monthly payment will be a gentle stream or a roaring river in your budget landscape.

A Down Payment Speaks a Thousand Words

Ever wonder How much For a down payment on a house? Buckle your seatbelts because the amount can influence your gross monthly payment BIG time. Kinda like how a few words from Monica Padman can turn an okay talk into an unforgettable conversation, a substantial down payment can turn scary payments into contented sighs.

Nashville to Knoxville: It’s a Different Tune

Play a different tune with the mortgage calculator Tennessee, y’all! Whipping out this bad boy is like taking a musical road trip from Nashville to Knoxville — every stop (or city) has different numbers to serenade you with, showing how your gross monthly payment might sway and swing to the rhythm of local real estate blues.

Isn’t it a hoot? By the time you’ve whistled through this ride, your gross monthly payment doesn’t seem so shocking anymore. It’s like the mystery novel you can’t put down, except when you do, you’re wiser about the ways of the wallet—which, let’s be honest, is a pretty sweet deal!

How do you calculate gross monthly pay?

Oh, calculating your gross monthly pay? Piece of cake! Just take the total amount you earn before taxes and deductions and voilà, that’s your number. If you’re on a salary, divide your annual salary by 12. Hourly folks, just multiply your hourly rate by the number of hours you work in a month. Simple, right?

What does gross pay per month mean?

Gross pay per month, eh? Well, that’s the whole enchilada of your earnings before Uncle Sam dips his fingers into your wallet for taxes, insurance, and the like. Think of it like the full sticker price of a car before negotiations and fees come into play.

What is my gross payment?

Your gross payment is the whole shebang you rake in before anything gets snatched away. We’re talking taxes, retirement contributions, healthcare – before all that jazz, the amount on your paycheck is what you call your gross payment.

How do you calculate gross pay?

To calculate gross pay, just grab the number before deductions from your paycheck. If you’re on the clock for hourly work, multiply your hourly wage by the number of hours you’ve clocked in during the pay period. Salary folks, divide your annual salary by the number of pay periods. Easy-peasy!

How do I calculate my gross monthly income from my pay stub?

Calculating your gross monthly income from your pay stub, you say? Look for the total amount before deductions, and that’s your answer. Sometimes, though, you need to jimmy the numbers a bit—if the pay stub isn’t monthly, just work out the period it covers and scale it up to a month. It’s like turning a mini cupcake into a full-sized treat.

What is my monthly gross income if I make 15 an hour?

If you’re grinding for $15 an hour, just multiply that by the typical 40 hours a week and again by 52 weeks a year. Divide that bulky annual figure by 12 to get your monthly gross income. Bam! If you’re clocking a standard workweek, you’d be pulling in about $2,600 each month before tax.

What is an example of a gross income?

An example of gross income, huh? Say you’re a wizard with numbers, a bona fide accountant, earning a cool $70,000 a year. That’s your gross income—the total dough you’ve earned before the taxman comes a-knocking.

Is monthly salary gross or net?

Alright, let’s sort this out: monthly salary is usually talking about your gross salary—the amount you’ve negotiated in your employment contract before deductions. Net salary would be what actually lands in your bank account after the dust settles, taxes and other deductions are done dancing around your paycheck.

How do you calculate gross pay from net?

Flipping net to gross pay can be a bit tricky, but hang tight. You’ll need the details on deductions and tax rates. Start by factoring back in each deduction to your net pay, and bingo, you’ve got your gross pay. It’s like reverse-engineering a recipe from the finished cake.

What is net monthly income?

Net monthly income is what you actually get to bank and spend on all life’s little pleasures and bills. It’s your take-home pay after taxes, Social Security, your gym membership, and that pesky student loan are deducted.

How to calculate gross monthly income from biweekly paycheck?

Gotcha on the gross monthly income from a biweekly paycheck! Here’s the deal: take your biweekly gross pay, multiply that by 26 (since there are 26 biweekly periods in a year), and then divide by 12 to get your monthly amount. Like turning biweekly groceries into a monthly food stash.

What is an example of a gross income?

Another example of gross income coming up! Picture this: You’re a freshly-minted coder making $80,000 a year before deductions. That’s your gross income, the big cheese, your earnings in all their glory, soon to get a little haircut from taxes and such.