Navigating the homebuying journey can sometimes feel like trying to understand the plot of love after lockup season 4 — confusing, with twists and turns you might not see coming. To mitigate that confusion, having a clear understanding of your mortgage costs from the get-go is crucial. That’s precisely where the Good Faith Estimate (GFE) fits into the picture. In recent years, the GFE has undergone significant transformations to ensure that borrowers can more easily understand and traverse the costs associated with their loans.

The Evolution of the Good Faith Estimate in 2024

Unpacking the Good Faith Estimate: What You Need to Know Now

The Good Faith Estimate is the financial compass for navigating the mortgage seas. It’s there to give you a clear rundown of all the expenses you can anticipate when shackling up with a loan. But like a chameleon, the GFE has changed its colors several times over the years.

From its inception, the GFE has been a beacon of hope, intended to provide transparency in an often complex mortgage process. Initially crafted as a rough outline of loan charges, it has since transformed into a more detailed and consumer-friendly format, providing more thorough disclosures.

So grab your compass. Let’s trek through the transformative landscape of GFEs and ensure you’re not caught off guard by hidden fees that could later rain on your parade.

| Aspect of Good Faith Estimate (GFE) | Detail |

|---|---|

| Definition | A preliminary document that provides an estimate of the costs and terms associated with a reverse mortgage loan to assist borrowers in comparison shopping. |

| Prior Usage (Before Jan. 1, 2023) | Document used to estimate expenses in a home loan scenario, detailing lender’s charges and loan terms based on borrower information. |

| Current Usage (From Jan. 1, 2023) | Must now also include charges expected from co-providers or co-facilities for an entire episode of care, relevant for both uninsured and self-pay patients. |

| Components | An itemized list of estimated charges, including specific services, and products associated with the borrower’s care or the loan terms. |

| Replacement Forms | The Loan Estimate (LE) and Closing Disclosure have replaced the GFE to improve transparency and understanding of loan terms and financial responsibilities. |

| Difference from Loan Approval | A GFE is an estimate and not an official loan approval. It may change after full review of borrower’s income and debts. |

| Importance for Borrowers | Allows borrowers to compare costs and features across different lenders and loan offers to find the best fit for their financial situation. |

| Impact for Uninsured/Self-Pay Patients (2023) | Enables a more comprehensive cost estimate, accounting for all related services and provider/facility charges during the coordinated care episode. |

Delving Deeper: The 2024 Updates to Good Faith Estimate Explained

In 2024, the Good Faith Estimate reforms ensured you’re not just squinting at numbers but truly understanding what you’re diving into. Rather than a blizzard of indecipherable jargon, it’s now a neatly organized list that breaks down the nitty-gritty of your expected charges, including those pesky little line items. And boy, isn’t that a breath of fresh air?

Changes in the bigger picture, especially regulatory tweaks, have lit the path for these updates. Like precision cogs in a well-oiled machine, they aim to make the entire mortgage process transparent and foolproof.

Dive into the data, and you’ll see borrowers aren’t just nodding along to terms and conditions; they’re actively engaging with the details. That’s financial enlightenment in the making!

The Impact of Revised Good Faith Estimates on Lenders and Borrowers

It’s no small feat for lenders to adjust their sails to meet the new GFE standards. But the effort seems to have paid off, with clearer skies for both lenders and their clients. Like the steadiness you feel walking into Churches in sioux city ia, there’s a newfound stability in the borrower-lender relationship.

For borrowers, the revised GFE is like getting a crystal ball into their financial future — no murky waters, just a clear view of what lies ahead. This clarity does wonders for financial planning, sparing many the gut-wrenching surprises of unforeseen costs.

Experts emphasize the seismic shift the revised GFE has initiated, taking us on a journey toward more equitable lending practices that truly consider consumer welfare.

Pros and Cons: Assessing the Outcomes of Good Faith Estimate Modifications

Just like the little red corvette, the revamp of the Good Faith Estimate is mostly fabulous, but let’s be real, no process is foolproof. On the upswing, borrowers are steering their own mortgage ships with far more confidence and capability than ever before. Yet, there are growing pains, and some lenders have found the transition bumpy, grappling with new requirements that might feel like a ninth inning curveball.

Let’s not sugarcoat it — every change has its critics. Some worry that the modifications have added layers of bureaucracy. Yet, for those focused on fair play in the mortgage field, the changes are a homerun.

Navigating the New Landscape: Good Faith Estimate in Practice

Roll up your sleeves, it’s time to get hands-on with the Good Faith Estimate. Here’s a pro tip for borrowers: scrutinize your GFE with the same intensity as a Stafe review of a buzzy new play. It pays to understand each line item, as this is the blueprint of your mortgage commitment.

Lenders, it’s over to you to ensure the changes in the GFE aren’t just fine print but are communicated with the weight they warrant. Think of it as crucial as getting your message across in any meaningful sit-down.

Peek at some real-world stories and the plot thickens — or rather, clarifies. Case studies show that when understood and used correctly, the updated GFE can align expectations and reality, sparing everyone from unwanted drama.

Beyond the Estimate: Good Faith Estimate’s Role in Broader Financial Literacy

Looking beyond the initial shock and awe of getting your new home mortgage, the GFE is playing a pivotal role in peppering financial literacy throughout the mortgage shopping experience. It’s become a didactic tool, empowering consumers to be more than passive participants. They’re now active, savvy decision-makers — akin to educated investors in the marketplace.

The translation of this document into knowledge has been akin to turning water into a fine wine. With the evolution of the GFE, borrowers no longer just glance over terms and conditions; they chew over every detail, ensuring they’re not caught in a foreclosure rout down the line.

Regional Variations: Good Faith Estimate Adjustments Across the States

From coast to coast, the Good Faith Estimate is the Constitution of mortgage disclosures, but not all states wear it the same. Some add a twist here, a tweak there — aligning national guidelines with local practices to ensure the ensemble fits just right.

Let’s compare notes. What works in sun-kissed California might not be the ticket for New Yorkers. Each state has its own recipe, cooking up regional compliance measures that flavor the GFE to local palates.

Examining the data, this move isn’t just window dressing. It’s the real deal in terms of effectiveness, ensuring that whether you are in the Big Apple or the Bay Area, your GFE talks your language.

The Tech Touch: Good Faith Estimate and the Rise of Digital Mortgage Platforms

Imagine if mortgage shopping was as intuitive as streaming your favorite series or as hassle-free as calling a ride. Thanks to technology, such a scenario is no longer a pipe dream. The integration of GFE with digital platforms is like giving your old TV a smart makeover—suddenly, everything is at your fingertips, crystal clear and accessible.

Today, algorithms ensure that the Good Faith Estimate is not merely an estimate but a precise, easy-to-digest layout of your mortgage’s financial landscape. It’s become the norm to have these figures calculated with laser precision, giving you the confidence of a bond trader moving millions with the click of a button.

Looking down the road, we can see technology continuing to revolutionize this process. Who knows, perhaps soon your GFE will project holographically from your phone!

Preparing for the Future: Good Faith Estimate and Long-Term Mortgage Strategies

The newly upholstered Good Faith Estimate isn’t just about dotting i’s and crossing t’s for today. It’s about setting the stage for your financial solvency tomorrow and years down the road. With a clearer understanding of your loan terms, you can calculate the trajectory of your long-term mortgage plans with the precision of an astronaut charting a course to Mars.

In expert circles, there’s chatter that we might see more tweaks to the GFE. After all, the only constant is change. What those changes will be, nobody has a crystal ball clear enough to predict. Yet, one thing is sure: they’ll be designed with the buyer’s best interests at heart.

Conclusion: The Updated Good Faith Estimate as a Cornerstone of Mortgage Transparency

We’ve journeyed far and wide across the rolling hills of the Good Faith Estimate evolution. What’s crystal clear is this: the updated GFE isn’t just a piece of paper; it’s a cornerstone of mortgage transparency and a trusty guide in the homebuying quest. Let’s hammer it home — without clarity in the mortgage process, aspiring homeowners would be adrift in a sea of questionable terms and conditions.

Honing in on the nitty-gritty, the GFE gives you, the borrower, the power to make informed choices, whether you’re gathering gift funds or pondering a Government-backed loan. Much like a trusted guide, it illuminates the path ahead, allowing you to march confidently toward your goal of homeownership.

So there you have it, dear reader, your map to understanding the vibrant landscape of the updated Good Faith Estimate. It’s not just another document; it’s a shield against the slings and arrows of unforeseen mortgage expenses — a beacon highlighting the path to a safe financial harbor.

Good Faith Estimate: Unpacking the Mysteries

Hold your horses, folks! Before you sprint through the meadow of mortgage paperwork, let’s huddle up and have a chinwag about something that might just tickle your fancy – the Good Faith Estimate (GFE). Yep, you heard it right; mortgage lingo doesn’t have to be as dry as a bone.

Once Upon a Time in Mortgage Land

So, what’s the lowdown on Good Faith Estimates? Way back when, getting a mortgage was akin to herding cats—utterly bewildering with surprises around every corner. But then, the GFE galloped in like a knight in shining armor. Simply put, it’s a breakdown of expected closing costs that lenders must fork over—a crystal ball glimpse, if you will, of the charges you’re likely to face when securing a loan.

Good Faith Guessing Game

Now, don’t get your knickers in a twist; while it’s named an “estimate,” lenders can’t just pluck figures from thin air. The GFE is as close as they can get without shaking a magic 8-ball—but what does that “good faith” part really mean? If you scoot on over to the definition of Good Faith Estimate, you’ll find it’s not about crossing fingers and hoping for the best. It’s about honesty and integrity. Lenders are obliged by the bigwigs in legislation land to give you a fair shake of the sauce bottle—an estimate they genuinely think covers the costs.

Accurate As a Sharpshooter

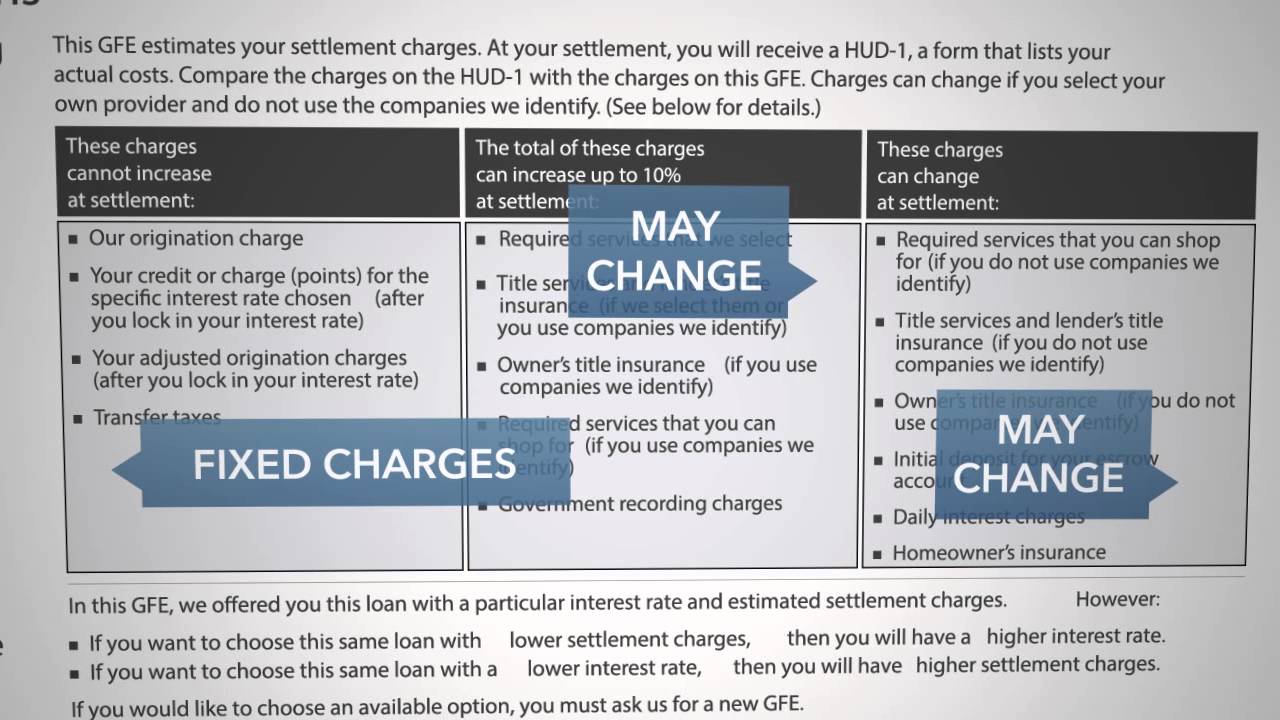

Holy smokes, right? Lenders must pull out the stops to be as accurate as a sharpshooter because if they shoot from the hip and get it wrong, they could end up in hotter water than a lobster at a clambake. With rules tighter than a new pair of boots, if the actual closing costs exceed the disclosed GFE by too much, the lender might have to eat those costs. Talk about having some skin in the game!

No More Guesswork

But wait, there’s more! The Good Faith Estimate has had a bit of a facelift and merged with another document to become the Loan Estimate. This change was about as popular as a bee at a picnic for sticklers who were used to the old ways, but it’s meant to help you, dear borrower, to compare apples to apples when shopping for loans. It’s like having a treasure map that leads you straight to the best deal—with fewer “Arrgh!” moments along the way.

Smart Cookies Use the GFE

Alright, here’s the kicker—if you’re a smart cookie about to tread the boards of the home-buying theater, getting to grips with your Good Faith Estimate is sharper than a porcupine’s backside. It’s not just about knowing what you’ll pony up in cash but also about seeing the full monty of the mortgage escapade you’re about to embark on.

So summon your inner Sherlock and dissect that GFE like it’s the case of the century. After all, understanding this paper trail could land you savings bigger than Texas. And that’s not just blowing smoke—it’s a bona fide shot at keeping your hard-earned greenbacks right where they belong: in your wallet.

What is a good faith best estimate?

Oh boy, here we go! A good faith estimate (GFE) is basically your lender’s best guess—think educated shot in the dark—of what your loan costs will probably look like. Now, don’t get it twisted; it’s not just some number they’ve plucked from thin air. It’s an itemized list of fees that lenders are required by law to hand over within three days of your loan application so you’re not hit with any surprises later on.

What is a good faith estimate called now?

Hold up! What used to be called a good faith estimate got a makeover and is now known as a Loan Estimate. Yep, that’s the fancy new name it’s been rocking since 2015 – same concept, just a bit more streamlined to make comparison shopping for mortgages easier. So, don’t go looking for the old GFE, it’s ancient history!

Does a good faith estimate mean you are approved?

Nah, getting a good faith estimate doesn’t mean you’re in the clear just yet. Think of it like being handed the menu at a restaurant – it just shows what’s on offer and what it costs; it doesn’t mean you’ve ordered anything. It’s there to give you a ballpark figure of closing costs, but approval? That’s another step down the road, my friend.

What is the good faith estimate update for 2023?

For 2023, hold onto your hats because the good faith estimate isn’t getting any big overhauls or flashy updates like your favorite smartphone app might. The rules around it are pretty set in stone—but hey, always keep an ear to the ground because you never know when the winds of change might blow through the mortgage world.

What is the good faith rule in a contract?

In the land of contracts, ‘good faith’ isn’t just a fancy term—it’s your promise that you’re playing fair and not hiding any jokers under the table. It’s the commitment to be honest and straightforward in your dealings. If you sign a contract with a good faith rule, you’re basically saying, “Hey, I’m here to do this right, no monkey business!”

Can a good faith estimate change?

Sure thing, a good faith estimate can absolutely change—it’s not set in stone. If there’s a significant change, like if you pick a different loan type or the appraisal comes in wonky, the lender might update your GFE to keep it real. Just remember, while some changes are legit, it shouldn’t be doing backflips every other day.

What is the 7 day rule in mortgage?

The 7 day rule in mortgages is pretty straightforward—it’s like a brief pause for you to catch your breath. Essentially, lenders must get you the loan estimate at least a week before closing, giving you ample time to review all the nitty-gritty details without feeling like you’re trying to sip from a fire hose.

What is an example of a good faith statement?

An example of a good faith statement? Picture it as a handshake when making a deal, saying “I got you,” like when a seller says to a buyer, “We’ll fix any termites issues before you move in, scout’s honor”—that’s a solid nod of good faith that they’ll sort it out.

What are the 4 C’s of credit?

The 4 C’s of credit are kind of like the secret sauce to loan approval—they’re crucial! They stand for Credit history (do you pay your bills on time?), Capacity (can you handle the payments?), Capital (what’s your skin in the game, like down payments?), and Collateral (what’s backing the loan?). Lenders eye these like a hawk to decide if you’re good for the money.

Why is my loan estimate so high?

Your loan estimate could be sky-high for a few reasons—and not always ones you can control! It could be due to the loan type you’re after, your credit history (yeah, every late payment counts), or even the lender’s specific costs. Sometimes, it’s just that the real estate market is as unpredictable as a teenager’s mood.

How many loan estimates should I get?

Here’s the thing, shopping around is smart—you wouldn’t buy the first car you see, right? Aim for at least three loan estimates to compare. It’s a bit like Goldilocks; you need to find the one that’s just right for you. It takes some legwork, but hey, it can save you a bundle in the long run!

How often do you send Good Faith Estimate?

The good old Good Faith Estimate only needs to make an appearance once for each loan application. The lender must provide it within three business days of your application, but after that, it’s in your court to review. No repeats unless something major changes with your loan deets.

How many years does the Good Faith Estimate have to stay on a patient’s record?

Alrighty, when it comes to keeping records, the rule of thumb for Good Faith Estimates and the paperwork party is at least six years. You gotta stick to the script set by federal law, which basically says, “Keep that paperwork on file, it’s important.”

When did Good Faith Estimate start?

Good Faith Estimates got their start with the Real Estate Settlement Procedures Act (RESPA) of 1974. Back in the day, it was all about transparency, making sure borrowers like you and me aren’t blindsided by hidden fees at the closing table.

What replaced the GFE?

The GFE met its match and was swapped out with the Loan Estimate form as part of the TILA-RESPA Integrated Disclosure (TRID) rules. The whole game changed in October 2015 when this new kid on the block took over, to clear up any confusion and better protect borrowers—you guessed it, that’s you!

When did the GFE go away?

The GFE walked into the sunset in October 2015 when it was replaced by the clearer, more user-friendly Loan Estimate. The switch-up was all about making mortgage shopping easier to digest, like swapping a heavy textbook for a neat summary.

When was the good faith estimate replaced by the loan estimate?

The new Uniform Residential Loan Application (URLA), or Form 1003, got a facelift to make it easier for all of us to spill our financial guts. The changes, which kicked in on March 1, 2021, include a more consumer-friendly layout, better clarity on loan terms, and additional data fields to make sure lenders are treating applicants fairly—think of it as the mortgage world being dragged into the 21st century!