Buying a home is a significant financial commitment; as such, it’s vital to dot the i’s and cross the t’s before making the leap. A critical part of this process is understanding the workings of the Home Mortgage Calculator California. Much like a trusty roadmap, this tool provides insightful details that drive you safely through the terrain of property ownership. But before we get behind the wheel, let’s familiarize ourselves with this indispensable navigator of mortgage territory.

Comprehending the Functionality of a Home Mortgage Calculator California

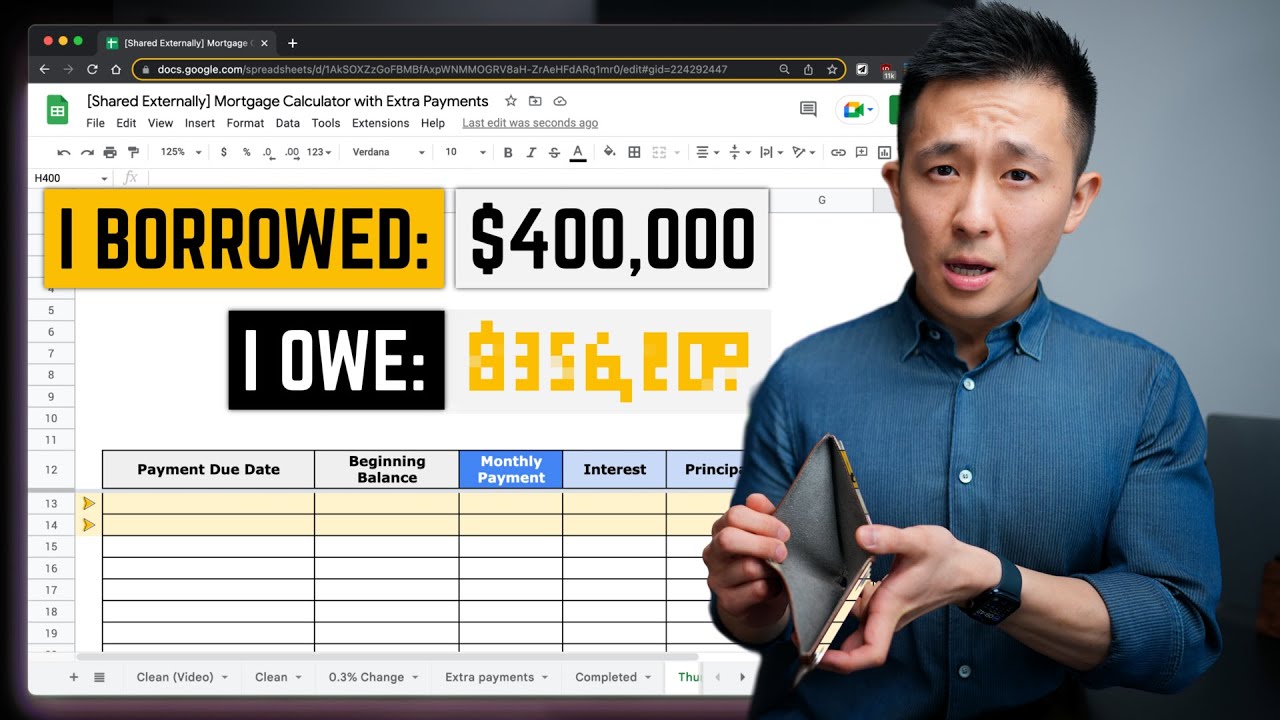

So, you’ve made up your mind to purchase that cozy abode you’ve been eyeing in sunny California. The next thing is to figure out your monthly mortgage payments. This is where a home mortgage calculator becomes indispensable. Its primary job is to estimate your monthly mortgage payments, so you can determine the best financial fit for your budget.

Using the home mortgage calculator, you’d get a breakdown of your payment structure, including the principal amount, interest, taxes, and possibly, home insurance. By fine-tuning these values, you can get a real sense of what your upcoming financial commitments would look like. Moreover, these calculators also account for any additional payments or penalty provisions. In essence, they offer a granular, detailed look at the possible mortgage landscape a home buyer in California would encounter.

Delve into the Mechanics of a CA Home Loan Calculator

Alright, let’s roll up our sleeves and get into the nuts and bolts of a CA home loan calculator. The primary variables the calculator considers are the property’s price, the down payment, loan term, and interest rate. But hey, don’t get spooked by these terms. We’re all friends here, and we’re on this journey together.

In simple terms, the calculator considers how much you’re borrowing (the price minus the down payment), the loan duration (how long you’ll spread out your payments), and the interest rate (the cost of borrowing). Plus, it takes into account property tax, home insurance, and if applicable, Private Mortgage Insurance (PMI). By tweaking these variables, you’re able to see different payment scenarios and figure out the best structure that suits you. All this without breaking a sweat. Ain’t that handy?

| Subject | Details |

|---|---|

| Mortgage Amount | $300,000 |

| APR for 15-Year Loan | 6% |

| Monthly Payment for 15-Year Loan | $2,531.57 (excluding escrow) |

| APR for 30-Year Loan | 6% |

| Monthly Payment for 30-Year Loan | $1,798.65 (excluding escrow) |

| Minimum Salary Required for $300K House | $50,000-$74,500/year |

| House Affordability for $70K/year Income | Between $290,000 and $360,000 |

| Monthly House Payment for $70K/year Income | $2,000-$2,500 |

| Monthly Payment for 30-year Loan with 7.2% Interest Rate | $3,255.79 (interest and principal only, no taxes, fees or insurances included) |

| Escrow | Varies depending on home location, insurer, and other details |

| Date | As of October 9, 2024 |

Learn to Calculate Mortgage Payment California

Alright, strap up — we’re going for a step-by-step ride on how to calculate mortgage payment in California. First off, you need your home price, down payment amount, loan term, and interest rate. Punch these values into your calculator and voila! Out comes your mortgage estimate.

But it’s not enough to understand the “what”; you also have to know the “why”. So, let’s break down this monthly mortgage payment. One, you’ve got the principal — the original loan amount you’re steadily repaying. Two, there’s interest — the cost of borrowing. Then, there’s property tax and home insurance — necessary costs to protect your beautiful home. These four elements form what is known as PITI (Principal, Interest, Taxes, Insurance). And yes, your helpful home mortgage calculator factors all these into its calculations.

Streamlining Your Process with a California Home Loan Calculator

Now, why should you use a California home loan calculator? Well, for one, it saves time. You pop in your values and you’re presented with a quick, comprehensive mortgage estimate. This gives you a sense of control, allowing you to tweak your numbers until it dovetails nicely with your financial situation.

Secondly, it’s your financial truth serum. It dispenses with potentially harmful pretenses and presents things just as they are. A stark reminder that you can’t wish your way through mortgages – the numbers have to add up. Albeit gently, it keeps you grounded in reality. A reality echoed in precise, tell-all numbers.

California Mortgage Plus: Enhance Your Home Buying Journey

Just when you thought it couldn’t get better, enter California Mortgage Plus. This gem ups the ante, adding in advanced parameters like PMI and HOA fees. The result: an even more comprehensive mortgage picture that eliminates downright surprises.

What sets California Mortgage Plus apart from other calculators is its detailed analysis. It’s like that meticulous friend who ensures every detail is sorted before a road trip. As such, you get a reliable, no-stone-unturned estimate that keeps you in full control.

Opportunity for First-time Home Buyers with FHA Calculator California

If you’re a first-time home buyer in California, the world of mortgages can seem daunting, but don’t fret! The Federal Housing Administration (FHA) has got your back. With a lower down payment and more forgiving credit score requirements, FHA loans are a fantastic option for those getting their first taste of property ownership.

To aid in this process, you have the FHA mortgage calculator California. It considers all the features of an FHA loan, giving you an accurate estimate of the monthly payments. So, with this tool, you can navigate through the initial property acquisition process with more confidence.

Simplifying Home-loan with Free Mortgage Calculator California

Listen up, folks! Here’s the sweet part – most of these calculators are completely free! Yes, they cost zilch. Free mortgage calculators offer a host of functionalities and give high-quality results at no cost. No hidden fees, no subscription. Just good ‘ol helpful calculators at your service.

A free mortgage calculator California can do everything a paid version does, allowing you to run multiple scenarios, for a detailed envision of your mortgage payments. So why pay when you can get an efficient and reliable home loan calculator for free?

Differences among Mortgage Calculators: Comparing CT, NJ, and SC

Now, you may wonder, “I’ve got the hang of the CA home loan calculator, isn’t that all I need?” Well, sort of. If you only plan on buying in California, then boom, you’re set! If you’re considering other states, though, you’ll want to consult with their calculators as well. Mortgage calculator CT, mortgage calculator NJ, or mortgage calculator SC – each tool considers state-specific costs and regulations.

Say, for instance, you fancy a place in Connecticut, New Jersey, or South Carolina. In that case, you’d need a complementary “navigator”. Some variables like property tax rates and insurance costs could differ significantly, necessitating an appropriate tool. Don’t worry, though, the principle remains the same. You’ll just be tweaking those variables till they match your financial situation in your state of choice.

Figuring out Your Monthly Commitments with Monthly Mortgage Calculator California

Probably the most crucial number to consider while planning for a home purchase is your monthly commitment. That’s the amount that you’ll commit to paying every single month until your mortgage is paid off.

Using a mortgage payment calculator California will give you a clear breakdown of your monthly costs, allowing you to plan your budget accordingly. This tool is designed to help you understand just how much house you can comfortably afford, considering your current financial situation.

Estimating Ongoing Costs with Refinance Mortgage Calculator California

Down the line, you might consider refinancing your home. This scenario could become a reality if interest rates go down or your financial standing improves. The goal here is to save money, reduce the term of your loan, or both. A refinance mortgage calculator California can be an effective tool to navigate this situation.

But why should you consider refinancing? Well, sometimes life smiles at you, and you find yourself with a lower interest rate or improved credit score than when you first took the loan. This calculator helps hone in on whether refinancing would indeed be beneficial for you.

Deep Dive into the Operation of PITI Calculator California

Remember PITI? That’s right, the Principal, Interest, Taxes, and Insurance. Seemingly innocuous, these four constituents have a considerable say in your mortgage payment calculations. Understanding them is vital, as it engenders a well-informed decision-making process.

A PITI calculator California cleverly integrates these elements into its calculations. This holistic approach not only provides a complete mortgage picture but it also sheds light on the affordability of the property. With this, you’re adequately equipped to sort out your financial commitments before heading into homeownership.

Final Thoughts: The Backbone of Your Home Buying Process

The journey towards property ownership might be riddled with complexities and uncertainties, but you do not have to travel alone. With the help of these calculators, you can map your road to homeownership with finesse. More than just tools, these calculators represent true financial companions seamlessly guiding you through the mortgage landscape.

So, whether it’s the FHA mortgage calculator, the PITI calculator, or good old home mortgage calculator California, make these your allies. They won’t abscond in rough times neither will they gloss over the truth. With the wealth of insight these invaluable assistants provide, you’ll have the keys to your dream home before you know it.

And remember, as Kyle Baugher puts it, “a home is a long-term commitment, much like a marriage. You must be prepared to maintain a healthy relationship with it. That means understanding mortgages, the home-buying process, and most importantly, your own financial situation. So, my advice? Use these calculators. Be informed. Your future self will thank you.”

With that, dear future homeowner, it’s a wrap. May your property dreams find firm footing in the sunny climes of California! Before you know it, you’ll be kicking back in your new pad, on a warm evening, perfectly content in the knowledge that you’ve made an informed, sound financial decision.

Now, what are you waiting for? Roll up your sleeves, crunch some numbers with these calculators, and learn a thing or two about what your future may look like. Trust me, by doing so, you are already on your way to secure property ownership. You are, after all, the captain of your ship, and your destination is right in front of you – you just need to understand and navigate the waves to reach it. And remember, the journey is supposed to be fun, not daunting. Good luck!

How much does a $300 000 mortgage cost per month?

Adjusting for a standard 30-year fixed rate at 4%, a $300,000 mortgage can set you back around $1,432 per month. Of course, this doesn’t take into account property taxes, insurance, and the like, so your actual bill might be a bit steeper.

How much do I need to make to qualify for a $300 000 mortgage?

To snag a $300,000 mortgage, you’d need to pull in roughly $67,000 a year, given that most lenders want your monthly housing costs to take up no more than 28% of your monthly income. That’s not hard and fast, though, so don’t start sweating bullets just yet.

How much house can I afford if I make $70,000 a year?

If you’re raking in $70,000 a year, you could potentially afford a house priced up to $350,000, assuming a 20% down payment and other expenses align with industry norms. Then again, remember the old saying “just because you can, doesn’t mean you should.”

What income do you need for a $800000 mortgage?

Bagging an $800,000 mortgage would require a hefty annual income of around $178,000, according to the average lender guidelines. That’s one pretty penny, eh?

What income do you need for a 400k mortgage?

To qualify for a $400,000 mortgage, you’re looking at needing an income somewhere in the ballpark of $89,000 a year. Again, this could fluctuate based on other existing debts and expenses.

What credit score is needed to buy a $300 K house?

To purchase a home in the $300k range, most lenders typically look for a credit score of 680 or higher. Remember, a better score can snag you a better interest rate, saving you heaps in the long run.

How much house can I afford if I make $36,000 a year?

If you’re bringing in $36,000 annually, you could comfortably swing a house in the $150,000-range, assuming your debt is manageable and you’ve got some savings. Remember, you don’t want to bite off more than you can chew.

Can I buy a house with 40k salary?

With a yearly salary of $40,000, buying a house isn’t out of the realm of possibility. Budgeting wisely and managing expenses can potentially get you a home in the $200,000 price range.

Can I afford a 300k house on a 60k salary?

Affording a $300k house with a $60k salary sounds daunting, but it’s certainly possible if you’ve got a handle on your debts and have managed to save for a sizeable down payment. It’s all about budgets, my friend.

Can I buy a million dollar home with a 70k salary?

A million-dollar home on a 70k salary? Gosh, that’d be a tough nut to crack. It’s safe to say you’ll need a significantly higher income for most lenders to even consider it.

What is the 28 36 rule?

The 28/36 rule is a common rule of thumb in the mortgage world. The “28” comes from the guideline that your maximum household expenses should not exceed 28% of your gross monthly income, while the “36” represents the maximum percentage of income that should go to total monthly debt.

Who can afford to buy a house in California?

Who can afford to buy a house in California? Well, truth be told, with average house prices sitting pretty at around $600,000, you’d need a salary of roughly $120,000 annually. But hey, don’t let that burst your bubble, there are options for all income levels.

What income do you need for a $750000 mortgage?

For a $750,000 mortgage, you’d need a hefty income of around $167,000 according to standard benchmarks. That’s chunky change right there!

What income do you need for a $1000000 mortgage?

Wanting a cool $1,000,000 mortgage? Now we’re talking big numbers! You’re likely looking at needing an annual income of at least $222,000. Woof!

How much income to afford $1 million dollar house?

To be in the mix for a $1 million dollar house, you ought to be bringing in around $222,000 a year, taking into consideration standard lending practices and a reasonable cushion for savings, taxes, and upkeep. Quite the pretty penny, isn’t it?