Understanding how to calculate debt ratio is an absolutely essential part of your financial toolkit. Whether you’re sizing up a new home on the sun-kissed hills of California or considering dabbling in the stock market, this potent number can be the compass that guides you through the tempest of financial decisions. Gird your loins, folks! We’re about to embark on a journey of shocking debt ratio mastery.

Step 1: Understanding What Good Debt and Debt Ratio Mean

Alright, warriors of fiscal responsibility, let’s cut through the financial jargon like a hot knife through butter and get down to brass tacks.

Desk Calculator Large Digit Display, Battery Dual Power Basic Calculator Desktop, Big Button for Office, Business, Home and School (Grey).

$8.99

The Desk Calculator with a Large Digit Display is an essential tool, meticulously designed to meet the demands of a fast-paced office, bustling business environments, as well as the academic needs at home and school. It features a prominent display, ensuring that each digit is clearly visible, which reduces the likelihood of errors when dealing with complex calculations. The calculator is finished in a professional grey, seamlessly integrating into any office decor. Moreover, its angled screen facilitates easy reading from various positions, making it accessible for a collaborative work setting.

Built for intuitive use, this Basic Desktop Calculator boasts large, well-spaced buttons which minimize the chances of hitting the wrong key, speeding up data entry with a tactile feel that provides physical feedback with each press. The dual power design ensures reliability, operating primarily on battery power with a solar panel as a secondary source, maintaining performance in well-lit spaces and preserving battery life. Durability combines with functionality, as this robust calculator endures the wear and tear of daily use while being light enough for easy transport between workspaces. Users from accountants to students will appreciate its straightforward interface, which makes it a breeze to perform a wide array of arithmetic operations.

The Desk Calculator is distinctly crafted to serve various computing tasks in the realms of business calculations, financial work, school projects, and everyday home budgeting. Its energy-efficient operation guarantees that it’s always ready when needed, offering peace of mind and reducing maintenance. For those who prefer to maintain a tidy workspace, the streamlined design minimizes clutter and provides a neat footprint on any desk. With this reliable grey calculator, crunching numbers becomes a more organized and less strenuous process, allowing users to focus more on the results and less on the process of calculation.

Exploring the Meaning of Good Debt

Ever heard the phrase “it takes money to make money?” Well, that’s the essence of what is good debt. Take, for example, a mortgage. You’re probably thinking, “Isn’t a mortgage a ball and chain?” Here’s the scoop: a mortgage can be considered ‘good debt.’ You’re putting your cash into an asset—a piece of the Earth, if you will—that can appreciate faster than your aunt’s antique vase collection.

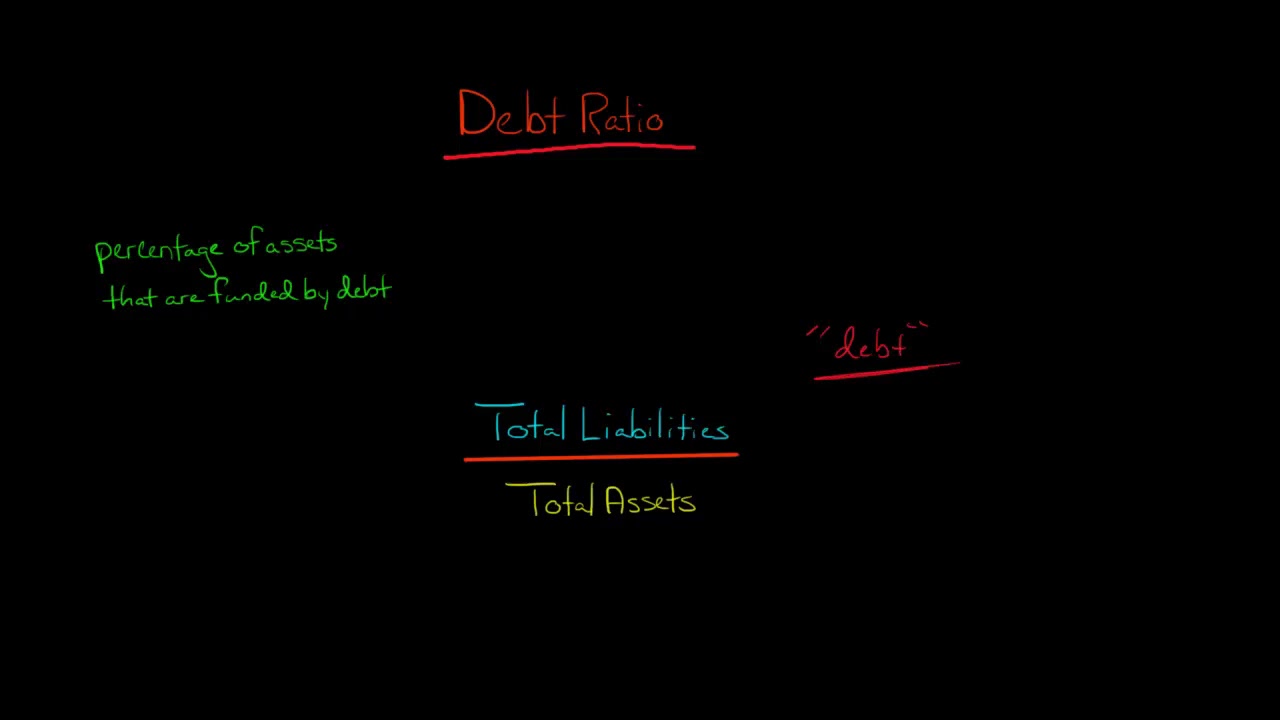

Defining Debt Ratio and Its Importance

Here’s a riddle for you: What do investors and lenders eyeball more than the latest Emilia Clark nude scene in a hot TV show? The debt ratio, of course. It’s a straightforward yet mighty figure, defined as Total Debt / Total Assets. So if your debt-to-glory ratio is higher than a kite, you’ve got some financial pruning to do. Keeping this number well-manicured indicates to potential lenders that you’re as reliable as a Swiss watch.

Step 2: Dive Into the Debt Ratio Formula

Roll up your sleeves; we’re going deep into the debt ratio formula, leaving no stone unturned.

Breaking Down the Components of the Formula

To calculate your debt ratio, grab your calculator and divide your total debt by total assets. Got $150,000 in liabilities and $600,000 in total assets? Boom! Your debt ratio is 0.25, or 25%. That’s lower than a snake’s belly, my friend—a stellar position to be in.

Real-World Applications of the Debt Ratio

Let’s switch gears for a sec and look at big fish like Tesla. Sure, Elon’s baby isn’t just cool electric cars; it’s also about mastering their financials. A company’s debt ratio can be calculated by total debt divided by total assets. Over 100%? They’re in hot water. Below it? They’re sailing smoother than a gravy boat.

Calculated Industries ConversionCalc Plus Ultimate Professional Conversion Calculator Tool for Health Care Workers, Scientists, Pharmacists, Nutritionists, Lab Techs, Engineers and Importers

$36.77

The Calculated Industries ConversionCalc Plus is a versatile and comprehensive professional conversion calculator, specifically designed to meet the varied needs of health care workers, scientists, pharmacists, nutritionists, lab technicians, engineers, and importers. With an extensive list of built-in functions, it effortlessly converts between metric and standard units, ensuring accurate and reliable data for critical calculations and reducing the risk of conversion errors. Its user-friendly interface makes navigating through conversions quick and intuitive, which is essential for professionals who require immediate results in fast-paced environments.

This ultimate conversion tool features specialized functions for a variety of sectors, including dose-to-weight conversions for healthcare professionals, ingredient weight to volume conversions for nutritionists, and complex unit calculations for engineers and scientists. It is equipped with an easy-to-read, backlit LCD display, so results are clear even in low-light conditions, as well as a durable, ergonomic design that stands up to the demands of daily use. The ConversionCalc Plus saves precious time by eliminating the need for manual conversion tables and the potential errors that can come with them.

Not only is the ConversionCalc Plus a practical tool for the workplace, but it also serves as an educational asset for students and trainees in relevant fields. It includes a quick reference guide and an intuitive keyboard layout that assists users in learning the logic behind unit conversions while improving their efficiency. Whether it’s used for preparing medications, conducting nutritional assessments, processing laboratory data, designing engineering projects, or managing import logistics, the ConversionCalc Plus is the ideal all-in-one calculator that blends accuracy, functionality, and ease of use.

| Step Description | Calculation Formula | Example Figures | Result | Interpretation |

| 1. Determine Total Assets | Sum of all the assets owned | $600,000 (Total Assets) | — | — |

| 2. Determine Total Liabilities | Sum of all short-term and long-term debts | $150,000 (Total Liabilities) | — | — |

| 3. Calculate Debt Ratio | Total Liabilities ÷ Total Assets | $150,000 ÷ $600,000 | 0.25 or 25% | Indicates a healthy balance between debts and assets. |

| 4. Evaluate Based on Thresholds | Compare result with known thresholds (30%, 40%, 100%) | 25% Debt Ratio | — | Excellent (<30%). Acceptable risk for lenders. |

| 5. Calculate Total Debt | Sum of all long-term and short-term debts | — | — | Total Debt is required for determining the absolute debt amount. |

| 6. Calculate Debt to Net Worth Ratio | Total Liabilities ÷ Net Worth | — | — | Useful for understanding financial leverage and solvency. |

| 7. Interpretation of Debt Ratio | Debt Ratio < 1.0 (or 100%) or > 1.0 (or 100%) | — | — | <100%: More assets than debt. >100%: More debt than assets. |

| 8. Lenders’ Consideration of Debt Ratio | Compare individual’s or company’s ratio with lenders’ standards | — | — | Below 30% is excellent; above 40% is critical for individuals. |

Step 3: Managing Your Debt to Credit Ratio

Alright, it’s time to talk about another member of the debt ratio family: the debt to credit ratio. It’s the black sheep perhaps, but it’s got its own appeal.

What Is Debt to Credit Ratio and Why It Matters

This little gem measures your available credit against how much you’ve used and, darling, it makes or breaks your credit score. Too high and your financial reputation could go down like a lead balloon!

Strategies to Improve Your Debt to Credit Ratio

One under-the-radar move is playing musical chairs with your balances using balance transfer credit cards. Just don’t get left standing when the music stops. By consolidating your debt, you could be paying less in interest than the night court cast makes in residuals!

Step 4: Calculating Your Total Debt Ratio Like a Pro

Now, let’s put our learning hats on and dive into the nitty-gritty of your own total debt ratio.

Steps to Accurately Calculate Your Own Total Debt Ratio

Picture this: You’re knee-deep in festive shopping madness. You’ve got some short-term debts (credit card) and some long-term debts (that pesky student loan). Collect the balances, add them together, and compare it to your total assets. That’s your total debt ratio.

Comparing Your Total Debt Ratio to Industry Standards

Your personal debt ratio should be lower than a limbo stick at a beach party. Aim for below 30%, and you’re golden. If you’re hitting 40%, sound the alarms—creditors may leave you faster than a teenage boy at a family gathering.

Step 5: Mastering Your Debt Ratio for Long-Term Success

We’ve reached the summit, financial trailblazers. It’s time to plant your flag and take command of that debt ratio for enduring prosperity.

Consolidating and Refinancing: Tools for Better Debt Management

Considering home buying in California? Debt consolidation and refinancing options from fintech goliaths like SoFi or veterans like Rocket Mortgage can morph your debt ratio faster than Maddox Jolie-pitt grows up!

Regular Monitoring and Adjustment: The Key to Debt Ratio Mastery

You wouldn’t go on a road trip without a map, right? Think of apps like Mint or YNAB as your financial GPS. They help track your debts as deftly as Indiana Jones on the hunt for lost treasure—ensuring you keep your numbers shipshape and Bristol fashion.

CATIGA Desktop Calculator Digit with Large LCD Display and Sensitive Button, Solar and Battery Dual Power, Standard Function for Office, Home, School, CD (Blue)

$8.99

The CATIGA Desktop Calculator is a user-friendly and practical tool designed for accuracy and efficiency in everyday calculations in the office, home, or school settings. It features a large, easy-to-read LCD display that ensures the user can clearly see their digits and computations at a glance. The sensitive, responsive buttons are engineered for quick entry, minimizing the likelihood of errors during fast-paced number crunching. This reliable calculator boasts a standard set of functions, including addition, subtraction, multiplication, division, and various auxiliary operations to meet the daily mathematical demands.

Built with convenience in mind, the CATIGA calculator operates via dual power sources, using solar energy with a robust battery backup to ensure continuous operation even in low light environments. The eco-friendly solar panel efficiently powers the calculator under natural or artificial light, while the battery serves as a reliable alternative, ensuring constant readiness for any calculation task. This CD (Blue) edition of the calculator not only serves its purpose effectively but also adds a vibrant splash of color to the workspace, distinguishing itself from the more traditional office tools.

Designed to be both durable and portable, the CATIGA Desktop Calculator is perfect for professionals, students, and anyone in need of a dependable calculating companion. Its compact design ensures that it doesn’t occupy too much space on a desk, while its sturdy construction is intended to withstand the rigors of daily use. The intuitive layout of the keypad and functions makes this calculator accessible to users of any age or expertise level. Whether balancing a budget at home, solving complex equations in a classroom, or managing finances in an office, the CATIGA Desktop Calculator stands as a versatile and essential accessory for a multitude of math-related tasks.

Conclusion

Embracing Financial Mastery through Effective Debt Ratios

Folks, we’ve trawled through the world of debt ratios like a pro. From understanding in finance to practically applying ratios to your life—if you weren’t a believer in the power of financial literacy before, I bet your socks you are now!

Remember, knowledge is a renewable resource. Use our mortgage refinance calculator and Debt-to-income ratio calculator to stay ahead of the game. Just as I live for financial success stories, I want you to thrive in the vast ocean of economic opportunity.

So let’s raise our glasses to a future where you’re not just keeping your head above water but surfing the waves of financial prudence and success. It’s not merely about managing debt, but mastering it. Get ready to make some waves, money mavens!

How to Calculate Debt Ratio: Unlock the Mystery!

Hey there, savvy reader! Struggling to work out your debt ratio and why it matters as much as a solid workout plan? Well, buckle up because we’re going on a little number-crunching journey that’ll beef up your financial fitness faster than an Athlean X session!

Step 1: Gather Your Debt Intel

Just like stepping on a scale, you’ve gotta face the music (or numbers in this case) honestly. Tally up all that you owe – from those pesky credit card bills, student loans, car payments, to your mortgage. Don’t shy away; getting a clear image is key!

Step 2: Income Insights

Now, let’s talk about what’s coming into your bank account. Total up your monthly take-home pay. Remember, like the buildup to a killer punchline, this is the moment of truth where your debts and income duke it out.

Step 3: The Debts-to-Income Showdown

Alright, get ready to rumble! Divide your total monthly debt by your total monthly income. This might feel like you’re trying to understand the contemporary meaning of an abstract painting – but fear not! Simply put, if your debts are the paint, and your income is the canvas, that percentage you get is the overall picture of your financial masterpiece.

Step 4: Percentage Play

Grab that calculator and multiply your result by 100 to get a percentage. Bam! That’s your debt ratio staring right back at you. If it’s high, don’t sweat it. This is just the warm-up. With the right plan, you can get leaner.

Step 5: Rinse and Repeat for Mastery

Rome wasn’t built in a day, and neither is debt ratio mastery! Keep checking in on this number like you would your heart rate during a cardio blast. Staying on top of it is the secret sauce to getting financially swole.

So there you have it, the lowdown on how to calculate debt ratio without the snooze fest. Keep it handy because it’s one number that can truly pack a punch when you’re looking to flex your financial might. Stay calculated, folks!

What is an example of a debt ratio?

An example of a debt ratio? Well, imagine you’re juggling your finances — picture your total monthly debt payments are $2,000 and your monthly income is $6,000. In this case, divide $2,000 by $6,000 and voila! Your debt ratio is about 33%.

What is a good debt ratio percentage?

What’s a good debt ratio percentage? It’s like finding the sweet spot in baking — you don’t want too much or too little. Generally, a debt ratio of 35% or less is pretty peachy; it shows lenders you’re not biting off more than you can chew.

How do you calculate debt?

How do you calculate debt? To get the lowdown on your debt, just add up all the money you owe – from credit cards to loans, the whole shebang. It’s akin to tallying your bar tab before last call — you need to know what you’re working with!

What is the formula for debt to worth ratio?

The formula for debt to worth ratio sounds complicated, but it’s easy as pie. Take your total liabilities and divide them by your net worth. If it feels like trying to measure your love for pizza, remember, it’s all about keeping those liabilities in check.

Is a debt ratio of 75% good?

Is a debt ratio of 75% good? Uh-oh, that’s getting into hot water territory. This means you’re leaning heavy on borrowed money — like being up to your ears in water on a sinking boat. It’s a red flag to creditors that you might struggle with new debt.

Is a debt ratio of 70% good?

Is a debt ratio of 70% good? It’s a bit like playing with fire, honestly. A 70% debt ratio suggests that you’ve got quite a bit on your financial plate, so lenders might view you as a riskier bet than someone with a lower ratio.

What is the formula for bad debt ratio?

What is the formula for bad debt ratio? It’s not something to write home about — bad debt ratio compares doubtful debts to the total receivables. Simply put, this ratio tells you what slice of your receivables might just go poof into thin air.

What is too high for debt ratio?

What is too high for debt ratio? Well, if you’re pushing past 40%, you’re entering the “better watch out” zone. It’s like your diet is becoming more midnight snacks than greens — a sign that things might not be so healthy with your finances.

How do you explain debt ratio?

How do you explain debt ratio? Picture it as your financial report card — it tells you (and potential lenders) how much of your monthly income is already promised to past debts. Lower ratios mean more gold stars for you in the eyes of creditors.

How to calculate ratios?

How to calculate ratios? It’s a bit like making your favorite cocktail — it’s all about the right mix. Take two related numbers, divide the first by the second, and you’ll have the ratio that tells you the strength or balance of your financial situation.

How to calculate debt-to-equity ratio calculator?

How to calculate debt-to-equity ratio calculator? First off, snag your total debts and equity. Now, punch those numbers into a calculator faster than a kid with a new video game, divide debt by equity, and boom – there’s your debt-to-equity ratio!

What are common debt ratios?

What are common debt ratios? It’s like a toolbox for your finances – you’ve got your debt-to-equity ratio, your debt-to-income ratio, and your debt service coverage ratio, each helping you suss out a different facet of your financial health.

What is the most common debt ratio?

What is the most common debt ratio? Hands down, it’s the debt-to-income ratio. It’s as popular as a hit song at a summer concert, showing lenders whether your wallet’s stuffed enough to handle your debts without breaking a sweat.

How do you explain debt ratio?

How do you explain debt ratio? Again? Alrighty, think of it as your financial fitness tracker: It measures the chunk of your income that goes towards debt and whether you’re in shape to borrow more or if you’re financially winded.

What are the commonly used debt ratios?

What are the commonly used debt ratios? There are a handful that top the charts: Your debt-to-income ratio is like the lead singer, with debt-to-equity and debt service coverage ratios as the bandmates, all rocking out to keep your financial status in tune.