Understanding the Comprehensive Loss Underwriting Exchange (CLUE)

Imagine that you’re buying insurance, and somewhere out there, there’s a little-known report shaping your premium quotes as uniquely as Chris Hemsworth’s hair molds his Hollywood identity. Enter the Comprehensive Loss Underwriting Exchange (CLUE), an intricate tool that could be the hidden hero or villain of your insurance narrative.

The Surprising Origins and Development of the CLUE Report

The inception of the CLUE report wasn’t unlike the first time you saw a flip phone; it was futuristic, a bit bewildering but revolutionized communication—in this case, between insurance providers. Initially, the idea was simple: create a shared database to track insurance histories. Insurance companies such as State Farm and Allstate witnessed a sea change, as historical data on auto and property claims over a seven-year period became a gold mine for risk assessment.

The Impact of a CLUE Report on Insurance Rates and Coverage

The tale of the tape lies here, folks. Insurance gurus pore over CLUE reports like critics over “Chris Rock and Jada Pinkett Smith” news articles, except they’re evaluating risk, not celebrity drama. If your CLUE report smells fishier than a week-old sushi roll, you bet your premiums might soar, leaving you reminiscing about the lower homeowner insurance costs that could have been. Let’s unravel this with real cases: Jane Doe filed three claims in five years, her insurance provider, getting cautious, decides her risk factor has mutated quicker than a sci-fi movie virus, and up goes her rates.

How CLUE Reports Affect Homebuyers and Mortgage Rates

Homebuying is akin to courtship; you woo lenders like Quicken Loans with your debonair financial persona. Yet, CLUE reports act like the protective best friend, whispering your past financial flings in the lender’s ear. A sullied report waves red flags—higher mortgage rates may loom, or worse, a cold-shoulder rejection might ensue. The real shockwave? How a negative CLUE report on a property can chill its real estate market appeal faster than a polar vortex.

Privacy Concerns and the Comprehensive Loss Underwriting Exchange

You’re thinking, “Hold up, is Big Brother insurance style here?” Well, ladies and gents, strap in because this ride dives deep into the murky waters of data privacy. The Fair Credit Reporting Act is your legal lifeguard here, and yes, CLUE must play by the rules. But does knowledge of your claims feel like a peek into your financial closet? Where’s the balance? On one hand, we crave privacy tighter than our favorite jeans; on the other, we need that just-right insurance rate grounded in hard data.

CLUE Reports: Myths vs. Reality

“CLUE reports reveal everything!” Hold your horses—it’s not the all-seeing eye. It doesn’t track parking tickets any more than Flixtor streams your favorite live sports. Rather, it’s a factual summary focused on claims history for property and auto—nothing about your Netflix binges or that time you sang off-key at karaoke.

How to Obtain and Interpret Your Own CLUE Report

Ever wished to be a detective in your own privacy mystery? Well, voilà! Ring up LexisNexis at 1-866-312-8076 like an insurance Sherlock Holmes and request your CLUE report. Or, take the digital express through their online form like you apply For a business loan—efficiently. Once you have the dossier, play that jazz music, and study each claim like a fine wine connoisseur.

Navigating Disputes and Corrections in Your CLUE Report

Mistakes in CLUE reports are like finding raisins in your chocolate chip cookies—unwelcome surprises. But you, my friend, are not helpless. Challenge inaccuracies like you’re debating the superiority of Pods moving cost versus traditional movers. Contact LexisNexis, be the squeaky wheel, and make sure your financial narrative is spotless and true.

Future Directions of CLUE and the Insurance Industry

AI whispers around the corner, and blockchain struts in like it owns the place. These two might be the game-changers in how CLUE evolves, reshaping its heart and soul. Alongside, there’s chatter about new regulations like the ingredients list on a cereal box—revealing everything. Could we see a shift as decisive as Danilo Cavalcantes character arcs? Only time will tell.

Conclusion: The Secret World of Insurance Data Mining

What a journey through the underbelly of insurance data! The Comprehensive Loss Underwriting Exchange is a potion mixed with insurance needs and privacy potions. CLUE reports can be your fairy godmother, nudging you towards savvy decisions, like understanding What Is expense ratio for maximum benefit in wealth management, or they can be the stooge that trips you up, possibly leading to increased homeowner insurance cost and tougher mortgage approvals.

Like a well-oiled screenplay, every twist and turn in your claims history scripts its adventure. Stay informed, stay proactive, because, in the end, managing your CLUE report effectively is not just about numbers and data, it’s about securing that peace of mind, something that cannot be valued, much like the perfect ending to a movie epic or the timeless magic of Chris Hemsworth’s hair.

Unveiling the Mysteries of the Comprehensive Loss Underwriting Exchange

You know how you might keep tabs on Chris Rock and Jada Pinkett Smith’s latest shenanigans? Well, believe it or not, there’s something similar for the insurance world, and it’s known as the comprehensive loss underwriting exchange. This mystical-sounding entity might not be making headlines like Hollywood celebs, but it sure holds some juicy details—about your insurance claims, that is!

Are You in the Driver’s Seat of Your Insurance History?

Hold onto your steering wheel! Every time you file a car insurance claim, it’s like leaving a breadcrumb that leads right back to your driving history. The comprehensive loss underwriting exchange is like a hawk, keeping a keen eye out, collecting data faster than you can say “fender-bender.” We’re talking records of claims you’ve made, inquiries you’ve shot their way, and sometimes, this info sticks around for as long as seven years. Yikes!

Your Home is Their Castle Too

Think your humble abode is off the comprehensive loss underwriting exchange’s radar? Think again! Much like Chris Hemsworth’s hair gets attention for its perfect waves, this exchange notices every single time you claim damage or loss on your property. Suddenly, that tree through the window during the storm last year isn’t just a memory—it’s a permanent record that could impact your future insurance premiums.

Insurance Matchmaking: It’s a Thing!

Here’s a fun tidbit: when you’re shopping around for new insurance, providers might swoop right into the comprehensive loss underwriting exchange, digging up your past quicker than you can dig into a tub of ice cream on a bad day. Think of it as an insurance matchmaking service—they’re peeking at your profile to see if you and the insurer could have a fairy tale ending, or if it’s more likely to end in a financial horror story.

Say Cheese! Your Snapshot is Worth a Thousand Words

Alright, brace yourself for some camera action because your comprehensive loss underwriting exchange record is like a snapshot of your insurance soul. It’s a treasure trove of detail, capturing every twist and turn of your claim history. And get this—it could even include information that’s not as straightforward as a simple ‘claim filed’ note. Your insurance script might have more plot twists than an award-winning thriller!

You Can Be the Star of Your Own Insurance Saga

Now, don’t get all gloomy thinking the comprehensive loss underwriting exchange is the end-all and be-all. You’ve got the power to request a copy of your report once a year for the oh-so-appealing price of—wait for it—free! Yep, you’ve got the right to scour your own data and ensure that it’s accurate. Any mistakes? You can challenge them like a hero standing up to the villain in the climax of an epic film.

There you have it, folks – the comprehensive loss underwriting exchange uncovered in all its mysterious glory. It might not have the glam of Hollywood or the magic of Asgard, but when it comes to the insurance world, it’s definitely playing a leading role. Keep a close tab on it, and you might just find yourself taking home the award for Most Informed Policyholder of the Year!

What is the comprehensive loss underwriting exchange?

Whew, the Comprehensive Loss Underwriting Exchange, or CLUE for short, is like a secret diary for insurers, spilling the beans on your past home or auto insurance claims. It’s a detailed report that insurers peek at to check out your claim history before deciding to play ball with you or not.

Can I view my clue report online?

Oh, you betcha! Peering into your CLUE report online is as simple as pie. Just hop onto the LexisNexis website, and with a few clicks, you can request your very own report. Handy, right?

What shows up on a clue report?

So, what’s the scoop on a CLUE report? Think of it as the highlight reel of your insurance claims history. It’s got the juicy details on any claims you’ve filed, including the type of loss, the amount dished out, and even when it all went down. It’s pretty much your insurance track record!

How do I clear my clue report?

Clearing your CLUE report is kinda like trying to erase a bad grade from your report card – not the simplest task. If you spot an oopsie, you’ll need to contact the reporting insurer and play detective to prove it’s incorrect. No magic eraser, but definitely worth a shot if there’s a blunder!

Why would an insurer use the claims and underwriting exchange?

Insurers use the Claims and Underwriting Exchange, CLUE for short, as their go-to background checker. It’s like they’re flipping through your insurance yearbook to see if you’ve been naughty or nice with past claims. It’s a crucial tool in their belt to gauge the risk of taking you under their wing.

What is a comprehensive loss mean?

When your car decides to give you a headache with damage from anything other than a fender bender with another vehicle, that’s what you call a comprehensive loss. It’s the stuff of “it could happen to anyone” – theft, hail damage, or an unexpected rendezvous with a deer on the road.

Can I pull my own LexisNexis?

Pulling your own LexisNexis report is definitely on the table. Just like ordering takeout, you can request your personal report, and LexisNexis will serve up the details of your insurance claims faster than your favorite pizza delivery.

How far back does a clue report go?

The CLUE report’s got a memory like an elephant, stretching back seven whole years of your claims history. Time flies, but insurers like to keep these old stories on hand to decide if you’re a keeper.

How much does clue report cost?

Guess what? Grabbing a copy of your CLUE report won’t cost you a dime! It’s like nabbing a free coffee on your birthday – totally on the house, once a year, thanks to the Fair Credit Reporting Act.

Can I pull a clue report?

Can you pull a CLUE report? Absolutely! It’s your report, after all. You’re entitled to a free peek once a year, so you can make sure everything’s on the up and up with your insurance history.

Can a clue report be wrong?

A CLUE report wrong? Say it ain’t so! But alas, mix-ups happen. If the info looks wonky, it’s your cue to raise a flag. Get on the horn with the reporting company and LexisNexis to get things squared away.

How do I check my insurance claim?

To check your insurance claim, just ring up your insurance provider or log into your account online. It’s like tracking a package – you want to know where it’s at and when it’ll hit your doorstep, or in this case, your bank account.

Why did my clue data disappear?

If your CLUE data pulled a Houdini and vanished, it might be because you haven’t made any claims in the past seven years. After that, your history takes a bow and exits stage left from the report.

Does clue track your data?

Does CLUE track your data? You bet they do; they’re like the paparazzi of insurance claims! They keep tabs on your claims for seven years, so insurers have the scoop on what kind of policyholder you’ve been.

What if LexisNexis has wrong information?

Wrong info in your LexisNexis report? Ugh, talk about a bad hair day for your data. But don’t sweat it – you can dispute the errors and get them to set the record straight. A bit of a hassle, but hey, it’s worth it to clear your name.

What is the ICA in insurance?

Ah, the ICA in insurance – that’s Insider’s Club, right? Just kidding! It stands for the Insurance Contribution Act, which is all about determining how much cash each insurer has to fork over to a shared pot that covers folks who’re harder to insure.

What is the difference between comprehensive loss and collision loss?

Comprehensive vs. collision loss – let’s break it down. Comprehensive is like the catch-all bucket for the weird stuff (theft, weather, vandalism), and collision? Well, that’s when your car tangles with another car or object. Think of them as two sides of the auto insurance coin.

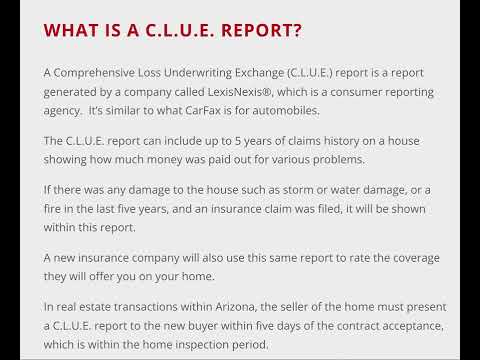

How many years of claims history does the clue comprehensive loss underwriting exchange contain?

The CLUE report is like a carrier pigeon that delivers news of your seven-year insurance claim history. Whether it’s a tiny scratch or a big boo-boo, if you made a claim, it’s remembered for a solid seven spins around the sun.

What causes an underwriting loss?

An underwriting loss happens when insurers are in the red, paying out more in claims and expenses than they’re raking in from premiums. It’s like throwing a party that costs more than the cover charge – not the goal, but it happens!