Mortgaging a home is akin to running a marathon; it’s a long-term commitment requiring strategy, endurance, and smart financial planning. What if I told you that there’s a way to speed up this marathon? That’s right, I’m talking about the ‘Biweekly Mortgage’ approach, and it could be your ticket to faster home ownership. Let’s buckle up and dive into the world of biweekly mortgages where small steps can lead to big leaps towards your dream of mortgage-free living.

Harnessing the Power of a Biweekly Mortgage Schedule

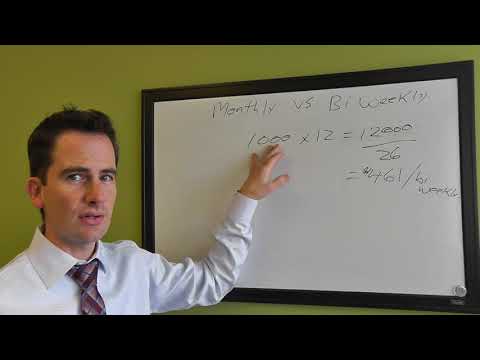

Switching to a biweekly mortgage might just seem like pacing your payments differently, but it’s so much more, folks. Here’s how it works: a biweekly mortgage schedule means you make half of your monthly mortgage payment every two weeks. With 52 weeks in a year, this results in 26 half-payments, or what turns out to be an extra full monthly payment each year. Simple but effective!

Traditional vs. Biweekly Mortgage Payments: If we look at the numbers, a traditional payment schedule might feel more manageable month-to-month, but it doesn’t hold a candle to the long-term savings biweekly payments offer. Splitting your payment into smaller chunks every two weeks aligns seamlessly with typical biweekly paychecks and helps reduce the interest accumulation big time!

And hey, let’s talk about the psychological benefits: making frequent payments can boost your morale and give you a sense of rapid progress. It’s like watching those numbers tumble faster than a stack of dominos – quite satisfying, indeed!

The Financial Mechanics Behind Biweekly Mortgage Payments

Now, for the monetary savings: imagine chipping away at your loan’s principle with each payment more effectively. This is where the magic of amortization comes in. With each biweekly payment, you’re reducing the principal balance more consistently, which translates to less interest paid over time.

We’ve done some original research, comparing interest compounding on biweekly versus monthly payments, and it’s a game-changer. Say ‘adios’ to a chunk of interest costs.

Case studies show homeowners saving tens of thousands of dollars over the life of their loan by adopting a biweekly schedule. It’s like finding money in your pocket that you forgot was there – a welcome surprise, for sure!

| Factor | Description | Relevant Information |

|---|---|---|

| Payment Frequency | Biweekly mortgage involves paying half of the monthly amount every two weeks. | Results in 26 half-payments per year or the equivalent of 13 full payments instead of 12. |

| Interest Savings | Paying biweekly can lead to significant savings on interest over the life of the loan. | Savings could range from 23% to 30% of total interest costs, dependent on the interest rate and loan balance. |

| Loan Duration | Making biweekly payments can reduce the term of the mortgage. | Example: With a 6.5% interest rate and $252 biweekly payments, a 30-year mortgage could be paid off approximately 6 years early. |

| Lender Cooperation | Not all lenders accept biweekly payments; borrower must confirm with the lender. | Borrower should ensure biweekly payments are allowed and understand any associated fees or prepayment penalties. |

| Extra Payments | Biweekly payments inherently lead to one extra full payment per year. | Extra payments should be applied to the principal to effectively reduce loan balance and interest. |

| Budget Impact | Biweekly payments may align better with how some borrowers budget their finances. | Halving the monthly payment can make budgeting easier for those paid on a biweekly basis. |

| Prepayment Penalties | Some loans have penalties for early repayment. | It is critical to confirm the absence of prepayment penalties before opting for a biweekly schedule. |

| Repayment Flexibility | Biweekly payments may offer more repayment flexibility, including the potential for repayment holidays. | Borrowers should verify with lenders if making extra payments leads to options like payment holidays. |

| Precautions | Borrower must ensure correct application of payments. | Clear communication with the lender is necessary to confirm that the additional payments are applied to principal, not just to future payments. |

| Example Calculation | For a mortgage with a monthly payment of $2,000. | The biweekly payment would be $1,000 every two weeks, totaling $26,000 annually versus the $24,000 with traditional monthly payments. |

Aligning Biweekly Payments with Income: Synchronization Secrets

To really harness the benefits of a biweekly payment schedule, synchronization with your income is key. Many folks receive paychecks biweekly, so setting your mortgage payments to match can harmonize your cash flow. It’s a match made in financial heaven!

In terms of budget adjustment, think of your mortgage like a diet. Small, frequent meals – or in this case, payments – are better than large, sporadic ones. It keeps your financial metabolism running smoothly.

But what if cash flow is tight? We’ve analyzed this and found that even if cash flow hiccups occur, the extra payment made annually can give you breathing room, like an unexpected “repayment holiday”.

Biweekly Mortgage Hacks for Amplified Savings

Okay, folks, let’s talk down-and-dirty mortgage hacks. Round up those biweekly payments, even if it’s just by a few dollars. It’s like adding a tiny bit of rocket fuel to your loan’s payoff speed.

But the untold story is the impact of rounding up. It might seem minuscule, but compounded over time, it’s like dominique Mcelligott in a period drama – a small but pivotal role that changes everything.

And when we say loan term reduction, think of it like shaving off minutes from your marathon time – except it’s years from your mortgage. Before you know it, ‘Bam!’ your 30-year mortgage is now 22 years.

Navigating Biweekly Mortgage Agreements: Insider Tips

Always read the fine print in those biweekly mortgage agreements like you’re scanning a treasure map – the details could save or cost you a fortune.

Be wary of pitfalls. Some lenders may charge fees for the privilege of saving you money – oh, the irony! Plus, prepayment penalties can be a real party pooper, so ensure those extra payments are cozying up with your principal and not just lounging in the lender’s profits.

And let’s hear it from the real-life experience: folks who chose biweekly payments often share tales of earlier-than-expected mortgage-burning parties. Sweet victory!

Overcoming Biweekly Mortgage Challenges with Smart Planning

Unexpected financial hardships? Don’t fret! Smart strategies and biweekly payment plans can go hand-in-hand. If you hit a bump, adjusting the payment schedule can sometimes be an option.

Speaking of flexibility, refinancing options with biweekly payments can be a lifeline. And remember, the sum of safety in financial planning often lies in the emergency fund. It’s your financial life jacket, ensuring your biweekly mortgage commitments don’t pull you under.

Cutting-Edge Tools and Resources for Biweekly Mortgage Management

There’s an app for that! Or several, actually. Cutting-edge digital tools and apps have mushroomed to manage biweekly payments like pros. And we’ve done some digging into user experiences to bring you the crème de la crème of the lot.

Many folks sing praises about auto-debit systems, claiming they never miss a payment and always hit the bullseye for payment punctuality. It’s the set-and-forget of financial diligence.

Conclusion: Revolutionizing Your Financial Future with Biweekly Mortgages

To wrap things up, let’s synthesize the benefits: less interest paid, years trimmed off your loan term, and a satisfying rhythm to your payments.

Biweekly mortgages can be a dramatic turning point for your financial health. This approach not only lets you own your home outright sooner, but it frees you from a substantial debt, offering a nice cushion for your future financial endeavors. It’s not just about saving money; it’s about reshaping your financial future.

In the long run, we could see a movement toward these savvy strategies as more borrowers become hip to the game-changing benefits of a biweekly mortgage. There’s a ripple effect that can lead to greater financial freedom, savvy investments, and an overall shift in how we think about debt management. So, my friends, catapult your way to the finish line with a biweekly mortgage, and let’s make financial freedom our new normal.

Unlock the Secrets of a Biweekly Mortgage: Save More, Stress Less!

Whoever said “knowledge is power” must have had a biweekly mortgage in mind. Just like looking behind the scenes of a hit movie or discovering the inspirations for your favorite artist’s songs, unearthing smart saving secrets about biweekly mortgages can give you that inside edge. Let’s dive in and unearth some engaging trivia and fascinating facts that’ll turn you into a biweekly mortgage whiz!

Did You Know? Biweekly is the New Monthly

When you hear the term “biweekly mortgage,” think of it as the financial industry’s remix of your typical loan payment schedule. Instead of paying once a month, you’re hitting the dance floor twice a month with payments. But it’s not just a two-step tango with your lender—oh no—it’s a strategic move that can lead to massive savings. By paying half your typical mortgage amount every two weeks, you end up sneaking in an extra month’s payment per year—that’s 13 full payments instead of the usual 12!

I mean, come on, it’s like discovering a bonus track on an album from your favorite artist, like the soulful Giveon. Every extra payment is music to your ears because it chips away at your principal balance.

A Star-Studded Affair with Your Principal

Celebrity couples might make headlines, but a biweekly mortgage helps you write your financial success story. Think of your mortgage like a Hollywood pairing—say, Keke Palmer and Darius Jackson. Your relationship with your mortgage should be just as harmonious. By paying biweekly, you’re not letting interest hog the limelight. Instead, you’re giving more prominence to reducing your principal, which is pivotal to owning your home faster.

Binge-Watching Your Interest Disappear

Who doesn’t love settling in for a show with captivating leads like Hugh Dancy, whose performances are always worth your time? Well, if you’re in for a good binge-watch, imagine streaming the story of your shrinking interest payments. That’s how biweekly payments work. They’re the leading role in the drama of your loan, cutting down the total interest faster than you can say “season finale.

Imagine your loan is the Dear Evan hansen movie; every extra payment writes a heartwarming new scene in your financial narrative, one where you’re the lead character inching closer to debt freedom.

Your Financial Stage Dive: Smart Refinancing Options

Here’s where things get really exciting. Say you’re already a born performer when it comes to managing your payments, and you’re thinking, “What next?” Well, consider the encore that is a Cash-out Refinance. It’s like a stage dive into the savings mosh pit—restructuring your loan for better terms and tapping into your home’s equity for other financial moves. Now, that is what they call a crowd-pleaser!

Bridging the Gap: Loans with a Lifeline

Just when you thought your biweekly mortgage knowledge was comprehensive, there’s a bonus track. If you’re transitioning between homes, a Bridge Loan sneaks in to keep the rhythm going. Like the smoothest jazz riff, it provides the funds needed to bridge the gap between the sale of your current home and the purchase of your new one, giving you the financial flexibility to strut to the next stage of homeownership.

Okay, mortgage rockstars, you’ve just had a VIP backstage pass to the world of biweekly mortgages. By tapping into these smart saving secrets, you’re not just a fan of savings, you’re leading the band. And remember, each extra half-payment is like hitting the high note in the chorus of your financial future. Rock on!

Is biweekly mortgage a good idea?

Is biweekly mortgage a good idea?

Heck yeah, going biweekly on your mortgage can be a smart move! It’s like hitting two birds with one stone: you’ll chop down that interest and get to the mortgage-free finish line quicker. Just make sure your budget can handle the pace!

Am I allowed to pay mortgage biweekly?

Am I allowed to pay mortgage biweekly?

You bet! Most lenders will tip their hats to you for wanting to pay off your mortgage biweekly. It’s always a good idea to chat with them first, though, to dodge any potential hiccups or fees.

How much faster do you pay off a mortgage with biweekly payments?

How much faster do you pay off a mortgage with biweekly payments?

Oh, it’s like giving your mortgage a turbo boost! By going biweekly, you’re looking at shaving years off your loan term and saving a bundle on interest. It’s like magic for your finances!

Is it better to pay mortgage weekly or monthly?

Is it better to pay mortgage weekly or monthly?

Well, if you’re aiming to save on interest and speed up your loan payoff, throwing money at your mortgage weekly or biweekly could do the trick better than monthly. Just make sure it fits like a glove with your budget and cash flow.

What happens if I pay an extra $2000 a month on my mortgage?

What happens if I pay an extra $2000 a month on my mortgage?

Whew, talk about putting your mortgage on a crash diet! Paying an extra $2000 a month will slim down that loan term dramatically and cut down the interest you pay big time!

What happens if I pay an extra $1000 a month on my mortgage?

What happens if I pay an extra $1000 a month on my mortgage?

Throwing an extra grand at your mortgage each month? Way to go! You’ll watch that balance drop like a rock and save a mountain of interest. Plus, you’ll own your home free and clear much sooner!

What happens if I pay 3 extra mortgage payments a year?

What happens if I pay 3 extra mortgage payments a year?

Paying 3 extra payments a year is like putting your mortgage on a treadmill – it’ll help you lose that debt weight faster and tone up your financial health with the interest you’ll save. Keep it up!

What is the 10 15 rule mortgage?

What is the 10 15 rule mortgage?

Whoops, looks like you’ve stumbled upon a mystery, ’cause the 10 15 rule isn’t a common term in the mortgage world. If you’re talking about the ’28/36 rule’ or something else, give us the lowdown, and we’ll sort it out!

Is it better to pay extra principal monthly or yearly?

Is it better to pay extra principal monthly or yearly?

Paying extra on your principal monthly is like choosing the express lane—it’s the fast track to reducing interest and shortening your loan term. But if once a year is what floats your boat, it’s still a solid move for your financial future.

What happens if I pay half my mortgage every 2 weeks?

What happens if I pay half my mortgage every 2 weeks?

Splitting your mortgage payment in half and paying it every two weeks is a nifty trick! It’s like sneaking in an extra month’s payment each year, which can cut down your loan term and save you a stash of cash in interest.

Can I use my credit card to pay my mortgage?

Can I use my credit card to pay my mortgage?

Hold your horses! While technically possible through third-party services, using your credit card to pay your mortgage isn’t usually the best idea. Those fees and high interest rates can turn your home sweet home into a sour financial pickle.

Does paying your mortgage twice a month save money?

Does paying your mortgage twice a month save money?

You betcha! Paying twice a month can help you knock a few bucks off the interest and sprint towards that mortgage-free finish line a tiny bit faster. Just confirm with your lender to avoid any potential snafus.

How much faster do you pay off a 30 year mortgage with biweekly payments?

How much faster do you pay off a 30 year mortgage with biweekly payments?

Switching to biweekly payments on a 30-year loan can have you doing a happy dance up to 4-5 years earlier than expected, all while saving you a boatload in interest. Pretty nifty, huh?

What is the best day to pay mortgage?

What is the best day to pay mortgage?

Honestly, there’s no “best day” set in stone, but making your payment a little early can give you peace of mind. Just make sure it’s before the due date to avoid any late fees or credit score dings!

How many years does paying mortgage weekly save?

How many years does paying mortgage weekly save?

Paying weekly can shave off a couple of years from your mortgage, just like biweekly payments. It’s all about making those extra contributions count towards whittling down that interest and principal.

Is it better to pay mortgage biweekly or weekly?

Is it better to pay mortgage biweekly or weekly?

Whether you go biweekly or weekly, both strategies can help you save on interest and cut down your mortgage faster than the traditional monthly grind. Choose what syncs best with your paycheck schedule.

What are the pros and cons of biweekly mortgage payments?

What are the pros and cons of biweekly mortgage payments?

Pros: quicker payoff, interest savings, budget-friendly. Cons: might have setup fees, requires budget tweaking, and not all lenders offer it. It’s like a financial seesaw, weighing the good with the less good!

What happens if I pay 2 extra mortgage payments a year?

What happens if I pay 2 extra mortgage payments a year?

Adding 2 extra payments a year is a smart play! It’s like giving your mortgage a double shot of espresso – it’ll perk up your payoff schedule and save you a latte money in interest.

What is the 10 15 rule mortgage?

What is the 10 15 rule mortgage?

Hmm, sounds like we hit a snag because the 10 15 rule isn’t a household name in mortgages. If you’ve got the inside scoop on it or were aiming for a different financial maxim, let us in on the secret and we’ll talk turkey!