Demystifying the Principal of a Loan: A Comprehensive Analysis

Ah, the principal of a loan, a term so commonplace in the finance universe, yet as clear as mud to many folks navigating the complex waters of borrowing. Let’s face it; when the chips are down, knowing exactly what is the principal of a loan can make a world of difference in your financial dealings.

Understanding this bad boy is pivotal for both borrowers and investors—it’s the meat and potatoes of your loan diet. Grasping its essence can mean the difference between a manageable financial commitment and a runaway debt train.

Loans come in all shapes and sizes, and principal is the star throughout their lifespans. From mortgages to car notes, every loan tells a tall tale of how its principal shrinks or balloons over time. Buckle up; we’re taking a deep dive into interest payable and the life of loan principals.

Principal Definition Finance: The Backbone of Your Loan

So, what’s this “principal” ballyhoo all about? In finance-speak, the principal is the main event—the original lump of cash you borrow from a lender and promise to pay back. It’s the foundation on which the castle of your loan is built.

This concept isn’t some newfangled idea; it’s been around since folks decided trading chickens for goods wasn’t going to cut it. Every financial system, past and present, has its own way of calculating and managing the principal. However, whether you’re dealing with yesteryear’s tally sticks or today’s blockchain, the endgame remains the same—balancing the books.

| Attribute | Description |

|---|---|

| Definition | The principal of a loan is the original sum of money borrowed from a lender. |

| Constituents | Only the borrowed amount, excluding interest. |

| Role in Monthly Payments | Monthly payments are divided into a portion that reduces the principal and a portion that pays interest. |

| Impact on Loan Term | Paying extra on the principal can shorten the loan term and reduce the total interest paid. |

| Loan Interest Relationship | Interest is calculated based on the remaining principal; as it decreases, so does the interest portion of future payments. |

| Principal Advance | A specific disbursement of principal, without interest, provided to the borrower during the loan term. |

| Effect of Early Repayment | Additional payments made solely towards the principal can lead to significant savings on interest and faster loan payoff. |

| Example (For a $200,000 loan) | If you borrow $200,000, that amount is the principal. Your payments will reduce this amount, plus pay the interest agreed upon. |

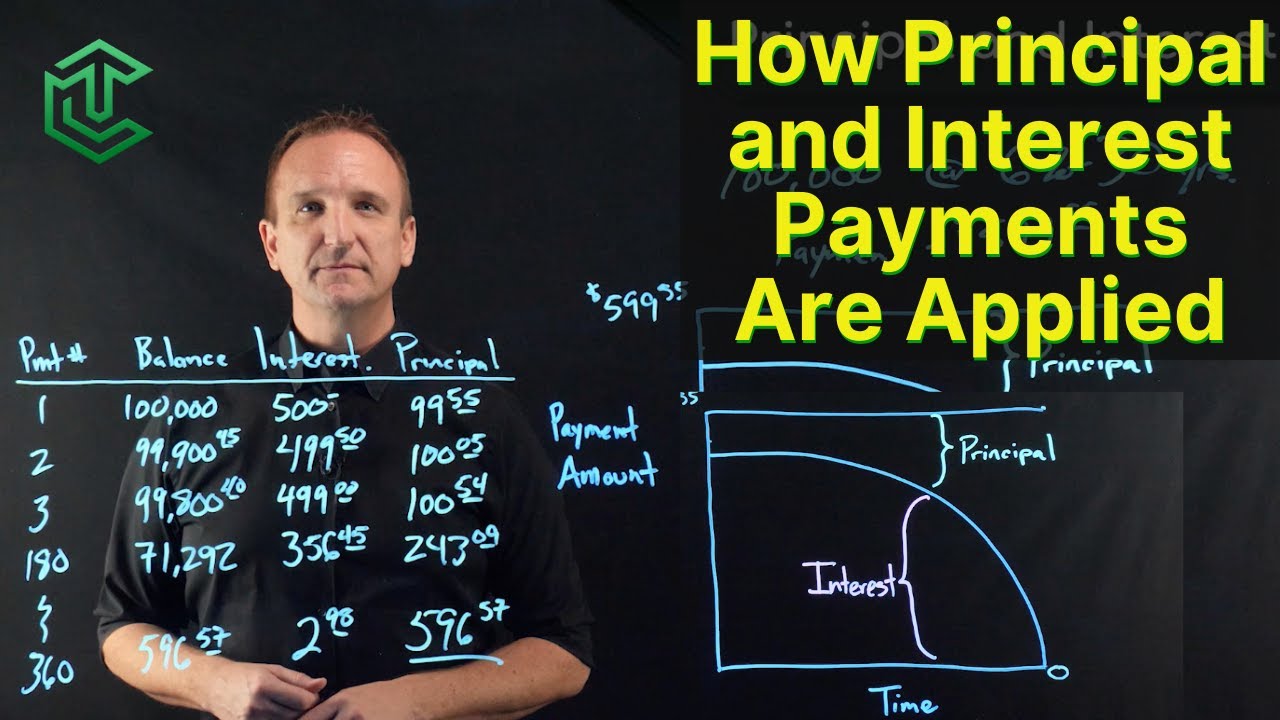

Principal vs Interest: Dissecting Your Loan Payments

Roll up your sleeves; we’re about to slice and dice the principal and interest to see how they tick. Think of your loan payment as a Thanksgiving turkey. The principal is the meat you’re trying to gobble up, and the interest is the stuffing—a necessary evil that can sometimes take up too much space on your plate.

Visual aids like charts and graphs paint a thousand words, depicting how each payment slowly chips away at the mountain that is your principal, while the interest acts like a clingy sidekick. Imagine Joe, who took out a loan for his waterfowl business—his story showcases the dance between principal and interest as he navigates the waters of repayment.

Interest Payable Over Time: How It Relates to Your Loan’s Principal

Curious about this interest payable? It’s the price tag on your borrowed bucks—the extra dough you pass along to your lender for the privilege of using their money. Let’s say you got your hands on a principal amount; the interest is what keeps the clocks at the bank ticking.

Want to minimize that interest? Short story: the faster you reduce your principal, the less interest you pay. It’s like trimming the fat off your steak—the leaner it gets, the less there is to cook. Financial gurus will tell you to hit the principal hard and fast for a leaner loan life.

What Is the Principal of a Loan in Various Financial Products?

Speaking of mortgages, if home sweet home is your goal, building equity is all about knocking down the principal. The auto loans scene is a different kettle of fish; cars depreciate faster than you can say “oil change,” impacting the principal. “Loans right now” are also an intriguing gambit for those in immediate need of a cash injection.

For the knowledge-hungry, student loans offer a lesson in principal management—knowing the difference between subsidized and unsubsidized can save you major bucks. And let’s not forget the entrepreneurs—the principal in business loans is the rocket fuel for your growth or day-to-day operations.

The Tactical Side of Principal: Prepayments and Loan Strategy

Can we talk strategy? Making prepayments on your principal might sound as delightful as finding extra fries at the bottom of the bag, but it can have its disadvantages, like in paying off a car loan early. It’s a tango between saving on interest and dodging potential pitfalls, so you’d better learn the steps.

Every loan has its unique beat—some encourage early principal payments, while others slap on penalties like a stern schoolmaster. It’s a global phenomenon, with prepayment strategies varying as widely as local delicacies.

Principal Over Time: Amortization and Its Financial Implications

Amortization—sounds as heavy as a Sunday roast but it’s simply how a loan’s principal and interest are spread over time. Imagine a pie chart showing your payments hugging the curves of an amortization schedule; each slice getting closer to being debt-free.

But don’t forget, refinancing or tweaking your loan can shake up your principal like a polaroid picture. Insights from the financial analyst crowd can help you navigate these waters without capsizing your financial boat.

Interest Rates and Their Influence on the Principal of Your Loan

Now, pull up a chair while we gab about interest rates. These numbers can play nice or rough with your principal—it’s all about timing and trends. Keeping an eye on the forecast can mean the difference between smooth sailing and rough seas for your loan’s lifecycle.

Central banks play maestro to the orchestra of interest rates. Their wand-waving can see your principal dance to a tune that either hastens or hinders your debt-paying journey.

Protecting Your Principal: Risk Management in Loan Agreements

Loan agreements aren’t just fine print and legalese; they’re a treasure map guiding you to protect your principal from marauders and storms. Some consumers have tales more gripping than a detective novel when it comes to outmaneuvering risks to their principal.

Insurance and other clever financial products are the lifeboats designed to keep your principal safe from the angry seas of uncertainty.

Technology and Loan Principal: The Future of Borrowing

Fintech is turbocharging the loan landscape—these brainy bots and algorithms are becoming ace pilots in the cockpit of principal management. With AI steering the ship, future captains of industry might navigate loan repayments with the deftness of seasoned sailors.

Places like emerging markets, where technological adoption can be patchy, stand to benefit from such advancements—watching them catch up is like witnessing a caterpillar turn into a butterfly.

Behind the Scenes: The Role of Principals in Loan Securitization

When loans go Hollywood and get securitized, it’s the principal that gets top billing. This star of the show influences the value of securities—movie execs in the loan biz call these collateralized debt obligations or CDOs. Here, our waterfowl entrepreneur, Joe, might find his loan principal bundled with others, creating a blockbuster financial product.

Have a look at the securitization market—it’s the talk of the town. Its future is as hotly debated as the finale of your favorite TV saga.

Innovative Wrap-Up: Charting Your Financial Voyage with Loan Principals in Mind

Let’s stitch this patchwork of wisdom into a quilt you can snuggle under for financial comfort. Keeping your loan’s principal in check is like mastering the compass of your fiscal ship.

As the financial seas chop and change, the perception and handling of loan principals are evolving faster than a blazer dress at fashion week. The future points to a more tailored approach to loan management, where the principal is both the constant and the variable in the equation of personal wealth.

Anchor down, because your understanding of what is the principal of a loan just got a whole lot richer. And who knows? With this guide in hand, your voyage towards financial enlightenment might be smoother than you ever dreamed possible.

Is it better to pay interest or principal?

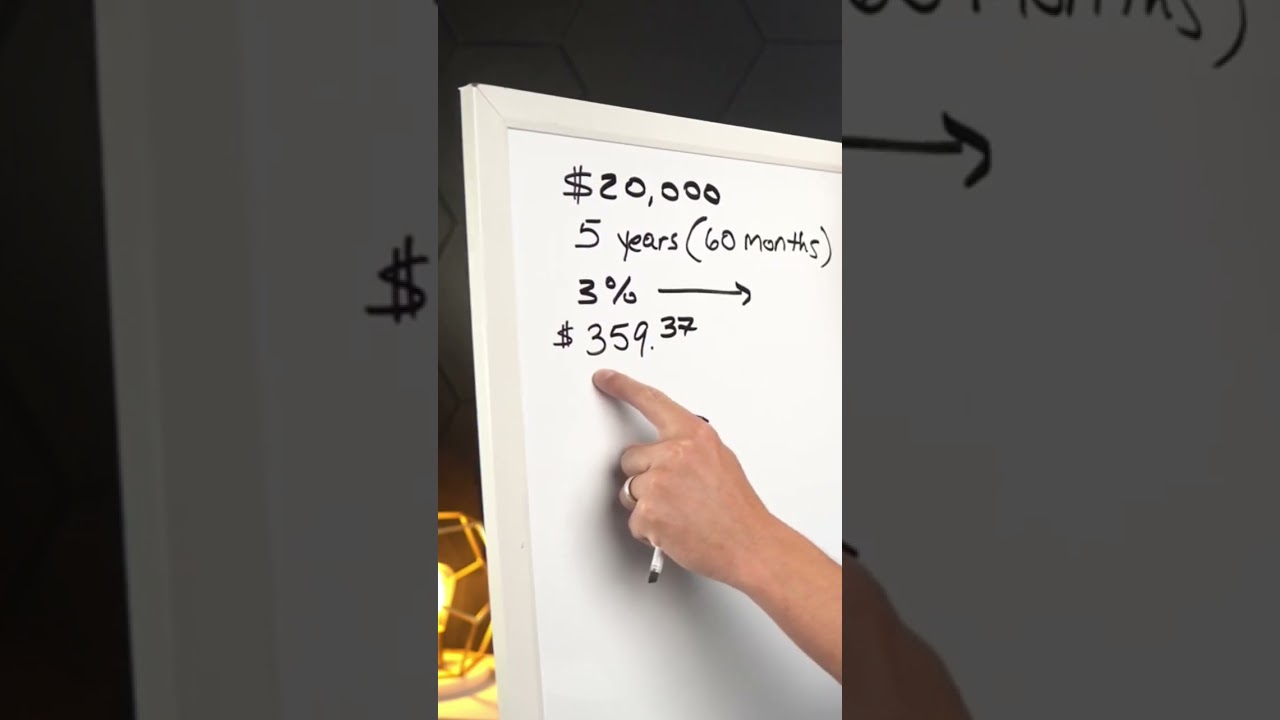

Well, isn’t that the million-dollar question! When you’re balancing your checkbook, you might wonder if it’s better to throw your hard-earned cash at the interest or the principal of your loan. Here’s the deal: paying down the principal reduces the balance quicker, which means you’ll pay less interest over time. It’s like hitting two birds with one stone.

What is the principal of a loan quizlet?

Quiz yourself on this: the principal of a loan is the actual amount you borrowed, not a penny more or less. Picture it as the heart of what you owe, while interest is like the pesky mosquitoes buzzing around, racking up what you gotta pay back over time.

What is a principal advance on a loan?

Getting a principal advance on a loan sounds fancy, huh? It’s pretty much when you get an extra sum of money on top of what you borrowed initially. Think of it like getting a cash top-up, but don’t forget it’s not free money — it adds to your debt, increasing the principal amount you’ve gotta pay back.

What happens if I pay an extra $100 a month on my car loan?

Oh, the sweet sound of shaving down debt! Tossing an extra $100 a month at your car loan does wonders. You’ll be out of debt faster than a kid running towards an ice cream truck and, bonus points, you’ll pay less in interest over the life of the loan. It’s a win-win!

Do extra payments automatically go to principal?

Wouldn’t it be peachy if extra payments magically found their way to your principal? Well, you might have to give your lender a nudge. They don’t always automatically apply extra dosh to your principal, so ring ’em up or check your online account to make sure your money’s going where you want it to.

What is principal in loan interest?

Interest is the pesky little sidekick to your loan’s principal — it’s the cost of borrowing money. Think of the principal as the main slice of your debt pie, while the interest is like the crumbs that keep adding up until you’ve polished off the whole thing.

What is principal in terms of debt?

If we’re talking debt lingo, ‘principal’ refers to the meaty portion of what you owe — ya know, the amount you snagged as a loan before interest turned it into a growing beast.

Does interest disappear if you pay off the principal?

No, wiping out your principal doesn’t make interest vanish into thin air. It’s like cutting weeds in your garden; you chop ’em down, but you still gotta deal with the ones that popped up earlier. So, you’ll still owe interest that’s piled up to that point, but once the principal’s gone, interest stops growing.

Why am I paying more interest than principal?

Ever feel like you’re in a hamster wheel, paying more interest than principal? It’s ’cause most loans have an amortization schedule that’s front-loaded with interest, meaning early payments are mostly interest, and it’s like you’re running but not getting anywhere with the principal.

What is an example of a principal payment?

Imagine you buy a fancy new gadget on credit. When you pay back part of what you originally spent, that’s a principal payment. It’s like hitting the undo button on a part of your debt—simple as that.

What happens if I pay principal only?

Dive headfirst into paying principal only and you’ll see your loan shrink faster than a snowball in the sun. But keep an eye out! Some loans have prepayment penalties or specific rules about this, so you don’t want to get tripped up by the fine print.

Is paying principal worth it?

Is paying down your principal worth it? As worth it as an umbrella in a rainstorm, my friend. It slices through the interest you’ll end up paying and can set you free from debt’s chains sooner. If you can swing it, it’s a savvy move.

What happens if I pay an extra $500 a month on my mortgage principal?

Picture this: an extra $500 a month cascading onto your mortgage principal. It’s like a magic potion for your loan, significantly slashing the interest and potentially knocking years off your mortgage. It’s the heavyweight champ of overpayments!