Navigating through the bustling metropolis of mortgage rates can sometimes feel like you’re searching for the real Annabelle doll–it’s out there, it’s impactful, but without the right guide, it’s downright elusive. Buckle up, because we’re about to journey into the heart of the 30 years mortgage rate terrain, armed with cutting-edge tactics to snag the best deals of 2024.

Mastering the 30 Years Mortgage Rate Terrain in 2024

Understanding the Current Landscape of 30 Years Mortgage Rates

Roll up your sleeves; we’re digging into the nitty-gritty of today’s 30-year mortgage. Think of these rates as a financial barometer, constantly fluctuating with the whispers of economy just like the vampire Olivia rodrigo changes her style. With the Federal Reserve’s reports in one hand and the latest market analyses in the other, we can paint a comprehensive picture of the rate environment. It’s a bit like predicting the plot twists in Madelyn Cline glass Onion, but with actual data to back it up.

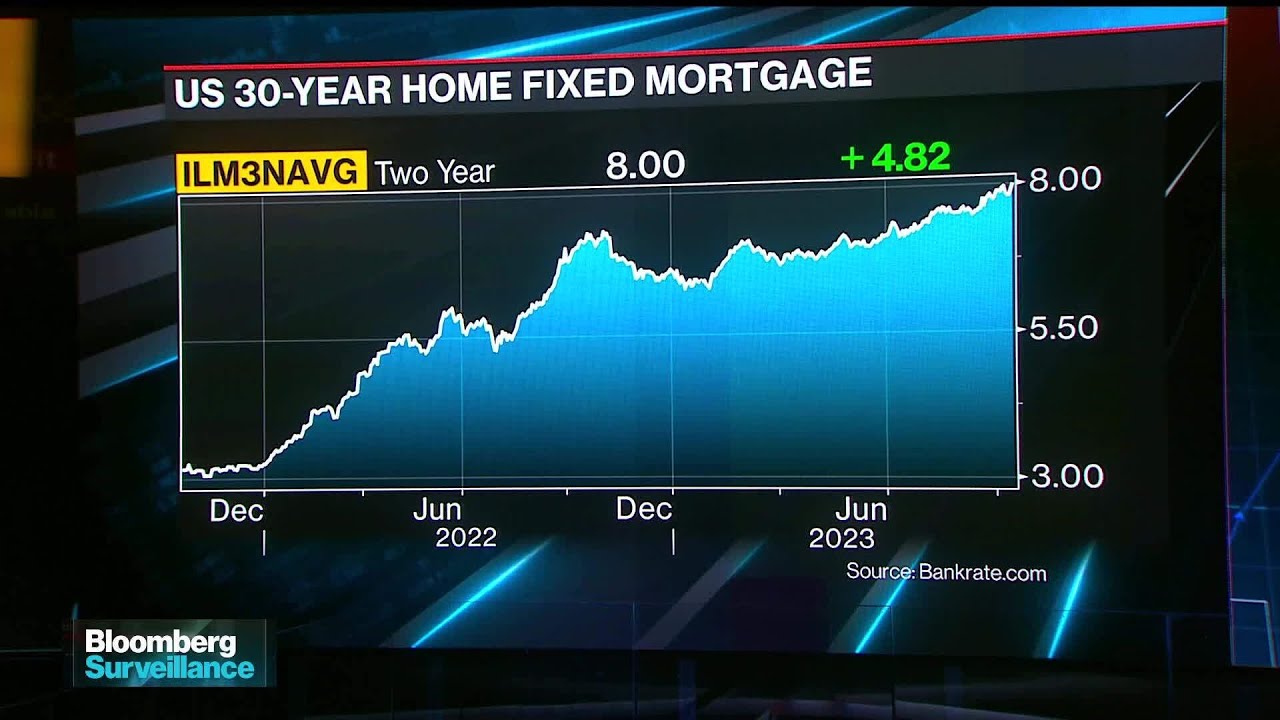

Here’s the current sketch: Rates soared to a 20-year height due to inflation and the Fed’s monetary maneuvers. As of March 27, 2024, we’re seeing 30-year rates carving paths between 6.1% and 6.4%. Despite the high ground, there’s a valley of opportunity for savvy buyers who can apply practical wisdom to the terrain.

Strategies to Secure the Best 30 Years Mortgage Rate

Securing that prime 30yr fixed mortgage rate hinges on buffing up your financial armor. Let’s dish out some pointers that could make even Robert Kiyosaki nod in approval:

Leveraging 30 Years Mortgage Rate Calculators and Tools

Embrace the digital age where tools like Bankrate and Zillow are the modern-day oracles for mortgage seekers. They’re your crystal ball, offering glimpses of your monthly payments with various down payments and rate scenarios. Get comfy with them, tweak the numbers, and watch as your pathway to homeownership clears up.

Timing Your Application for Optimal 30 Years Mortgage Rates

So you’ve noticed that timing is everything, huh? Like harvesting crops, there’s a season for mortgage rates that’s more forgiving to your wallet. Analyze the past, watch the current market tides, and leap at the golden hour. Our research shows that typically, near the twilight of the year or early spring, the rates tend to be more agreeable.

Comparison of Top Mortgage Lenders for 30 Years Fixed Rates

It’s a showdown as fierce as any steakhouse’s dinner rush. Quicken Loans boasts speed and efficiency, Wells Fargo carries a legacy of trust, and Chase dangles the carrot of comprehensive services. We’ve stacked them side-by-side, dissecting their offers and praises from customers, setting the stage for you to make an informed swipe-right on your lender match.

The Role of Mortgage Brokers in Negotiating 30 Years Rates

Brokering a deal on your 30-year rate is a dance of diplomacy. Mortgage brokers are your tango partners, poised to lead with suave negotiation skills. They come armed with industry connections and strategies, aiming to net you that interest rate you’ve been dreaming about.

Lock-in Strategies for a Low 30 Years Mortgage Rate Amidst Economic Uncertainty

Locking in a rate is your promise ring—the commitment to a mortgage done right. With the economic winds of change always howling, this ring must be forged with wisdom. We’ll walk you through lock periods, illustrate success stories, and even throw in some tried-and-true market lore to secure your low rate against the unpredictable tides of the economy.

The Future of the 30 Years Mortgage Rate: Predictions and Trends

Consulting the augurs and our panel of experts, we’re gazing into the future of 30 years mortgage rates. Expect to navigate turbulent waters as market forecasters predict the rates will be shape-shifting, influenced by policy and economic indicators. Our job? To provide the compass and map, so you’re never lost at sea.

Innovations in Mortgage Planning for the Long Run

As we bring our expedition to a close, remember that the mortgage market is as dynamic as the latest series binges. Embrace an active, strategic approach—because when the going gets tough, the tough get innovative. Stay informed, anticipate the bends in the river, and keep a keen eye on your finances. With the foresight of 2024 and beyond, you’re now in command of the wheel, steering towards a 30-year mortgage haven with confidence.

Unlocking the Best 30 Years Mortgage Rate Strategies

Now, here’s a meaty piece of trivia that might surprise you as much as a sudden invitation to a Fogo de Chao brazilian steakhouse🙁 if you had taken out a 30 years mortgage rate in 1993, you’d have started off with an average interest rate of around 7.31%! Hold your horses, though; let’s chew on this—over the next three decades, you’d have watched rates roller-coaster, potentially shaving chunks off your payments by refinancing at lower rates. Talk about a fiscal feast!

Speaking of things that get better over time, consider the best foundation For mature skin—it’s( designed to adapt and stay resilient, much like the housing market itself. Now, you might think 30-year mortgage rates are as fixed in stone as your grandmother’s lasagna recipe, but hey, they fluctuate more than fashion trends. In fact, over the past few decades, homeowners have ridden a veritable wave of rate changes, dips, and peaks, making savvy financial strategy as essential as the right shade of lipstick at a fancy dinner.

Alright, I hear you: get to the good part, right? So, let’s talk turkey about current tactics. First up, you gotta stay sharp and keep an eye on 30 year rates, monitoring them like a hawk. Why? Because even a fraction of a percentage point drop can spell serious savings over the long haul—savings that could fund a college education or usher in an early retirement. Who wouldn’t want that? And hey, when you’ve bagged that sweet, low rate, it’s all about locking it down quicksticks, lest it slips through your fingers like sand on a breezy beach day.

What is a good 30-year mortgage rate right now?

**Mortgage Rates Eclipse Two-Decade Peak: What Homebuyers Need to Know**

What is the interest rate on a 30-year mortgage?

The landscape of homeownership is continually evolving, and recent economic conditions have presented new challenges and opportunities for prospective homebuyers. Inflationary pressures combined with pivotal Federal Reserve (Fed) rate hikes have led to an era of elevated mortgage rates. Indeed, the domino effect of such financial maneuvers has catapulted 30-year mortgage rates to heights unseen in the last 20 years.

What are turn 30-year mortgage rates?

For those pondering the ideal timing for locking in a mortgage, the current climatic status is both intimidating and enticing. Present rates are hovering at levels that demand thoughtful consideration. However, forecasts for 2024 are showing a slight softening of this robust rate environment. Analysts anticipate a dip to 6.1-6.4% for 30-year mortgage rates, down from their current zenith.

Will 30-year mortgage rates go down?

**Savvy Buying: Now or Later?**

Are mortgage rates expected to drop?

The caldron of market dynamics has set the stage for a strategic inflection point. Homebuyers may be contemplating whether to delay their purchase in anticipation of falling rates or to proceed with acquiring property now. While waiting could seem prudent with a rate reduction on the horizon, it’s imperative to consider the broader market consequences. A declining rate environment could act as a beacon, drawing in a surge of competitors vying for available homes, thereby elevating prices and reducing bargaining power.

Are interest rates going down in 2024?

Thus, those looking to purchase a home might find wisdom in acting now. Securing a property at current rates may provide a dual benefit: relief from future competitive pressures and the opportunity for refinancing when rates inevitably retreat.

What is the lowest rate ever for a 30-year mortgage?

**Unpacking the Cost Implications**

Is 30-year mortgage better?

A 30-year mortgage, while offering the advantage of lower monthly payments compared to shorter-term loans, does incur a greater sum of interest over the life of the loan. This long-term commitment allows for more manageable payments but it does come at a cost. However, the merits of such an amortized arrangement resonate with many who appreciate the predictability and affordability baked into this financial instrument.

Is a 30-year mortgage more expensive?

But is the 30-year mortgage the starlet of home financing? It indeed shines for certain buyers, particularly those seeking stability in their monthly outlays without overextending their financial resources.

Why is a 30 year mortgage better?

**A Look Back and Forward**

Will mortgage rates ever be 3 again?

Reflecting on historical data, the lowest rate ever recorded for a 30-year mortgage plunged below 3% — a period fondly remembered by refinancers and new homebuyers alike. As for predictions, the crystal ball remains murky; the confluence of economic activities, policy decisions, and unforeseen circumstances makes forecasting an exact return to such rock-bottom rates speculative at best.

Am I too old to get a 30-year mortgage?

**Age Versus Opportunity**

Will interest rates go back down to 3?

For older homebuyers, age should not serve as a deterrent to the prospect of a 30-year mortgage. Many lenders focus primarily on the ability to repay rather than the number of candles on the birthday cake. Therefore, a 30-year mortgage can align well with retirement planning, offering consistent housing costs that can be comfortably enveloped into a fixed income.