Understanding Your Credit Score: Why It Matters and How It’s Calculated

Credit Score Basics: The Foundation of Your Financial Profile

Hey there, savvy financial navigator! If you’re here, you’re probably well aware that your credit score is like the pulse of your financial health – a vital sign that lenders check to gauge your creditworthiness. A good score opens doors to better interest rates, sweeter credit card deals, and that dream home you’ve been eyeing. But what exactly goes into that magic number?

Credit bureaus look at a mix of elements to conjure up your score, from how reliably you pay your bills to the diverse flavors of credit you’ve sampled. It’s all about how well you handle your financial obligations.

The Anatomy of a Credit Score: The Five Pillars Explained

Diving deeper into the credit score crux, we discover the quintuple forces at play that mold your financial reputation:

Key Factor #1: Payment History and Its Preeminent Role in Your Credit Score

Payment history is king. It’s a straight-up fact that late payments can stick to your credit report like a bad reputation in a small town, lasting up to seven years. Defaults and bankruptcy court appearances? They’re the big, negative billboards on your credit highway. You need to treat every payment with the same attention as if you were sculpting a masterpiece – because for the credit bureaus, you are.

Don’t let late payments cast a shadow over your borrowing future. Avoid falling into the trap where loans slip into the abyss of forgetfulness, and you’ll be golden. And remember, damage control is tougher than maintenance, much like averting a crisis is harder than tuning in to sizzling Hbo max Deals.

Key Factor #2: Mastering Credit Utilization to Optimize Your Credit Score

Now, let’s tackle that sly fox, credit utilization. Lenders love to see you using less than a third of your available credit. Why? It shows restraint, like someone avoiding the dessert section at a buffet. If you’re maxing out your cards, lenders might think you’re overindulging and that could lead to a financial hangover.

Tips for managing this? Keep a close eye on your balances, just like you’d watch Rick Hoffman Movies And TV Shows – with intent and engagement. Know when to say when, and maybe even ask for higher credit limits (without using them, mind you) to keep that utilization rate oh-so-slender.

Key Factor #3: Length of Credit History and Its Subtle Impact on Your Score

The age of your credit history whispers tales of your fiscal past. A long history provides the backdrop of a seasoned credit user who’s seen it all. If your credit history were a movie, you’d want it to be an epic saga with more sequels than you could count. Lenders eye this track record for reliability, so keep those old accounts open, as long as they’re not costing you.

But what if you’re fresh on the scene, a newbie with a shiny, new credit file? Start building that history as soon as you can. It’s like planting a tree; the best time was yesterday, the second-best time is now.

Key Factor #4: The Strategic Approach to Credit Mix and Diversification

Apart from the aging single-account credit potion, lenders are enchanted by a diverse credit mix. A blend of installment loans and revolving credit gives a panoramic view of your financial sagacity. Lenders watch your juggling act with multiple types of credit to see how you handle different balls in the air.

But, be savvy. Don’t just take on different forms of credit for the show. It’s about finding that sweet balance, like managing your Debt-to-income Ratio. Use credit as a tool, not as an uncontrollable force.

Key Factor #5: New Credit Inquiries and Their Short-Term Influence

The mystery of credit inquiries, unveiled! Each hard pull on your credit can ding your score, albeit slightly. Why does this matter? It’s about perception. Blooming inquiries can give the image of credit reliance, a red flag that you’re hungering for credit like a midnight snack.

Yet, don’t let this deter you from rate shopping. Those pulls might cluster together as one when you’re shopping for the best terms. It’s like securing the deed to a property, you want to know you’re getting the prime cut.

Beyond the Basics: Advanced Tips for Maintaining and Improving Your Credit Score

Looking to step up the credit game? Here’s an insider tip: Become an authorized user on a well-maintained account. It’s like catching a ride on a credit express train. Also, consider tools like Experian Boost to potentially get credit for paying your utility and streaming bills on schedule.

Peering into the crystal ball, credit scoring might evolve. Stay informed. With trends like alternative data creeping into credit models, you’ll want to keep your financial behavior spick and span across the board.

Credit Score Myths Debunked: Separating Fact from Fiction

Now, let’s shatter some credit myths. Does checking your score lower it? Nope, that’s as fictional as a unicorn riding a scooter. And no, carrying a small credit card balance doesn’t charm the credit score spirits. Pay it off!

Utilizing evidence, we bust myths and beef up your credit wisdom, combating misinformation with the hard truth, just like debunking clickbait headlines about celebrity diets.

Conclusion: Harnessing the Power of Knowledge for a Better Credit Score

Wrapping this up, let’s remember your credit score is a numeric story of your financial journey. Each chapter, from payment history to new credit, shapes the plot. Empower yourself with knowledge, just as you would when learning a new skill.

Embrace the marathon that is credit management. Dive into your reports even more frequently than ever before. Don’t become a character in a tragedy of credit mishaps. Instead, star in your own success saga where your credit score soars high!

It’s not just about understanding the system; it’s about actively engaging with it. Be as diligent with your credit as you are with catching every episode of your favorite show or striking while the iron’s hot on the best deals.

Carve out your path towards credit excellence, and remember, at MortgageRater.com, we’re always here to guide you through the financial maze with the wisdom of Suze Orman and the practical insights of Robert Kiyosaki. Now, go forth and conquer your credit world!

Unlock the Mysteries of Your Credit Score

When it comes to getting the lowdown on your financial wellness, your credit score is like that magic number you just can’t ignore. It opens doors to new opportunities or, well, slams them shut if it’s a bit… let’s just say, under the weather. So, buckle up as we dive into some credit score essentials that’ll have you flexing those credit muscles in no time!

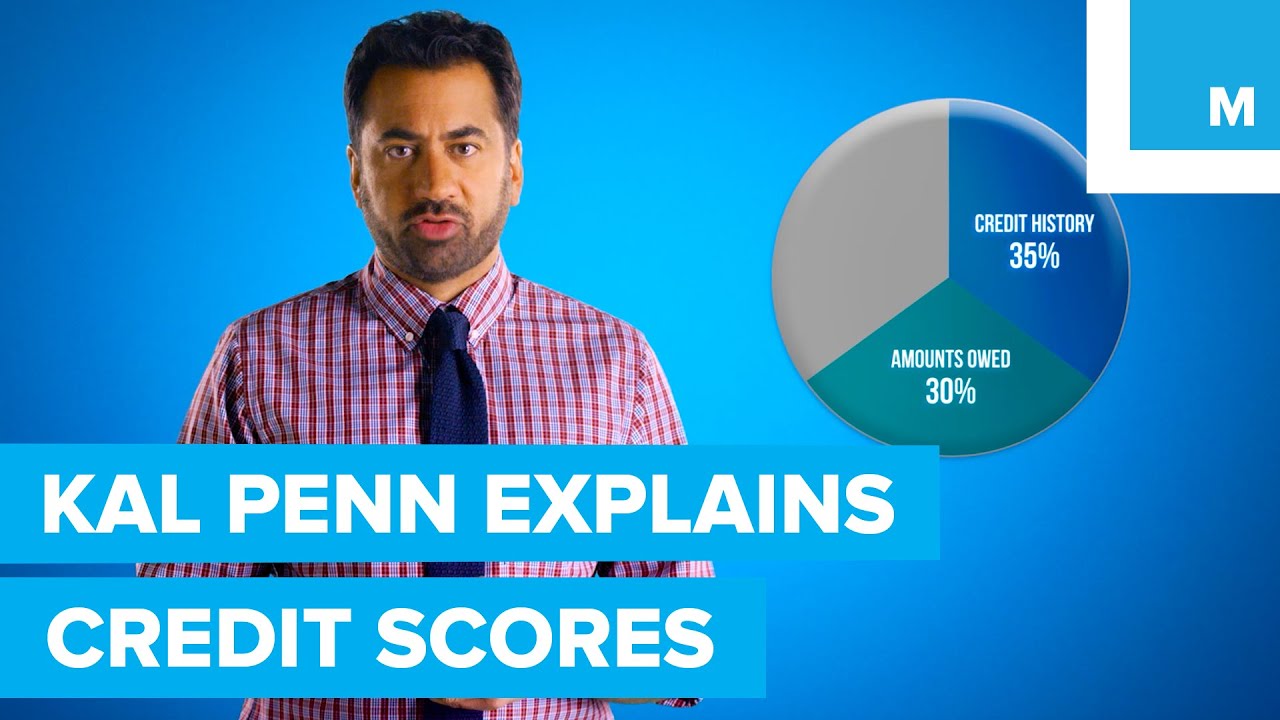

The Five-Star General: Payment History

Goes without saying, right? Your payment history is the head honcho of your credit score universe. It’s like that one friend who remembers every tiny detail about you. Missed a payment? It remembers. Paid on time? It gives you a gold star. Seriously, this bad boy accounts for a whopping 35% of your credit score. So, the golden rule? Pay your bills on time, every time!

The Sizable Slice: Credit Utilization

Here’s the skinny: credit utilization is how much credit you’re using compared to what you’ve got available. Imagine you’ve got a pizza – a big, cheesy, delightful one. Credit utilization is like how many slices you’ve devoured. Eating the whole pizza? That’s maxing out your credit, and it can leave your credit score feeling a bit queasy. Aim to only munch on 30% or less of that pizza to keep your credit score in tip-top shape!

The Long Haul: Length of Credit History

Your credit history is like a seasoned marathon runner – the longer it’s been in the race, the stronger its endurance. A lengthy credit history can show you’re a seasoned pro at managing credit. It’s not just about age, though; consistency is key here. Keep those old accounts open if they don’t cost you a dime, letting them age like a fine wine. That history makes up 15% of your score – not too shabby, eh?

New Kid on the Block: New Credit

Every time you apply for new credit, it can knock a few points off your score temporarily – kind of like stubbing your toe when walking into a room. But don’t fret! If you’re not hopping from one credit application to another like a frenzied bunny, it’s just a temporary blip on your credit radar.

The Diverse Crowd: Credit Mix

Variety’s the spice of life, and your credit score digs it too! A mix of different types of credit – think credit cards, auto loans, mortgages, and perhaps a personal loan from that time your car decided to be a drama queen – can be a good thing. It shows that you can juggle different types of credit without dropping the ball.

Speaking of Juggling, What About Those Balloons?

Ah, debt. It can feel like you’re juggling water balloons – one prick and everything explodes. If you’re feeling swamped, take a gander at debt consolidation. This savvy financial strategy might just help you handle your debts without getting soaked!

And that wraps up our little credit score safari! Remember, nurturing your credit score is a journey, not a 100-meter dash. Keep these essentials in mind and watch your score climb like it’s on a never-ending escalator – going up, of course!

What is a good credit score?

Oh boy, a good credit score, huh? Well, you’re aiming for something in the ballpark of 670 to 739 according to the FICO model, because that’s considered “Good.” Land above 740, and you’re sitting pretty in the “Very Good” range, while a score over 800? That’s the elite “Exceptional” zone, my friends!

How can I check my credit score for free?

Wondering how to check your credit score without spending a dime? Easy-peasy! You can snag a free peek at your score once a year from each of the big three credit bureaus—Experian, Equifax, and TransUnion—at AnnualCreditReport.com. Plus, many credit card companies and financial services offer a glimpse at your score as a perk, so check with them too.

Which credit score is most important?

When it’s crunch time and lenders are giving your financial history the side-eye, remember that the FICO score is the real MVP. It’s the one that most lenders have a serious crush on, so focus on beefing that up.

What is the best credit card for a 700 credit score?

Searching for the best credit card to match your 700 credit score can feel like finding a needle in a haystack, but don’t sweat it! For a score in that decent-to-strong range, look for cards that have a good mix of rewards, low APRs, and maybe even a sweet sign-up bonus.

Has anyone gotten a 850 credit score?

Has anyone hit the perfect 850 credit score? Bet your bottom dollar! While it’s rare as hen’s teeth, some financial unicorns have indeed pranced their way to this pinnacle of credit score glory. Hats off to those financial wizards!

Can you get a 900 credit score?

Can you get a 900 credit score? Nope, sorry folks. In the world of credit, FICO scores top out at 850, so chasing a 900 would be like trying to sprint past the finish line of a marathon—it just doesn’t go any further.

What is a good credit score to buy a house?

Guess what? A good credit score to buy a cozy little place to call your own is typically starting at 620 for some loan programs. But to really open doors, you want to aim for 720 or higher; it’ll likely net you better rates and a pat on the back from lenders.

What credit score is needed to buy a house?

If you’re itching to get the keys to your new digs, lenders typically want to see a credit score of at least 620. But let’s be real—you’ll have more options and better rates if your score isn’t just tiptoeing along the bare minimum.

What credit score is needed to buy a car?

Ready to vroom-vroom in a new ride? Credit scores for buying a car can vary, but usually, if you’re sitting around 660 or higher, you’re in a decent spot to secure financing. However, the better your score, the smoother the ride through the loan office.

What is a good credit score by age?

What’s a good credit score by age, you ask? It’s like a fine wine—better with time. Young ‘uns in their 20s are just starting out, so the average score might hover around the mid-600s. But as you age and get wiser with your bills, scores tend to rise, so by the time you’re rocking a comfy chair and reading glasses, your score should hopefully reflect a life of financial savvy!

What credit score do banks use?

If we’re tossing around bank talk, know this: Most banks tip their hat to the FICO score. It’s the go-to number they’re sweet on when they’re sizing up your creditworthiness.

What credit score does everyone look at?

And who’s everyone checking out at the credit score party? You guessed it—Mr. FICO. This score has serious street cred with lenders, so keep it looking sharp.

What is a normal credit limit?

Ah, the elusive “normal” credit limit. Well, it’s a bit like asking how long is a piece of string. New cardholders might see limits as low as a couple hundred bucks, while credit veterans can boast limits in the tens of thousands. All depends on your credit score, income, and the lender’s mood.

Can you buy a house with a credit score of 700?

Can you snag a mortgage with a 700 credit score? Heck yes, you can! A score like that is like a VIP pass to lenders’ hearts, likely scoring you competitive interest rates and a red carpet straight to your new home’s doorstep.

How big of a credit card can you get with a 700 credit score?

With a 700 credit score flexing in your wallet, you could land a credit card with a limit in the healthy range of a few thousand bucks, give or take. Just remember, it’s not only about the score—your income and debt play leading roles, too.

What is a good credit score by age?

Let’s talk good credit score street cred by age, again. The golden rule? It gets better with age, like cheese or a classic rock record. Keep those bills paid and don’t go nuts with credit, and you’ll probably see your score climb over the years.

How much of a loan can I get with a 670 credit score?

Curious about getting a loan with a 670 score? You’re in the “Good” credit neighborhood, so you might land a loan alright, but don’t expect the red carpet treatment. Your rates might just be a bit steeper than if you had financial six-pack abs (a.k.a. an “Excellent” score).

What’s a good credit score to buy a house?

What’s a solid score for house hunting? Plant your feet firmly in that good-to-great zone above 620, and you’ll likely find doors opening. But hey, aim for the stars over 720, and you might just get the lender’s version of a high-five in interest rate form.

What are the 5 levels of credit scores?

Credit scores are like a financial roller coaster of life—they come in five flavors: Poor, Fair, Good, Very Good, and Exceptional. You start low, climb high, and hope not to get stuck upside-down too often along the way!