Understanding the Impact: If I Pay Extra on My Car Loan Does It Go to Principal?

Introduction to how car loans work

Let’s dive right into the thick of it, folks. You’ve got yourself a car loan, and you’re wondering, if I pay extra on my car loan, does it go to principal? It’s a smooth ride ahead as we unravel the nuts and bolts of how your car loan works. When you finance a car, you’re borrowing a sum of money from a lender to purchase your new set of wheels. This loan comes with a specific repayment schedule, interest rate, and, if you’re not careful, some twists and turns that could make your journey costlier than you’d like.

The concept of principal vs. interest on a car loan

In the financial world, there’s nothing more critical than understanding the dance between principal and interest. At the heart of your car loan, we’ve got the principal – the chunk of change you borrowed initially and promised to pay back. Each month, part of your payment reduces the principal, while another slice covers the interest, which is like the lender’s rental fee on the money you’ve taken for a spin.

Common terms associated with paying off car loans early

When you aim to pay off that car loan early, you’ll encounter some lingo. “Prepayment penalty” might sound ominous, and rightly so, because some lenders will charge you for the privilege of paying back your loan ahead of time. Another term you’ll want to know is “principal-only payment.” As of October 23, 2023, paying extra money towards the loan’s principal is called a principal-only payment. Armed with these terms, you’re ready to put pedal to the metal and pay off that loan sooner than expected.

Strategies for Principal Reduction: Making Principal-Only Payments

What are principal-only payments?

Imagine directing all your hard-earned cash straight to the principal balance of your car loan. That’s what a principal-only payment does – it drives down the amount you owe without touching the interest that’s still warming up in the garage.

How to make sure your extra payment goes to the principal

Not all auto loans are created equal, and every lender shifts gears differently when it comes to extra payments. Often, if you simply send in more than the monthly due, that extra dough might be applied to future payments rather than eating away at your principal. To make sure your payment packs the punch you intend, get in touch with your lender directly and tell them you want your extra payment to be a principal-only payment.

Discussion on lender policies regarding extra payments

Every lender has their own roadmap when it comes to handling extra payments, and as of October 23, 2023, you have to specify how those payments should be applied. It’s like telling your GPS exactly where you want to go – otherwise, who knows where you’ll end up!

| Aspect | Detail |

|---|---|

| Payment Type | Principal-Only Payment |

| Application of Extra Payment | Must specify to lender to apply extra payment to principal. Otherwise, it may not automatically reduce principal amount. |

| Immediate Impact | Monthly payment amount remains the same but total loan term reduces, leading to an earlier payoff. |

| Interest Savings | Paying extra on principal reduces the interest paid over the life of the loan, especially if the interest rate is high. |

| Payment Frequency Benefit | Semi-monthly payments reduce principal more quickly and save on compounded interest. |

| Prepayment Penalty | Some lenders may charge a prepayment penalty for paying off the loan early. |

| Cash Flow Considerations | Extra payments mean less cash available for other debts or investments. |

| Risk of Being Upside Down | Early in the loan term, making minimum payments means more of your payment goes towards interest, risking owing more than the car’s value. |

| Long-term Financial Impact | Paying off the loan faster may improve credit and long-term financial health, though it could restrict cash on hand for investments or emergencies. |

Evaluating the Effects on Loan Amortization

Definition of loan amortization

Amortization sounds like a hefty word, but it’s simply the plan for how you’re going to pay off that car loan over time. It schedules your monthly payments so that, gradually, you’re switching lanes from paying more interest to more principal.

How extra payments influence your loan’s amortization schedule

Throw extra payments into the mix, and you’ll notice changes in your loan’s amortization schedule. Rather than spreading out your payments over the full term, you’re putting the brakes on interest and speeding towards full ownership a lot faster.

Long-term benefits of reduced loan term

When you shorten the life of your loan with extra payments, the long-term perks are as sweet as they come. You’re looking at potentially saving a bundle on interest and the sheer joy of owning your car outright sooner than you might have thought possible.

The Financial Advantages of Paying Extra Towards Your Car Loan

Interest savings over the life of the loan

Alright, let’s talk turkey. By paying extra towards your car loan, you’re not just cutting down on the total interest costs – you’re coming out ahead in the big financial race of life. This is especially true if you lock in those extra payments early on when interest is taking a bigger slice of your monthly payment pie.

Enhanced equity in your vehicle

Paying extra towards your loan also boosts your equity, which is the part of the car you truly own versus what you owe on it. Think of it as building a financial cushion that can come in handy if life throws you a curveball.

Improving your debt-to-income ratio

Extra payments on your car loan can also polish up your debt-to-income ratio, making it easier to invest in a home or get favorable terms on future loans. It’s like slimming down your financial waistline, making you a more attractive prospect for lenders.

Potential credit score benefits

Sure, every credit score journey is unique, but consistently chipping away at your car loan can reflect positively on your credit history. Just like a star athlete’s stats, a strong payment history can bolster your creditworthiness in the eyes of future creditors.

Overcoming the Challenges: What to Consider Before Making Extra Payments

Evaluating your overall financial health

Now hold your horses for a minute. Before you put extra cash into your car loan, you’ve got to examine the big financial picture. Is your job stable? Do you have other debts nipping at your heels? You want to make sure that accelerating your car loan payments won’t veer you off course elsewhere.

Weighing other debts and interest rates

Your car loan might have a co-star in the form of a mortgage, student loan, or credit card debt. Where’s the interest gnawing away the most? That’s where you need to tackle first. It’s like putting out the biggest fire before hosing down the smaller flames.

Understanding prepayment penalties

Remember those pesky prepayment penalties? They might just be lurking in the fine print, waiting to take a bite out of your wallet if you pay off that loan early. It could be a flat fee or a percentage of your remaining balance – either way, it’s something to suss out. But don’t let that discourage you! Look at the Disadvantages Of paying off a car loan early to weigh the pros and cons.

The importance of emergency funds

In the juggling act of life, keeping an emergency fund as your safety net trumps paying off debt early. Life can throw some curveballs, and having a stash of cash helps you deal without totaling your financial plans.

Real-Life Scenarios: How Extra Payments Can Shift Your Financial Landscape

Case studies illustrating the impact of extra payments

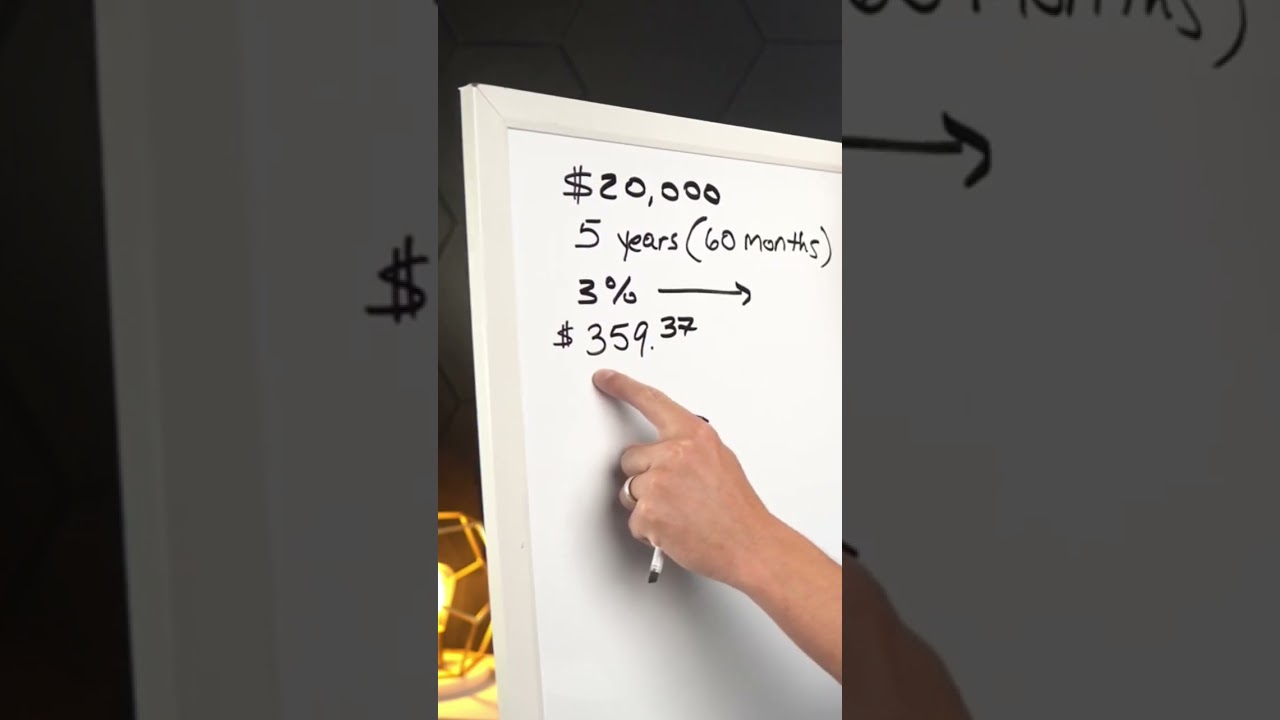

Let’s jump into some real-case scenarios because nothing speaks louder than the truth. Imagine Jane, who started with a $20,000 car loan at 5% interest over five years. After calculating her potential interest savings, Jane decides to make an extra $100 payment straight to her principal each month. She shaves off a significant chunk of interest and her journey to car ownership takes a shortcut.

Analysis of different payment strategies

You might also consider splitting your payment in half and paying twice a month, known as a semi-monthly payment strategy. Why bother? Because on an auto loan, interest compounds daily, and by paying half your payment early, you’re tapping the brakes on the principal, which helps reduce the overall interest pile-up.

Personal testimonials on the advantages of reducing loan principal

It’s not just theory – talk to folks who’ve taken this road, and they’ll beam about the financial breathing room they found by making principal-only payments. They’ll tell tales of lower interest payments, faster debt clearance, and the sweet freedom of owning their car outright way ahead of schedule.

Navigating Lender Terms: Ensuring Extra Payments Work for You

How to communicate effectively with your lender

Having a heart-to-heart with your lender is essential. It’s about making sure everyone’s singing from the same hymn sheet. When you’re on the phone with them, don’t be shy – get confirmation that your extra payments will target the principal. It’s about steering that financial vehicle exactly where you want it to go.

Confirming your payment is applied correctly

Even after you’ve had the talk with your lender, keep a keen eye on your statements to ensure your payments are hitting the mark. Errors happen, and the earlier you catch them, the smoother your journey to a paid-off car will be.

Pitfalls to avoid when making extra car loan payments

And here’s where you want to avoid some common potholes. Don’t get so wrapped up in paying off your car loan that you neglect other high-interest debts. Also, as attractive as lowering debt is, it shouldn’t come at the cost of your retirement savings or emergency fund.

Tools and Calculators: Projecting Your Car Loan’s Future

Overview of online payment calculators and how to use them

In this digital age, you’ve got some nifty online tools right at your fingertips to help you plot the course of your car loan payoff. Online payment calculators can give you a quick forecast of how extra payments will transform your loan’s horizon.

Apps and tools to track your loan and payments

Let’s not forget about apps and tools tailored for keeping your loan in check. They’re like having a financial buddy in your pocket, providing real-time updates and nudges when it’s time to make a payment.

Creating a personalized amortization table for your car loan

Feeling crafty? Why not create a custom amortization table? It’s a powerful way to visualize how each extra payment fuels your ride to becoming debt-free. It’s like mapping your financial road trip – the more detailed your map, the smoother the journey.

Advanced Payment Techniques: Lump Sum vs. Incremental Extra Payments

Comparison of different extra payment methods

When turbocharging your car loan, you’ve got two sexy options: lump sum payments or the more subtle approach of incremental extra payments. It’s a bit like choosing between a drag race and steadily gaining speed on the highway – both will get you to the finish line, just in different styles.

Analyzing the impact of lump sum payments on loan principal

Lump sum payments are like dropping a financial bomb on your principal. They can lead to drastic decreases in your overall interest and shorten the life of your loan in one fell swoop.

The case for periodic extra payments and their benefits

On the flip side, periodic extra payments might feel more manageable and can still offer significant savings on interest and a shorter loan term. It’s about persistence and small, sustained efforts that can add up to big achievements.

Adapting to Life Changes: When to Adjust Your Payment Strategy

Coping with financial hardships

Life isn’t always as smooth as freshly laid asphalt. If hardship hits, like job loss or unexpected expenses, it may be time to review and possibly ease off the extra car loan payments. Your financial health is the priority – keep it in fighting shape!

Leveraging windfalls wisely

Now imagine a lucky windfall comes your way – a tax refund, bonus, or inheritance. While the temptation to splurge is real, consider dropping a chunk of that windfall on your car loan. It’s a way to invest in your financial future rather than just indulge in the present.

Adjusting your payment plan in times of low-interest rates

Economic climates change, and so do interest rates. In times of low rates, you might find it more beneficial to invest spare cash rather than pay down low-interest debt. You’re playing the long game here, and sometimes, waiting for your shot can pay off bigger than a quick move.

The Future of Car Loans: Predicting the Path Ahead

Trends in car financing and how they affect loan repayments

As we gaze into the crystal ball of car financing, we see innovations and changing trends that could benefit your loan repayment strategy. There might be new loan products on the horizon that cater to borrowers looking to pay off their loans early. Remember, the loan landscape isn’t static – it’s a living, breathing ecosystem that evolves.

New loan products that accommodate early repayment

Lenders are catching on to the fact that borrowers love the flexibility. Newer loan products might just come with fewer strings attached when it comes to early repayment. It’s like loan providers finally figured out that one size doesn’t fit all.

Anticipating changes in interest rates and their implications

Interest rates tend to ebb and flow like the tide. In the coming years, shifts in the interest rate could either encourage you to pay off your loan more quickly or may suggest stashing your extra cash elsewhere. It’s all about reading the weather and adjusting your sails accordingly.

Beyond the Payments: Achieving Financial Freedom with Your Vehicle

Broadening your financial goals after paying off your car loan

Once you own that car free and clear, other financial peaks are there for the taking. Maybe you’ll start saving for a down payment on a house, build a robust emergency fund, or start a business. The world’s your oyster, and you’ve got a vehicle to take you there – metaphorically and literally.

Planning for your next car purchase or investment

Even as you celebrate that final car payment, it’s wise to look ahead. Start planning for your next car purchase or other significant investments. What’s the next destination on your financial road map?

Tips for maintaining financial discipline

Now, here’s the kicker – the same discipline that helped you pay off your car loan? Apply it to the rest of your financial journey. That’s how you build a legacy of smart money moves, one step at a time.

Driving Towards Financial Success: The Long-Term View of Car Loan Repayment

Visualizing the future without a car payment

Picture a future without car payments – what does that look like for you? Perhaps it’s more freedom, more savings, maybe even a vacation or two. By paying extra on your car loan when you can, you’re making that dreamy picture a reality.

How paying extra on your car loan fits into retirement planning

And let’s not forget the big retirement party down the road. Paying off your car loan early is like setting up the foundation for a stress-free retirement – one where you’re not bogged down by debt.

Tailoring your car loan payment strategy to match life’s milestones

No matter what stage of life you’re cruising through – be it welcoming a child, changing careers, or looking to downsize – your car loan payment strategy can be tweaked to fit snugly around your life’s events. It’s about making your money work for you, no matter what route you take.

As we pull into the final leg of our journey, let’s recap. When you ponder, if I pay extra on my car loan, does it go to principal? Remember, it can, but only if you navigate the process wisely. Keen knowledge on principal-only payments is just like having the best navigational system in your financial vehicle. Ensure every extra dollar you pour into your car loan takes you closer to your destination – a car that’s wholly, gloriously yours, and a financial status that you can rev with pride. It’s all about mastering the art of loan payments to propel your financial situation into the fast lane of success. So, keep those engines running, your eyes on the road, and here’s to smooth driving on the road of financial freedom.

Ready To learn more about car Loans right now ? Get in gear and steer yourself towards more informed decisions with the comprehensive guides and insights at your disposal. Happy travels and smart repayments ahead!

What happens if I pay extra on my car loan?

If you toss some extra cash at your car loan, you’re shortening the road to owning it outright. Think of it this way: Pay more now, and you’ll chip away at that principal balance, leading to less interest paid over time. Your wallet will thank you later!

Is it better to make 2 car payments a month?

Splitting your monthly car payment into two bi-weekly payments might seem nifty—it’s like giving your payment plan a little more pep. Yet watch out, it could lead to a smoother ride financially by potentially reducing the interest you’ll pay.

What are the disadvantages of paying off a car loan early?

Rushing to pay off that car loan early? Hold your horses! While it feels good to be debt-free, you might face prepayment penalties, lose a bit of your credit score’s oomph, or miss the chance to use that cash where it could work harder elsewhere.

Is it worth it to pro long auto loan and pay more than the principal?

Hmm, prolonging your auto loan to pay more than the principal? That’s like taking the scenic route when you’re in a hurry. Sure, smaller payments now might give your monthly budget some breathing room, but you’ll end up paying more in interest by the time you reach your destination.

How long does it take to pay off a $20000 car?

Paying off a $20,000 car loan feels like a marathon, doesn’t it? Depending on the interest rate and your monthly payments, it could take anywhere from a couple of years to six years or more. Stay steady and you’ll cross that finish line!

What is the fastest way to pay off a car loan?

Want to fast-track your car loan? Hit the gas on payments! Increase the amount you pay each month, make additional payments when you can, and consider refinancing for a lower interest rate. Vroom, vroom—bye-bye, loan!

How to pay off a 6 year car loan in 3 years?

Crushing a 6-year car loan in half the time? You’ve got the need for speed! Double down on those monthly payments, throw any extra cash bonuses or tax refunds at the balance, and cut back on non-essentials. It’s like putting your loan on a treadmill – it’ll slim down fast!

Is a 72-month car payment bad?

A 72-month car payment? That’s one long road trip with your loan. Sure, the monthly payments are smaller, but you’ll shell out more dough in interest. Plus, you risk owing more than the car’s worth down the line—it’s a bit of a bumpy ride.

Is 500 a month car payment a lot?

Dropping $500 a month on a car payment sure sounds steep, almost like climbing a financial Everest. It really hinges on your income and budget. If it’s more than 15-20% of your monthly take-home, then yeah, that’s pretty hefty!

Can I pay off a 72 month loan early?

Can you bail out of a 72-month loan early? Absolutely! Just be sure to check for prepayment penalties. Breaking free early means you’ll save on interest and dance your way out of debt sooner.

How can I avoid interest on my car loan?

Dodge that interest like it’s a pothole! To swerve clear, think about making larger or more frequent payments, refinancing for a better rate, or picking a short loan term. And hey, driving off the lot with a cheaper or used car also keeps the interest gremlins at bay.

What are the disadvantages of a large down payment on a car?

Going all-in with a large down payment on your ride might seem like a superstar move, but it could leave your savings tank on E. Less cash for other expenses or emergencies isn’t ideal, and that money might have flexed its muscles better elsewhere, like in an investment.

Do millionaires pay off debt or invest?

Millionaires managing their moolah often face the pay-off-debt or invest showdown. These savvy folks usually compare interest rates: if the debt costs more than investments earn, they might zap the debt first; if not, they let their greenbacks grow.

Is it smart to pay off car loan early?

So you’re noodling over paying off your car loan sooner? It could be a slam-dunk for peace of mind and saving on interest. But keep an eye out for prepayment penalties and think about whether that cash could be a slam dunk elsewhere.

How long is too long for a car loan?

How long is too long for a car loan? Picture a road trip that lasts over five years and your ride could be worth less than the IOU. Stick to something short and sweet – typically, 60 months or less – to keep your finances in the fast lane.

Is it better to pay extra on principal monthly or yearly?

Paying extra on your principal monthly vs. yearly? It’s like choosing between taking stairs or elevator for a workout – regular and consistent can give you a subtle leg-up, chipping away at that interest bit by bit each month.

How much extra should I pay on my car?

How much extra moolah should you throw at your car loan? Gauge your budget, partner! Any extra is a high-five to your future self, but don’t leave your wallet gasping for air. Even a little boost can turbocharge your loan’s countdown.

Does paying extra on loan help credit?

Paying extra on your loan is like giving your credit score a healthy smoothie. It shows you’re responsible with debt, which could sweeten up your credit. Just don’t get so gung-ho you forget to keep some cash for a rainy day.

Is there a best time within the month to make an extra payment to principal?

Is there a prime time within the month to chuck some dollars at the principal? Sure! Right after your regular payment hits. It’s like adding an extra push to your swing – straight toward lowering that interest. Timing is everything!