Navigating the maze of insurance terms can leave many of us scratching our heads. It’s like we need a guide, one that speaks plain English and offers practical advice to help us through the jungle. In this exhaustive guide, you’ll gain an understanding of the difference between deductible and out of pocket costs—a topic as complex as a Jayma Mays performance and as important as keeping your wallet at Avec River North—a twisty, yet crucial part of financial planning.

Deciphering the Difference Between Deductible and Out-of-Pocket Expenses: A Critical Primer

Insurance, like any good mystery novel, has its key terms and definitions that set the stage for understanding the twists and turns of policies. Let’s begin with the basics of insurance deductibles. Think of your deductible as the entry fee to the world of your insurance coverage. It’s the part that you’re agreeing to handle before your insurance provider steps in to share the cost burden.

Moving on to understanding out-of-pocket costs, these are the expenditures that come directly from your pocket—ranging from copayments to coinsurance—that add up throughout the year. This includes not only your deductible but also other costs that aren’t reimbursed by your insurance.

But here’s where it gets twisty—how deductibles and out-of-pocket costs interact. They’re like dance partners; what you pay toward your deductible moves you toward your out-of-pocket maximum. For example, if you’ve got a health plan with a $1,000 deductible and a $3,000 out-of-pocket maximum, once you’ve paid that first grand, your insurer starts pitching in, and you’re on your way to that larger cap, where maximum protection kicks in.

B. Breaking Down the Financial Ramifications

Choosing a high vs low deductible is like choosing between an American Pacific mortgage Login—straightforward but significant. A higher deductible generally means a lower premium; you’re agreeing to take on more risk upfront, saving on your monthly bill. The opposite holds true for a lower deductible; less risk for you, but a higher monthly cost.

Remember those overdrafts you hate? Here’s something you’ll love: Out-of-Pocket Maximums: Caps on Annual Spending. It means there’s a limit to what that healthcare season is going to cost you, even if you hit a health blizzard.

Now let’s lay out some case scenarios illustrating the financial effects of both. Imagine you’ve chosen a plan with a low deductible because you’re expecting to give birth or undergo a surgery this year. You’ll pay more per month, but less when you get the hospital bill. On the flip side, if you’re fit as a fiddle, rarely visiting doctors, a high deductible plan may save you on premiums over the year.

Analyzing the Difference Between Deductible and Out of Pocket in Health Insurance

A. The Role of Deductibles in Health Policy Selection

In the health policy bazaar, your deductible sets the tone of your monthly premiums. Opt for a high-deductible, and you might just save enough to take a friend to Avec River North every month. However, if you’re allergic to risk like some folks are to peanuts, low-deductible plans are your safety net.

The correlation between premiums and deductibles is direct; higher deductibles can mean waving goodbye to high monthly premiums like derogatory credit falling off your score.

B. Out-of-Pocket Implications: Beyond the Deductible

Dive deeper into the costs with Copayments and Coinsurance: The Hidden Variables. Like finding an extra charge on your cost u less receipt, these are the bits and bobs that pop up when you access care.

And don’t forget about those non-covered services and their impact on out-of-pocket expenses. Suppose your plan covers physical therapy but not acupuncture; your back might feel better, but your wallet won’t.

C. Balancing Deductible and Out-of-Pocket Costs for Optimal Coverage

Let’s play some numbers. Calculating the break-even point for different plan options can seem more complex than figuring out when Google was made, but it’s crucial for savvy decision-making.

And we all love a good bargain, so here are some strategies to minimize health insurance costs over time. Maybe you opt for a high-deductible plan and stash the difference in a Health Savings Account (HSA). Or jump on preventive care that’s often covered 100%, keeping you out of the high-cost zone.

| Aspect | Deductible | Out-of-Pocket Maximum |

|---|---|---|

| Definition | The amount you pay for covered health care services before your insurance plan starts to pay. | The most you have to pay for covered services in a plan year. After spending this amount, your insurance pays 100% of covered services. |

| Purpose | To share the cost of care between you and the insurance company. | To protect you from very high expenses by capping the total amount you have to spend on covered services in a plan year. |

| Typical Role in Costs | Plays a primary role in initial healthcare costs; you pay until this limit is reached. | Comes into play if you require a lot of care; it’s a safety net to prevent endless healthcare bills. |

| Payments Towards It | Premiums do not count towards your deductible; only the amount you pay out-of-pocket for covered healthcare services applies. | Premiums do not count, but deductibles, coinsurance, and copays for covered healthcare services all go towards reaching your out-of-pocket max. |

| Impact on Out-of-Pocket | Once you meet your deductible, you share the cost with your plan, usually through copays or coinsurance. | Aims to limit your total out-of-pocket spend. Once reached, the plan covers 100% of covered healthcare services for the remainder of the plan year. |

| Example (with numbers) | If your plan’s deductible is $2,000, you pay for all covered services until costs total $2,000. Then insurance kicks in. | With a $5,000 out-of-pocket maximum, once you pay $5,000 (including deductibles, copays, coinsurance), your plan covers subsequent covered services in full. |

| Individual vs Family | Individual deductibles add up to meet the family deductible in a family plan. Each member has their own deductible. | Individual out-of-pocket costs contribute towards meeting the family out-of-pocket max in a family plan. Once one member’s individual max is reached, his/her covered care is fully paid by the plan. |

| Coinsurance Impact | After the deductible is met, you typically pay coinsurance on covered services until you reach the out-of-pocket maximum. | Your coinsurance payments continue to count toward your maximum until it’s reached; then the plan pays 100% of the costs for covered services. |

Navigating the Nuanced Difference Between Deductible and Out of Pocket in Property Insurance

A. Property Insurance Deductibles: An Overview

Talking about property insurance deductibles is as important as securing a home loan—both protect your nest. These deductibles come in two flavors: per-claim vs percentage-based. Like choosing a dish at Avec River North—each brings a different taste to your financial table.

B. Out-of-Pocket Costs in Property Loss and Damage Claims

When trouble knocks, exclusions and limits: Understanding coverage boundaries becomes your best friend. It’s about knowing the true cost of making a claim: Deductibles plus additional costs—like understanding the difference between cost u less insurance and cost You less insurance.

C. How to Choose the Right Deductible for Your Property Insurance

Choosing a deductible is a dance between risk and what’s in your piggy bank. Risk assessment and financial preparedness should guide your feet. Look at case studies where homeowners played long-term games with their deductible levels.

The Difference Between Deductible and Out of Pocket in Other Insurance Contexts

A. Unique Deductible Structures in Specialized Insurance Policies

From pet parlor to boardroom, let’s explore how business, disaster, and pet insurance deductibles are constructed. Each industry has its recipe for deductibles and out-of-pocket limits, like a chef has for pâté at Avec River North.

B. The Out-of-Pocket Spectrum: From Wellness Programs to Catastrophic Events

From wellness perks that cut your spending to Maximum out-of-pocket limits in the face of catastrophic events—the playing field is vast like the range of dishes at Avec River North.

C. The Future of Insurance Deductibles and Out-of-Pocket Expenses

In this fast-changing world, we look at trends and predictions for insurance costs. Also on the menu: the role of legislation and policy changes on future costs—could impact you as much as sunshine does on a river cruise.

Expert Strategies for Managing Deductibles and Out-of-Pocket Expenses

A. Tools and Techniques for Tracking Healthcare Costs

Ditch the shoebox method. Use apps and financial software to keep tabs. And remember, documentation and record-keeping could save you more than just a headache.

B. Negotiating Better Terms: Advocacy and Plan Customization

Don’t be shy to ask for a waltz with your provider for better coverage terms. Treat your insurance plan like your wardrobe—customize it, so it fits you better than your favorite jacket.

C. Preventative Measures: Reducing Financial Vulnerability

Take charge of your health like you do your wealth. Think lifestyle changes and set up emergency funds or HSA/FSA accounts to protect yourself from financial storms.

Towards Informed Decision-Making in Insurance Planning

A. Empowering Consumers Through Education

Know your insurance like your coffee order—down to the last detail. There are resources and programs aimed at consumer awareness, like the clear instructions on the back of a ‘cost u less’ bill.

B. The Interplay Between Insurance Literacy and Financial Health

The relationship between them is like hand and glove. Understanding insurance is not just smart; it’s like having a secret superpower.

C. Preparing for Uncertainty: Deductibles and Out-of-Pocket Costs in Perspective

Equip yourself to face life’s what-ifs with the right coverage. It’s about building a personalized strategy for insurance and financial security.

Embracing Clarity in Coverage: A Lexicon of Deductibles and Out-of-Pocket Costs

To round off, knowing your insurance inside out is not just helpful; it’s empowering. Making sense of the difference between deductible and out of pocket costs is like unlocking a secret code—it puts you in control. So take these insights, strategies, and tools and use them to become a master of your insurance domain, building a safety net that’s as sturdy and reliable as your own understanding. Stay informed, stay prepared, and most importantly, stay on top of your financial well-being.

Understanding the Difference Between Deductible and Out of Pocket

When it comes to health insurance, navigating the maze of terms can be as tricky as trying to find a needle in a haystack. But fear not! Let’s dive into the quirky world of insurance lingo, where we’ll shine a light on the “difference between deductible and out of pocket” – terms that often have folks scratching their heads in confusion.

“Breaking the Ice” with Deductibles

Alright, let’s tackle deductibles first. Think of your deductible like the cover charge at the hippest club in town – you’ve got to pay up before you can enjoy the boogie. It’s the amount you pay each year before your insurance decides to kick in a dime. For example, if your deductible is a cool grand, you’re on the hook to cover those initial medical expenses out of your own designer jean pocket.

But hey, once you’ve hit that magic number, your insurance comes out swinging like the life of the party, covering a chunk of your healthcare costs while your wallet gets a breather. And get this: the concept of insurance deductibles isn’t new. It’s been around well before anyone wondered, When Was Google made, likely even before your grandparents were rocking bell-bottoms!

The Whole “Out of Pocket” Shebang

Now, on to out-of-pocket costs. This term covers the money you continue to shell out even after you’ve met your deductible. These out-of-pocket expenses include co-pays, coinsurance, and even some band-aids that are not covered by your policy. It’s the full meal deal of what you could pay, your financial “worst-case scenario” if you will.

There’s even a safety net in place, known as the out-of-pocket maximum. Once you’ve spent enough to hit this limit, your insurance takes over 100% of the covered costs. It’s like having a fairy godmother for your bank account saying, “I got this,” so you can avoid emptying every last penny into your health care piggy bank.

Dollars and Sense

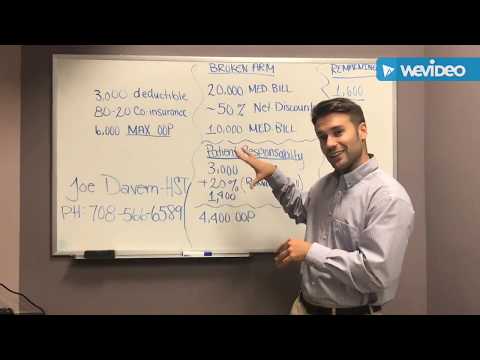

To put it all in perspective, imagine this scenario: You’ve got a $1,500 deductible, and your out-of-pocket max is $6,000. If you undergo a procedure costing $3,000, you’ll pay the first $1,500 (your deductible), and then a part of the remaining $1,500 until you reach your out-of-pocket max. It’s akin to filling up a leaky bucket – once you plug the deductible hole, the coinsurance drips start until the out-of-pocket cap stops the flow entirely.

So there you have it – the “difference between deductible and out of pocket” demystified! Just like understanding how the internet leviathan came to be with “when was Google made,”( getting a grip on these terms is essential for navigating the wild waves of health insurance. Now, armed with this knowledge, you can confidently strut into the insurance arena, ready to tackle your bills head-on like a champ! Remember, sorting through the details matters when it comes to your moolah and your well-being.

Which is more important deductible or out-of-pocket?

Well, it’s like comparing apples and oranges—both the deductible and out-of-pocket costs matter, but for different reasons. Let’s cut to the chase: the deductible is what you pay before your insurance kicks in, while your out-of-pocket maximum is the absolute cap on what you’ll spend in a year. Think of your deductible as the first hurdle and the out-of-pocket maximum as the finish line in the insurance race.

Is deductible and out-of-pocket the same amount?

Hold your horses—deductible and out-of-pocket aren’t twins! Your deductible is just a part of your total out-of-pocket costs, which can also include things like coinsurance and copays. So, nope, they’re definitely not the same amount.

What happens when you reach your deductible?

Alright, when you hit your deductible, cue the confetti—it’s a game-changer! Your insurance starts to share the bill, covering a larger chunk of your healthcare costs. However, you’ll still be paying copays or coinsurance until you hit that golden out-of-pocket maximum.

What happens when you reach out-of-pocket maximum?

Reaching your out-of-pocket max is like hitting the jackpot—bam, no more wallet workouts for covered services for the rest of the year! Your insurance company takes the baton and pays 100% of your covered expenses. Time to breathe easy!

Do copays go towards deductible?

Copays and deductibles—it’s a bit of a juggling act. Generally, copays don’t count towards your deductible; they’re separate payments you make for doctor’s visits or prescriptions. But every plan’s different, so it’s worth a quick check.

Does insurance cover anything before deductible?

Before the deductible, it’s like insurance is playing hard to get—usually, you foot the whole bill. But hey, there are exceptions like preventive care; for that, insurance might cover you right off the bat, no deductible involved!

Is a deductible a set amount?

Ah, the deductible—a number that doesn’t play hide and seek. It’s set each year in your policy, clear as day. Whether it’s a high or low number, that’s your fixed cost target before insurance coverage really kicks into high gear.

What is the quickest way to meet your deductible?

Want to speed-run your deductible? It’s like biting the bullet—schedule those treatments or procedures you’ve been putting off early in the year. Just be sure it’s covered by your plan, and voilà, you’re closer to that deductible finish line.

Is it good to have a $0 deductible?

Zero deductible? Sounds like a free pass, right? But hold on—while it means no initial costs, it often tags in higher premiums. It’s like paying upfront for a smoother ride later.

How can I avoid paying my deductible?

Dodging your deductible? That’s a tough cookie to crumble. Insurance contracts are tighter than a drum. But, if you’re in a pickle, talk to your doctor about payment options or check if your plan has any deductible-free services.

Why am I paying more than my out-of-pocket maximum?

Paying more than your out-of-pocket max is enough to make you blow a gasket—but wait, it could be due to non-covered services or going out-of-network. Time to read the fine print or ring up your insurance to avoid any curveballs!

How do deductibles and out-of-pocket maximums work?

Deductibles and out-of-pocket maximums—a dynamic duo in the health insurance world. Your deductible is the first chunk you pay, then you chip away at the rest with coinsurance or copays until you hit your out-of-pocket maximum. From there, you’re home free, with 100% coverage on eligible expenses.

Do copays count towards out-of-pocket?

Copays joining the out-of-pocket party? You bet! They strut right toward your out-of-pocket maximum, even if they often give the deductible the cold shoulder.

Is it better to pay higher deductible or lower deductible?

Deciding on a higher vs. lower deductible is like picking your poison. High deductible means a lower premium, but more upfront costs. It’s a balancing act—weigh your health needs and financial situation to figure out which brew won’t make you wince.

Is it better to have a high or low deductible?

High or low deductible—what’s the score? A low deductible could be sweet if you see the doc often, but if you’re fit as a fiddle and rarely need care, a high deductible might save you dough on premiums.

Is it better to have a higher premium or higher deductible?

Drum roll, please—for the big premium vs. deductible debate! A higher premium usually tags along with a lower deductible, so you’re paying more monthly but less when you need care. The flip side? A higher deductible means you’re saving on premiums, but if trouble hits, your wallet feels the pinch.

Is a $0 deductible health insurance good or bad?

Zero deductible health insurance—it’s a mixed bag. Perfect if you frequent the doc and want predictable costs, but your premiums might be high enough to make your bank account groan. It boils down to how much you’re willing to pay upfront vs. when you need care.