Navigating the mortgage process in 2023 can feel like finding your way through a maze. But with the right tools and understanding, you can calculate your mortgage loan accurately and make informed financial decisions. In this article, we’ll dive deep into the nuts and bolts of mortgage loans, showcase the top tools to calculate them, and uncover strategies to optimize your calculations. Let’s get started!

Understanding “Calculate Mortgage Loan” Basics

Before you start punching numbers into mortgage calculators, it’s vital to grasp the essential components that make up your mortgage. These factors include the principal, interest rates, loan terms, and amortization schedules. Here’s a quick breakdown:

Understanding these key elements will serve as a solid foundation as you calculate mortgage loans.

Top 7 Tools to Calculate Mortgage Loans in 2023

Here are some of the best tools to help you calculate mortgage loans effectively in 2023:

| Loan Amount | Interest Rate | Loan Term (Years) | Estimated Monthly Payment | Notes/Considerations |

| $400,000 | 7.00% | 15 | $3,595 | Does not include insurance or property taxes |

| $400,000 | 7.00% | 30 | $2,661 | Does not include insurance or property taxes |

| $500,000 | 7.10% | 30 | $3,360.16 | Range $2,600 – $4,900 depending on term and rate |

| $600,000 | 7.00% | 30 | $3,992 | |

| $600,000 | 7.00% | 15 | $5,393 |

Key Variables in Calculating Mortgage Loans

Calculating a mortgage loan isn’t just about feeding numbers into a calculator. You need to understand how different factors influence your finances:

Interest Rates

Interest rates remained historically low in 2023 but are subject to variations based on Federal Reserve policies and economic conditions. To put this into perspective:

– Example: A 0.5% increase in interest rates can cost an additional $30,000 over the life of a $400,000 loan at 30 years.

Loan Term

Choosing between a 15-year and a 30-year loan can significantly affect your finances. Consider this:

– Example: Opting for a 15-year fixed mortgage could save over $100,000 compared to a 30-year fixed at a similar interest rate.

Principal Amount and Down Payment

The principal amount and your down payment play significant roles:

– Example: A 20% down payment can eliminate PMI, saving you hundreds each month.

Strategies to Optimize Your Mortgage Calculations

Having the right tools and knowledge is great, but strategy matters too. Here are some tactics to optimize your mortgage calculations:

Refinancing Recommendations

Evaluate your current mortgage against prevailing rates. Refinancing could save you money.

– Example: Homeowners who refinanced in 2023 when average rates dipped, reported monthly savings of $200 or more.

Debt-to-Income Ratio

Minimizing discretionary debt can enhance your qualification chances and fetch better interest rates.

– Example: Reducing credit card debt by $10,000 increased one applicant’s credit score by 50 points, leading to a lower interest rate.

Pre-approval Strategies

Getting a pre-approval with a locked-in rate gives you an edge in volatile markets.

– Example: Pre-approvals in 2023 sped up home-buying processes, minimizing competition delays.

Utilizing Federal Programs

Federal programs like FHA, VA, and USDA loans offer advantageous terms for qualified applicants.

– Example: First-time buyers often use FHA loans to benefit from lower down payments and flexible requirements.

Carving the Future Path of Mortgage Calculations

Mastering mortgage loan calculation is crucial for making sound financial decisions. Utilize the best tools, comprehend the influencing factors, and apply strategic insights to optimize your home-buying process in 2023. As the mortgage landscape continually evolves, keeping informed will ensure enhanced financial stability and peace of mind.

Explore more resources such as the full disclosure meaning to ensure you’re fully informed about your mortgage terms. And remember, accurately calculating your mortgage loan might just be the key to unlocking the home of your dreams.

For a deeper dive into mortgage calculations and more tools to help you estimate home loan payments and calculate mortgage payment amounts, visit Mortgage Rater. Your journey to financial security and home ownership starts here.

Fun Trivia and Interesting Facts About Calculate Mortgage Loan

Curious about how to calculate mortgage loan and spice up your knowledge with some quirky facts? You’ve come to the right place! Let’s dive into some engaging trivia that’ll leave you both informed and entertained.

Mortgage Calculations Are Everywhere!

When you hear about mortgaging, you might think it’s all dry numbers. But, did you know mortgages and milk share a quirky link? Imagine you’re pondering your calculator mortgage payment while enjoying a glass of long life milk. Sounds odd, right? Yet, both offer longevity and security in their own ways. A mortgage gives you a long-term housing plan, much like long life milk ensures you have milk available without frequent trips to the store.

Estimation Fun

Ever wondered how long it’d take to buy a house entirely in coins? Well, not quite possible, but estimating your monthly mortgage payment is essential. Think of it like estimating how many cows it’d take to produce the world’s supply of long life milk! Speaking of estimates, the next time you project your mortgage cost, remember, whether it’s the Noi formula or pennies for milk, estimating is everything.

Unexpected Connections

So, you’re deep into the financial weeds and encounter a fun fact—mixed in with your mortgage planning is a nugget about Whether Ainsley earhardt Is engaged To Sean hannity! While their relationship status doesn’t affect your mortgage, it adds a splash of gossip to lighten the financial talk. And hey, if thinking about intriguing celebrity headlines keeps you more relaxed while you estimate and calculate, then why not?

Calculate mortgage loan processes can be daunting, but sprinkling in some trivia makes the journey more enjoyable. So next time you’re crunching numbers, pair it with a fun fact to make the task a little brighter.

What is the formula for mortgage calculation?

To calculate a mortgage, you’ll use the formula M = P[r(1+r)^n]/[(1+r)^n-1], where M is your monthly payment, P is the loan amount, r is the monthly interest rate, and n is the total number of payments. It might sound like gobbledygook, but plugging your numbers into an online mortgage calculator can simplify it.

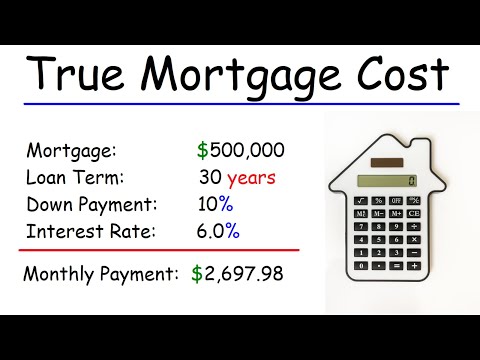

How much is a mortgage on a $500,000 house?

For a $500,000 mortgage, you’re looking at an estimated monthly payment of $3,360.16 if you have a 30-year loan term and a 7.1% interest rate. However, payments could vary between $2,600 and $4,900 depending on different interest rates and terms.

What is the monthly payment on a $600000 mortgage?

At a 7.00% fixed interest rate, the monthly payment for a $600,000 mortgage on a 30-year term is likely to be $3,992. If you go for a 15-year term, expect that to jump to around $5,393 a month.

How much is a mortgage on a $400,000 house?

On a $400,000 mortgage with a 7% fixed interest rate, the monthly payment is about $2,661 for a 30-year loan. If you choose a 15-year loan, the monthly payment goes up to around $3,595. Remember, those numbers don’t include insurance or property taxes.

How is a mortgage amount calculated?

To calculate a mortgage amount, lenders generally look at your financial health, including income, debts, and credit score. They also use a specific formula involving the loan amount, interest rate, and loan term to determine your monthly payment.

What formula do you use for mortgages?

When calculating mortgages, the formula used is M = P[r(1+r)^n]/[(1+r)^n-1], where M is the monthly mortgage payment, P is the principal loan amount, r is the monthly interest rate, and n is the number of payments over the loan’s term.

How much income do you need for a 350K house?

For a $350K house, you typically need an annual income somewhere between $70,000 and $87,500. This depends largely on your other debts, the loan terms, and current interest rates, so your mileage may vary.

What credit score is needed to buy a $500,000 house?

Buying a $500,000 house usually means you’ll need a credit score of at least 620, though a higher score can help you secure a better rate. Lenders look at your credit score to gauge how risky it might be to loan you money.

How much income is needed for a $500,000 mortgage?

To comfortably afford a $500,000 mortgage, you generally need an annual income of around $125,000 to $150,000. This assumes your monthly debt payments are in check and you have money for a down payment.

How much house can I afford if I make $36,000 a year?

If you make $36,000 a year, you can probably afford a house priced around $150,000, assuming minimal debt and a decent down payment. It’s always best to get pre-approved to know for sure.

How do people afford a $600000 house?

Affording a $600,000 house usually requires a household income of at least $150,000 to $180,000. This also factors in having a manageable debt load and a decent credit score to secure a favorable loan rate.

Is the 28/36 rule realistic?

The 28/36 rule, which says no more than 28% of your income should go to housing costs and 36% to total debts, is often considered realistic. It’s a good benchmark to ensure you’re not overextending yourself financially.

What should my income be for a 400k house?

To buy a $400K house, you generally need an annual income between $80,000 and $100,000. This range takes into account principal, interest, taxes, and insurance, assuming you don’t have a hefty amount of other debts.

How much house can I afford if I make $70,000 a year?

With a $70,000 annual income, you can usually afford a house priced around $280,000 to $300,000. Your exact affordability will depend on your debts, down payment, and the interest rate you can secure.

Can I afford a 400k house on 100k salary?

Making $100,000 a year, you can generally afford a $400K house comfortably. Lenders will still check your debt-to-income ratio and other factors, but you should be in good shape.