When it comes to banking, the devil’s in the detail – and often, that detail is the fees. Which of the following financial institutions typically have the highest fees? This question isn’t just idle curiosity; it’s a pressing concern for anyone trying to stretch their dollar further. It’s time to roll up our sleeves and dig into the nitty-gritty of bank fees, so you can keep more of your money where it belongs – with you.

Exploring High-Fee Territories: Major Banks vs. Smaller Institutions

Let’s get to the heart of the matter: which of the following financial institutions typically have the highest fees? In the ring of finance, like a Vinny Paz boxing match, there are heavyweights and underdogs. The heavyweights, major banks, boast a broad reach and convenience, but they can pack a punch with their fees. Meanwhile, the underdogs, smaller banks and credit unions, may lack visibility but often offer a cost-saving fee structure that’s a true contender for your business.

Major Banks: A Look at the Giant’s Wallet

Smaller Institutions: David against Goliath

Do keep in mind, though, it’s not always cut-and-dried. Do your homework and compare specific fees before making a move.

How Debt Certificates Play Into Bank Fees

Now, about those debt certificates that are purchased by an investor, they’re a critical funding source for many banks. However, they can be accompanied by high issuance fees, especially if the associated institution leans heavily on this financing mechanism. So if you’re investing in these debt instruments or considering a bank known for issuing them, keep an eye on the associated fees that might trickle down to other banking services you use.

| Financial Institution Type | Typical Fees | Interest Rates on Savings | Interest Rates on Loans | Other Characteristics |

| A. Check Cashing & Payday Loan Companies | Highest fees for check cashing & short-term loans; might charge flat fees or percentages up to several hundred percent APR on payday loans | NA | Extremely high (can exceed 300% APR for payday loans) | Target individuals who need immediate cash; often criticized for predatory lending practices |

| B. Banks | Monthly maintenance fees, overdraft fees, ATM fees, loan origination fees | Lower compared to credit unions | Higher compared to credit unions | Offer a wide range of services and products; fees vary by bank and account type; larger banks typically have more extensive ATM and branch networks |

| C. Credit Unions | Lower or no monthly fees, minimal overdraft fees, lower ATM fees | Higher than banks | Lower than banks | Nonprofit and member-owned; tend to offer more personalized customer service; access to nationwide ATM networks through partnerships |

| D. Online Banks | Minimal to no monthly fees, lower overdraft fees, often reimburse ATM fees | Competitive, often higher than traditional banks | Competitive, can be lower than traditional banks | Operate primarily online; no physical branches; offer high-tech banking features |

The Impact of Savings Account Fees on Interest Earnings

In which situation would a savings account be the best investment to earn interest? Typically, when you can stow your cash in an account that has minimal fees and offers a competitive interest rate. But here’s the rub: Savings account fees can eat into your returns like termites in a Sun Valley lodge – silently and persistently.

Interest Earnings vs. Account Fees: The Duel

If you’re not careful, the fees could outpace your earnings, leaving you running to keep still.

Navigating the Waters of High Bank Fees

Remember this: Your financial institution can’t help you if there is a mistake on your bank account statement. Protect yourself by keeping tabs on your transactions and be proactive. If fees are eating your lunch, shop around. Many banks offer free checking with no strings attached — well, not many strings.

Strategies to Avoid High Fees:

Sometimes a little awareness and a change in habits can make a world of difference to your bottom line.

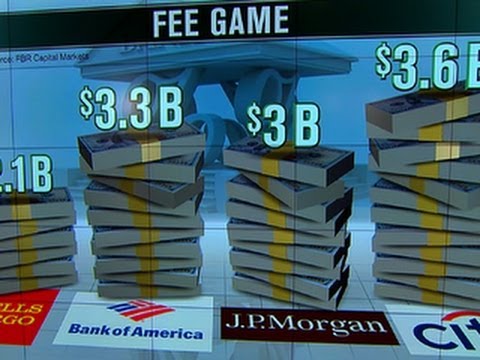

Comparing the Top Financial Institutions: Which Are the Most Expensive?

It’s quiz time! Which of the following financial institutions typically have the highest fees? If your answer includes check cashing and payday loan companies, ding ding, you’re spot on. These financial institutions are notorious for their exorbitantly high fees. Following closely behind are the major banks with their a la carte approach to service fees. Let’s look at the scorecard:

Armed with this intel, you can start to finetune where to park your money — or where to steer clear.

International Banks: Do They Charge More?

When dealing with international banks, you’re often playing in a different league. They may charge more, partly due to the complexities of operating across borders. Think currency conversion fees and international wire charges. If you’re involved in regular cross-border transactions, consider these costs before you leap.

Online Banks and Fee Structures: Are They Really Cheaper?

In this era of internet supremacy, online banks, unburdened by the costs of brick-and-mortar locations, often field lower fees. Which payment option Could have interest charged To You ? With online banks, traditionally, fewer scenarios exist where interest or fees accumulate — no maintenance fees, no minimum balance fees. They’re a breath of fresh air for fee-weary consumers, but always check the fine print.

Hidden Fees: What You Don’t Know Can Cost You

Hidden fees are the bane of any account holder’s existence — like grease on a doorknob, frustrating and hard to see. They can come in the guise of paper statement fees, account inactivity fees, and even fees for using a human teller. Institutions like payday loan companies are often the worst offenders.

Peel Back the Layers:

Knowledge is power, particularly when it comes to fee structures.

Negotiating Fees with Your Bank

What if I told you that you might be able to haggle your way out of some bank fees? Yes, it’s doable. It requires a blend of charm, evidence of loyalty, and sometimes just the sheer gumption to ask. It’s not guaranteed, but you’d be surprised at what a polite conversation can achieve.

Leveraging Technology to Track and Minimize Fees

Fintech has developed tools that can save you from the fee monster. Apps and online services can now provide real-time alerts on fees incurred and help manage your accounts more cost-effectively. They turn the tables on fees, giving you the upper hand.

Beyond the Fees: What Else Should You Consider?

Sure, fees are essential, but they are not the whole enchilada. You also need to weigh in on customer service quality, the diversity of banking products offered, and overall financial stability. A low-fee bank that’s always offline or unhelpful is no bargain.

On the Horizon: Are Bank Fees Changing?

As consumers become savvier and regulators turn their gaze to fee transparency, we’re seeing a slow but steady shift toward fairer fee practices. The landscape is changing, and continuous vigilance is vital to ensure it changes in your favor.

Side-Stepping Steep Costs: A Strategized Financial Approach

Managing your financial life strategically can protect you from steep fees. It’s about more than just looking for the lowest charges; it’s also about aligning your banking choices with your lifestyle and financial goals to create a tailored and cost-effective financial ecosystem.

You now have the inside scoop on which of the following financial institutions typically have the highest fees and how to dodge them. Stay informed, stay vigilant, and remember, sometimes the best savings are the fees you avoid paying. Here at Mortgage Rater, we’re in your corner, helping you fight the good fight for a better financial future. Keep an eye on the horizon, but never lose sight of the day-to-day battle against fees. With knowledge as your weapon and strategy as your shield, you’re ready to claim victory over the costs that lurk within the fine print. Aim high, spend smart, and save wisely.

What financial institution typically have the highest fees?

Oh boy, when it comes to fees, brick-and-mortar traditional banks usually win the race to the top. With a plethora of services that cost a pretty penny to maintain, they often pass on these costs to us, the consumers, unfortunately. So, if you’re wallet-conscious, these might not be your go-to choice for low fees.

Which type of financial institution typically charges the highest interest rates for loans?

All right, let’s talk loans. Payday lenders are notorious for charging eye-watering interest rates. With their short-term loans that can lead you down a rabbit hole of debt, they’re the ones to watch if you’re looking to avoid sky-high costs.

Which financial institution is likely to have the lowest fees?

Now, on the flip side, online financial institutions or credit unions are often your best bet for low fees. Without the burden of maintaining pricey branch networks, they’re in a prime position to cut us some slack on the fee front.

Which type of bank account typically offers the least if any interest?

If you’re hunting for interest, a traditional savings account won’t be your golden goose. Typically, these accounts offer minimal, if any, interest – talk about a snooze fest for your savings!

Do banks have high fees?

When it comes to banking fees, sure, they’re as common as rain in April. Banks often sport a collection of fees that could give a diner menu a run for its money, with everything from monthly maintenance to ATM withdrawal fees.

What is the largest source of fees for banks?

Ah, the main money-maker for banks? Overdraft fees take the cake, often catching us off guard and hitting where it hurts – our wallets!

Which types of loans usually cost the most?

Alright, let’s get this straight: payday loans usually top the charts as the costliest. With stratospheric interest rates that can leave you reeling, they’re the heavyweight champions of expensive loans.

What are the fees charged by banks that make borrowing more expensive called?

The sneaky culprits that ramp up the cost of borrowing from banks? They’re called “finance charges,” wrapping all those pesky interest payments and fees into one bitter pill.

Who charges the higher interest rate a bank loan or credit card?

Credit cards, hands down, tend to have higher interest rates compared to most bank loans. With rates that can skyrocket faster than a rocket, it’s best to keep a tight leash on that plastic if you want to keep your finances grounded.

What are the top 4 financial institutions?

Phew, the big players in the finance game? They’re typically commercial banks, credit unions, online banks, and brokerage firms. These heavyweights each bring something unique to the table.

What type of bank doesn’t have fees?

Looking for a no-fee oasis? Online banks and credit unions often wave goodbye to fees, giving your wallet a much-needed break.

What type of fees could be associated at a financial institution?

Fees at financial institutions come in all shapes and sizes, from monthly maintenance fees to pesky overdraft charges. They can nibble away at your balance like a mouse in a cheese shop.

Which type of bank account has the highest interest?

If you’re chasing the highest interest, your best shot’s with a high-yield savings account. These are the superheroes of the banking world when it comes to interest rates.

On which account banks provide a higher rate of interest?

In the world of bank interest, certificates of deposit (CDs) are where it’s at. Lock your money away for a set time, and you’ll be welcomed with higher interest rates that’ll make your savings smile.

What fees does Chase Bank charge?

Chase Bank? Oh, they’ve got a lineup of fees from monthly maintenance to insufficient funds that’ll make you think twice before going tap-happy with your debit card.

What investment firm has the highest fees?

The investment firm landscape can be a minefield of fees, but hedge funds often lead the charges with fees that can make even a high roller blink.

What is the largest and most common checking account fee?

Talk about a buzzkill — the most common checking account fee is for overdrafts. It’s like a slap on the wrist every time your balance waltzes below zero.

What investment comes with higher fees?

Investing isn’t all fun and games, especially when dealing with actively managed funds. They come strapped with higher fees than their passive counterparts, potentially chomping into your returns.

Why do banks have higher fees?

Banks, with their sprawling physical networks and full suite of services, often cite these factors as reasons for their higher fees – they’ve got to pay the bills somehow, right? But for us users, that often means digging deeper into our pockets. Keep a watchful eye and play your cards right to avoid fee landmines!