Deciphering the Balloon Mortgage: An Overview of End-of-Term Scenarios

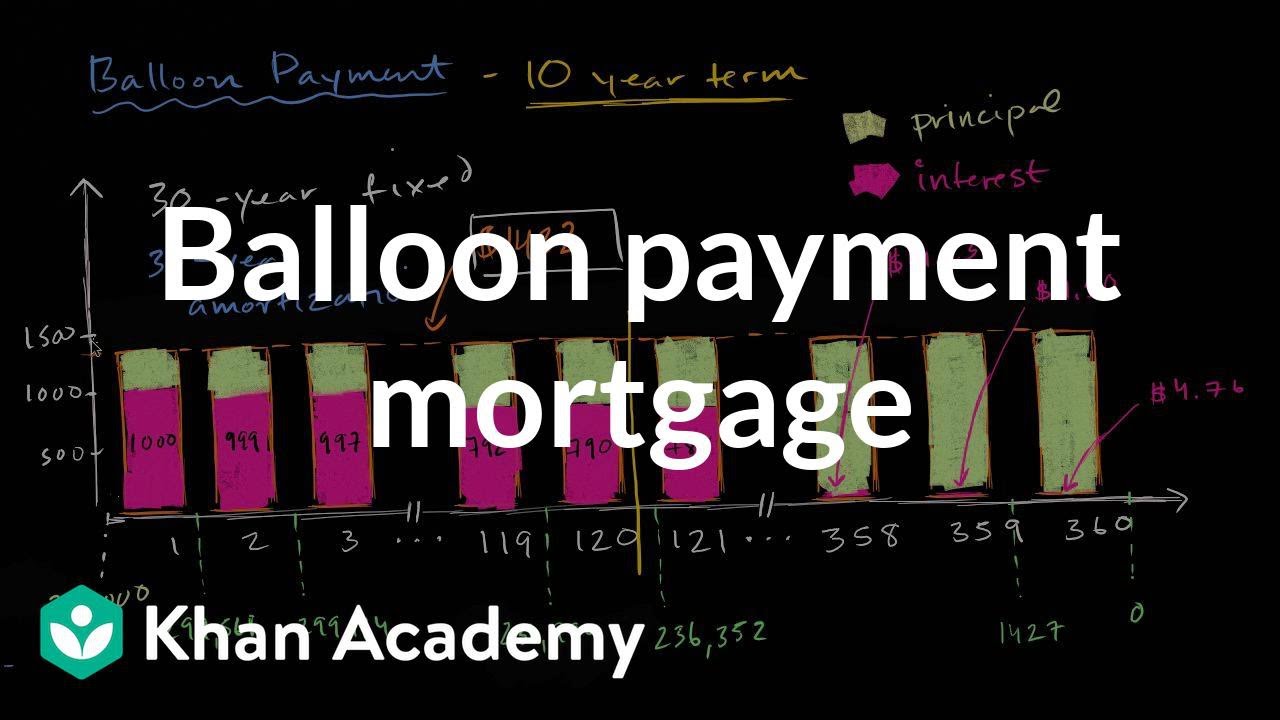

Buckle up, folks, because we’re about to embark on a journey through the ups and downs of balloon mortgages, a short-term and somewhat quirky financial vehicle that can leave some borrowers flying high and others deflated. Let’s start by tackling the basics: a balloon mortgage is like any other home loan, but with a twist. It begins with a series of manageable, fixed payments, and then—bam!—hits you with the “balloon payment” at the end, which is a whopping lump sum that can run you tens of thousands more than you’ve seen before.

Now, before you jump ship, let’s realize that this isn’t your run-of-the-mill mortgage; we’re talking about an Assumable Mortgage that deviates from the norm and could actually work for the savvy borrower.

Historically, balloon mortgages became the talk of the town when regular folks needed lower payments and had a reasonable hunch that they’d only be in their digs for a short while. Over time, as homebuyers have become savvier and the market more complex, the use of balloon mortgages has shifted, but their essence has remained the same, especially now in 2024.

The Final Countdown: Preparing for Your Balloon Mortgage Maturity Date

With the maturity date of a balloon mortgage looming on the horizon, it’s time to buckle down and game plan. Smart money says to start prepping early because nobody wants to be caught with their financial pants down!

Let me tell you about this friend of mine, let’s call him John. John was living the high life in la Casa de Los Famosos, but then got struck with the reality of his balloon mortgage coming due. Panic? Not John. He was squirreling away cash like a clever critter and even considered refinancing early on. That’s thinking ahead!

Now, we’re not saying John’s approach will fit like a glove for everyone, but it offers a snapshot of solid strategies that can help you keep your finances as comfy as a Lovesac bean bag.

| Feature | Description |

|---|---|

| Loan Type | Balloon Mortgage |

| Term Length | Short-term (e.g., 10 years) |

| Initial Payments | Series of fixed payments based on longer-term amortization (e.g., 30 years) |

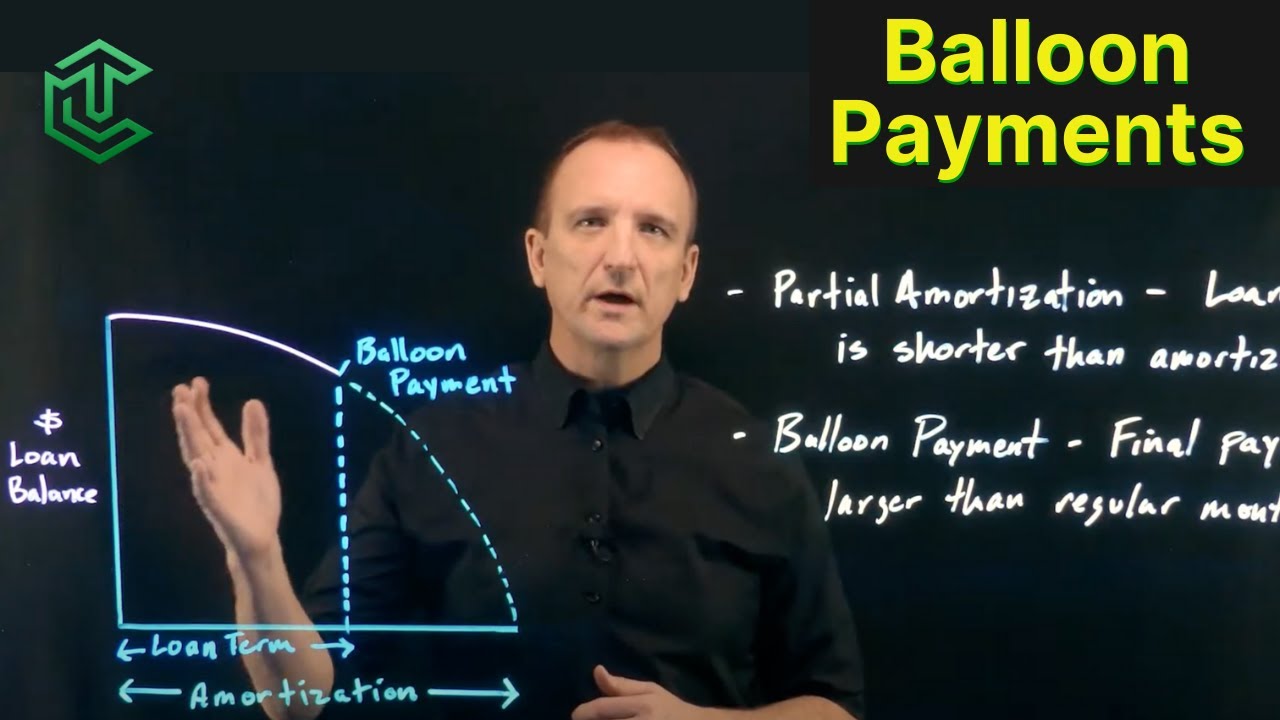

| Balloon Payment | Large lump-sum due at the end of the loan term, often at least twice the size of previous payments |

| Interest Rate (Example) | Fixed at 6.80% (Varies by lender, market conditions, and borrower creditworthiness) |

| Loan Amount (Example) | $280,000 (This will vary based on property value and down payment) |

| Balloon Payment Calculation (Example) | Future Value Formula: FV = PV*(1+r)^n–P*[(1+r)^n–1/r] – assuming a 7.5% annual interest rate |

| Monthly Payment (Example) | Based on a 30-year amortization, but varies by loan specifics |

| Uses | Suitable for borrowers expecting to pay off the loan, refinance, or sell the property before the balloon payment due date |

| Legality | No, not illegal; disallowed on many other mortgage types but allowable under specific loan terms |

| Financial Consideration | May lead to potential financial insecurity if the balloon payment cannot be met |

| Refinancing | Option for borrowers prior to the balloon payment due date |

| Disadvantages | High final payment risk; could pay more in interest over loan term |

| Ideal for | Short-term borrowers with a financial strategy to cover the balloon payment (e.g., investments, inheritance) |

| Balloon vs. Deposit | Balloon payments are made at loan maturity, whereas deposits are paid upfront |

| Alternative Use | Homes, cars, business financing with a clear exit strategy |

Navigating New Terms: Refinancing a Balloon Mortgage

Should you refinance your balloon mortgage, you might wonder? Let’s lay out the breadcrumbs for you. Lenders aren’t just handing out refinancing deals left and right—they’ve got criteria tougher than a Stockard Channing character.

The refinancing process is no walk in the park. It’s a step-by-step dance, from the sweet talk of the Appraisal to the grand finale at closing. But beware; while refinancing can give you more breathing room each month, you might just be waltzing with higher interests or a longer-term commitment.

Is it Popped? What To Do If You Cannot Refinance Your Balloon Mortgage

Let’s not sugarcoat it: if you can’t refinance when your balloon mortgage pops, you’re in a real Bo Derek of a pickle (and not the 10/10 kind). Here’s what you could do:

Failing that, the repercussions are no racist funny Jokes – we’re talking foreclosure signs in your yard and a credit score that’ll plummet faster than a lead balloon.

Payoff Strategies for Balloon Mortgages: Weighing Your Options

Now, if refinancing’s off the table, you’ve got to be nimble on your feet. Coming up with the dough for the balloon payment isn’t for the faint-hearted. Think ahead, strategize, maybe weave some investment magic – remember, you’re the maestro of your financial destiny. That Annual Percentage rate won’t wait for anyone!

The Balloon Mortgage Inside Look: Expert Opinions and Economic Forecasts

What the finance whizzes have to say about balloon mortgages in 2024: It’s not all sunshine and rainbows. Markets are as unpredictable as a soap opera, and interest rates spin faster than a weather vane in a tornado.

Our crystal ball is showing a mixed bag – with housing markets swaying and economies pulling the strings, balloon mortgages remain a wildcard in the deck.

Innovative Balloon Mortgage Products in 2024: A Glimpse into the Future

The mortgage landscape is evolving quicker than a chameleon on a race track, and 2024 is a testament to that. We’re seeing all sorts of fresh, innovative mortgage instruments, with swanky new features that might just make the traditional balloon mortgage look like a relic.

Technology’s turning the industry on its head, too. Fintech’s changing everything – from how you apply for a mortgage to how you pay it off. Brace yourselves; the future’s about to get a whole lot more interesting for those dabbling in balloon mortgages.

Conclusion: Navigating the Balloon Mortgage Landscape with Confidence

Alright, let’s circle back and tie a bow on all we’ve unpacked:

Braving the balloon mortgage waters takes guts and gumption, but armed with the right know-how and a dash of courage, you can do more than just stay afloat – you can swim like a champion.

Remember, with every challenge comes opportunity, and every obstacle, a chance to grow stronger. Here’s to managing your balloon mortgage with smarts, savvy, and maybe a bit of swagger too. Happy house hunting!

Balloon Mortgage: The Countdown to Lift-Off!

Well, folks, get ready for a ride with the concept of a balloon mortgage, which can be as thrilling as a space launch but involves your home finance instead of a rocket! So, strap in as we countdown to some high-flying trivia and interesting facts that will surely keep you on the edge of your seat.

Balloon Mortgage: A Blast from the Past!

Balloon mortgages might sound like the latest craze, but guess what? They’re not new kids on the block. Picture this: it’s the 1920s, flappers are dancing the Charleston, and folks are using balloon mortgages to buy those charming craftsman homes. Back in the day, this type of home loan was all the rage—before long-term loans with fixed interest rates came into the picture and grabbed the spotlight.

Up, Up, and Away… Until the Payment’s Due!

So, you’re probably wondering, “What’s up with the name?” Well, it’s all about the swiftness of the payoff. You see, with a balloon mortgage, you pay interest and maybe a bit of the principal here and there for a set period. And then—bam!—the remaining balance swells up and comes due all at once, just like a big ol’ balloon popping at the end of a party. And when that day comes, you better have a plan, because if you don’t, you could be in for a bumpy landing.

The Refinance Rollercoaster: Hold On Tight!

Hang on to your hats, mortgage mavens! When the end of the term is looming, many homeowners look to refinance their balloon mortgage. But here’s the kicker—refinancing isn’t a walk in the park. It’s more like a rollercoaster ride with its ups and downs, and twists and turns, depending on your financial health, credit score, and market conditions. If you can refinance, you might just be able to stay on the property merry-go-round a little longer. If not, well, let’s hope you’ve got a backup plan!

Balloon Mortgage or Fixed-Rate Mortgage? That is the Question!

Debating between a balloon mortgage and a fixed-rate mortgage? It’s like choosing between a mystery grab bag and a predictable present. Some folks reckon it’s smarter to go with a fixed-rate because, let’s face it, knowing your payment will stay the same every month is as comforting as Sunday pot roast at Grandma’s. But adventurers and risk-takers might fancy the lower initial payments of a balloon mortgage. Word to the wise—make sure you’ve got a hefty piggy bank or a golden parachute if you’re playing the balloon mortgage game!

When the Party’s Over: The Balloon Mortgage Comeuppance

Alright, party animals, when the fiesta wrap-up is nigh, some borrowers face the music with the sale of their humble abode. If the house has gone up in value, they could walk away with a tidy sum after saying adios to the mortgage. But if the market’s taken a nosedive, it could be more like the morning after a wild shindig—headaches and regrets, not to mention the stark realization that you owe more than your house is worth!

Remember, choosing a balloon mortgage is no joke—it’s a financial gamble, a leap of faith into the unknown. But if you play your cards right, stay keen on the market, and have a solid Plan B, this climax could be the kind of thrills you were looking for. Just don’t let that balloon payment catch you off guard, or you could be yelling “Mayday!” instead of “Yippee!”

And there you have it! Whether you’re a seasoned homebuyer, a finance whizz, or just mulling your options, I hope you enjoyed this trivia-filled jaunt into the world of balloon mortgages. Stay savvy, readers, and make sure your financial parachute is packed and ready—just in case!

How does a balloon mortgage work?

How does a balloon mortgage work?

Well, hold onto your hats, because a balloon mortgage is quite the ride! You start off paying smaller monthly payments, mostly covering interest, for a short stint—say 5 to 7 years. But here’s the kicker: when the term’s up, bam! You’re hit with a lump-sum payment, the ‘balloon’ part, which covers the rest of what you owe. So think of it like eating your veggies before getting to the giant meatball at the end of your fork!

Are balloon loans a good idea?

Are balloon loans a good idea?

Ah, the million-dollar question—or should I say ‘balloon-sized’ question! Whether a balloon loan is a bright idea or a financial faux pas totally depends on your situation. If you’ve got a plan to rake in some cash to pay off that big balloon payment down the road, or you’re betting on selling the property before the payment comes due, it might work out. But for the rest of us, it’s like playing financial hot potato, and that potato could get pretty darn hot!

Is a balloon mortgage illegal?

Is a balloon mortgage illegal?

Nope, no siree—it’s all above board! Balloon mortgages aren’t illegal. In fact, they’re a legit financing option, but they’re not your run-of-the-mill type of loan. They come with a unique set of rules and are designed for specific situations. Just like jaywalking, not a crime, but you’d better look both ways before you cross!

What are the disadvantages of balloon mortgages?

What are the disadvantages of balloon mortgages?

Where do I start? Disadvantages of balloon mortgages are like a long, bumpy list of “what ifs.” What if you can’t afford the huge final payment? What if your plans to sell or refinance fall through like a weak floorboard? The uncertainty can really tie your stomach in knots. Plus, if interest rates rocket up or your financial situation takes a nosedive, refinancing could be like trying to catch a greased pig.

Why do people avoid balloon mortgages?

Why do people avoid balloon mortgages?

Well, most folks steer clear of balloon mortgages like they’d avoid a skunk at a picnic. It’s all about that hefty final payment lurking at the end. Many borrowers find it unsettling to gamble on future financial stability or real estate market conditions—it’s a bit like betting on the weather. Plus, not knowing if you’ll be able to refinance can really keep you up at night!

Are balloon mortgages risky?

Are balloon mortgages risky?

Risky is as risky does, and yes, balloon mortgages can be like walking a financial tightrope without a net. The risk is sky-high because that final payment is massive compared to your earlier monthly payments. If you can’t make the balloon payment, refinance, or sell the property, you could end up foreclosing, which is a fancy way of saying you could lose your shirt—and the house!

Who is balloon mortgage best for?

Who is balloon mortgage best for?

A balloon mortgage fits like a glove for someone with a crystal-clear crystal ball—think real estate tycoons or those with a golden goose, expecting a windfall in the short term. It’s great for folks who plan to sell or flip the property before the big payment rears its head. So, if you can predict your financial future like a pro, a balloon mortgage might just be your magic carpet!

Can I pay off balloon loan early?

Can I pay off balloon loan early?

You betcha! Most times, you can pay off a balloon loan early, and there ain’t no party like an “early loan payoff” party. It’s like leaving the party before it gets too rowdy—you dodge that looming balloon payment and peace out with your property in hand. Just check the fine print for any prepayment penalties that might rain on your parade.

Why are balloon payments bad?

Why are balloon payments bad?

Whoa, Nelly! A balloon payment isn’t just a gentle bump in the road—it’s like hitting a pothole the size of Texas. They’re tricky because they come at the end of your loan term and can be a real whopper, much more than your regular monthly payments. If you’re not ready for it, a balloon payment can knock the wind out of your finances faster than a bull in a china shop.

What is a 5 year balloon mortgage?

What is a 5 year balloon mortgage?

Imagine you’re on a five-year financial sprint! That’s what a 5 year balloon mortgage is. You’ve got low monthly payments for five years, light as a feather, but when the clock strikes five, brace yourself. The entire remaining balance of the mortgage zooms in like a boomerang, and you have to pay off the rest of the loan, pronto!

What is a 5 year balloon with a 30 year amortization?

What is a 5 year balloon with a 30 year amortization?

Alright, picture this: you’re paying off your loan as if you had all the time in the world—like a leisurely 30-year stroll in the park. That’s what the 30-year amortization part is. But, plot twist! After just five years, you’re hit with the balloon part, where the remaining balance comes due in a lump sum. It’s like enjoying a long hike but having to sprint the last mile!

What is the typical life span of a balloon mortgage?

What is the typical life span of a balloon mortgage?

Short and sweet, the life span of a balloon mortgage is usually like a comet—dazzling but brief. Terms often range from 5 to 7 years before that big balloon payment comes due, and you’ve gotta settle accounts. So, don’t get too comfy—it’s a sprint, not a marathon!

How do I get out of a balloon mortgage?

How do I get out of a balloon mortgage?

Looking to high-tail it out of a balloon mortgage? You’ve got options! You can refinance that bad boy for a more traditional loan, sell the property to cover your bases, or make an over-the-top payment to deflate the balloon once and for all. Just make sure you’ve got your escape plan ready before that final payment swells up on the horizon.

What is the advantage of a balloon mortgage?

What is the advantage of a balloon mortgage?

Believe it or not, balloon mortgages do have their upside. They can be a real peach if you’re looking for lower initial monthly payments or planning to sell the property ASAP. It frees up some cash flow in the short term, so if you’re juggling your finances like flaming torches, that extra breathing room can be mighty handy.

What is a 5 year balloon with a 30 year amortization?

What happens if I can’t pay my balloon payment?

Alright, if you find yourself staring down the barrel of a balloon payment with empty pockets, you’re in a bit of a pickle. You might have to hustle to refinance, which depends on whether you’re still financial hot stuff or not. Worse comes to worst, if you can’t refinance, sell, or pay it off, foreclosure might be breathing down your neck. It’s crunch time, so you’ll need to act fast!

What happens if I can’t pay my balloon payment?

What happens at the end of a balloon mortgage term?

The end of a balloon mortgage term is showtime! You’ve reached the finale where you either cough up the balloon payment in full, take a bow, and own your home outright or hustle to refinance or sell the property before the curtain drops. If none of these acts come together, it might be curtains for your ownership. So make sure you’ve got a plan for the final act!