When it comes to the joys of homebuying, few terms can cause wide-eyed confusion quite like “Amortization Schedule.” But hang tight, folks! If you’ve been scratching your head over this mortgage puzzle, you’re about to crack the code. Let’s dive into the nitty-gritty in five simple steps, saving you the need to ask What Is a mortgage? all over again.

Decoding Your Amortization Schedule: A Homeowner’s Guide

Mortgage Loan Monthly Amortization Payment Tables Easy to use reference for home buyers and sellers, mortgage brokers, bank and credit union loan … of a given amount, term, and interest rate.

$16.95

The “Mortgage Loan Monthly Amortization Payment Tables” is an indispensable tool designed for a variety of users engaged in the real estate market. Whether you’re a first-time homebuyer, a seasoned property seller, a diligent mortgage broker, or a loan officer at a banking institution or credit union, this easy-to-use reference material simplifies the process of determining monthly loan payments. By providing a comprehensive matrix of amortization schedules, the tables allow users to quickly identify the monthly payment for a mortgage based on the loan’s principal amount, repayment term, and interest rate. This enables effective budget planning and financial forecasting, crucial for making informed decisions in the property market.

Crafted for clarity and convenience, the tables save users from complex calculations, presenting a clear trajectory of how a loan amortizes over time. Each page details a specific combination of loan attributes, allowing users to flip to the corresponding section and immediately find the information relevant to their needs. With a wide range of term lengths and interest rates covered, the tables cater to a variety of financing scenarios, ensuring that users can project payments for both conventional and adjusted loan structures. This at-a-glance format is ideal for comparing different loan options and determining the long-term financial impact of each.

Moreover, this resource is not only practical but also a time-saver during client consultations for mortgage professionals. It enhances client understanding and trust by providing transparent, digestible information on potential monthly repayments and the overall cost of credit. The Mortgage Loan Monthly Amortization Payment Tables serve as a reassuring roadmap for navigating the often complex terrain of mortgage planning, solidifying it as a must-have in the arsenal of every real estate industry professional. Whether in the office or on the go, this guide ensures that accurate payment calculations are always within reach, fostering confidence and competency in every transaction.

Step 1: Unraveling the Basics of an Amortization Schedule

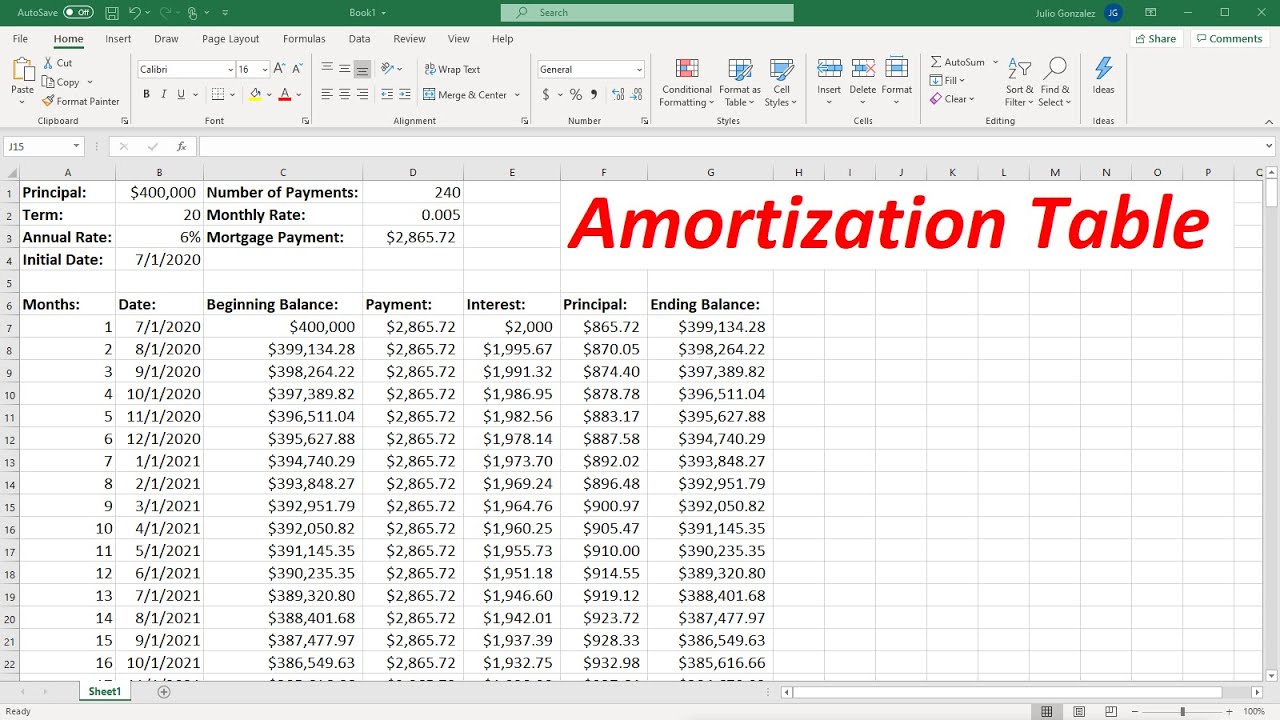

To start, let’s get down to brass tacks: what exactly is this all-important Amortization Schedule? Simply put, it’s a table detailing each periodic payment on a loan and plays a crucial part in mortgage planning. Now, don’t let your eyes glaze over just yet. Stick with me.

With a fixed-rate mortgage, the amortization schedule is a homeowner’s best pal for predicting financial commitment. Every month, like clockwork, you know what’s due. Variable-rate mortgages, however, have schedules that are a bit more, let’s say, dynamic. The interest bit can fluctuate, making the payment amounts shift over time. You’ll find more on this rollercoaster under our Adjustable-rate Mortgage chat.

Here’s the scoop on how an Amortization Schedule is structured:

– Chalk up the total loan amount – that’s your principal.

– The interest doesn’t stay put; initially, it’s like a needy friend demanding much of your payment.

– Over time, though, the principal chews up more of each installment until it’s all paid off.

Step 2: Dissecting the Numbers: How to Read Your Amortization Schedule

Navigating your Amortization Schedule is simpler than a Wordle today answer. It’s got columns and rows that spell it all out: payment dates, what’s going toward the principal, the interest amount, and the remaining loan balance.

Ping! Lightbulb moment: payment periods affect how quickly you crush the loan. Say you’ve got a monthly payment plan; it’ll whittle the balance differently than a bi-weekly approach.

And for those eager beavers making early payments, you can give yourself a pat on the back as you watch your interest bleeds dry, speeding up the principal’s demise. Ain’t that a sight?

Step 3: The Impact of Interest Rates on Your Amortization Schedule

Interest rates – they’re fickle beasts, always on the move. When they change, they nudge your Amortization Schedule into a new groove. For instance, let’s chat refinancing – some folks do it to snag a better rate, reshuffling the schedule deck.

Here’s a golden nugget: staying on top of interest rate changes is like knowing when to fold or hold in poker. It can save you a bundle or leave you reaching for the antacids.

Strategies for keeping calm and carrying on include locking in a low rate or riding the variable rate waves with an eagle eye.

The Mortgage Payment Handbook Monthly Payment Tables and Yearly Amortization Schedules for Fixed Ra

$50.12

The “Mortgage Payment Handbook: Monthly Payment Tables and Yearly Amortization Schedules for Fixed Rate Mortgages” is an essential resource for anyone navigating the complexities of home financing. This comprehensive guide provides clear and easy-to-use tables that answer the critical question: “How much house can I afford?” With tables for a wide range of loan amounts, interest rates, and terms, this manual allows you to quickly identify the monthly payments for various mortgage scenarios. It is designed to simplify financial planning for prospective homeowners, real estate professionals, and financial advisors alike.

Beyond just monthly payment tables, this handbook elaborates on the long-term view of a mortgage by including yearly amortization schedules. These schedules show the progression of payments over the life of the loan, specifying how much of each payment goes towards the principal balance versus interest. This is invaluable for those wishing to understand the impact of additional principal payments or for those considering refinancing. The amortization schedules presented in this handbook are useful tools for managing personal finance and making more informed decisions about real estate investments.

The “Mortgage Payment Handbook” is not just a reference document; it is also an educational tool that demystifies the often-intimidating world of mortgage calculations. It explains the principles behind the numbers, aiding users in grasping the realities of interest accrual and debt reduction. This information is especially helpful for first-time homebuyers who are looking to establish a solid understanding of mortgage terms and conditions. Thus, this handbook stands as a go-to guide for anyone seeking clarity and control over their home financing decisions.

Step 4: Advanced Insights: Using Your Amortization Schedule for Strategic Planning

Wisdom comes from experience, and getting strategic with your Amortization Schedule can turn you into a financial guru.

First off, it’s a blueprint for your money movements. Need to budget for that shiny new car or, perhaps, promise rings for that special someone? Peeking at the schedule shows you how your loan plays with your cash flow.

Second, sprinkling in extra payments isn’t just generous; it’s clever. Doing this is like telling your interest, “Not today, buddy!” – and who wouldn’t love that?

Last, but not a bit least, use this cipher to time your big moves. Refinancing or selling the homestead? The schedule won’t lie. If the numbers say go, then you might just want to grab those boots and do-si-do!

Step 5: Navigating Amortization Schedule Changes and Variances

Life’s a curveball-hurling pitcher, so when your loan terms change, expect your schedule to swing along. Loan mods, payment vacations, and the big-hearted forbearance can all leave their mark.

Nobody likes oopsies, but they happen, especially with Amortization Schedule surprises. Maybe you missed the fine print, or perhaps you got a bit too festive and skipped a payment. Keep your eye on the ball to prevent such stumbles.

To bring it home, here’s a real zinger: folks have ridden the tide of schedule changes to land on sunny financial shores. It involves a dash of wisdom and a sprinkle of courage – a recipe for success.

Conclusion: Mastering Your Mortgage’s Tempo

Alright, aspiring maestros, your baton is the knowledge we’ve just riffed through. Five steps to Amortization Schedule enlightenment, and you’re now tuned up to conduct your mortgage melody with confidence.

Remember to stay proactive with your schedule, and treat it as your very own financial GPS. It’ll steer you clear of potholes and keep you rolling on that road to payoff paradise.

And with parting thoughts, gaze toward the horizon. Mortgages, interest rates, and Amortization Schedules – they’re all doing the tango in an ever-twisting financial ballroom. So, keep your steps light and nimble, and who knows? You might just waltz your way to a payoff that’s music to your ears.

Amortization Schedule

$0.00

The “Amortization Schedule” is an essential tool for individuals and businesses managing loans and mortgages, providing a detailed breakdown of each payment throughout the life of the loan. This comprehensive schedule displays the proportion of each installment that goes towards the principal balance versus the interest, allowing borrowers to see exactly how their loan decreases over time. An amortization schedule is particularly useful for fixed-rate loans, where each payment is the same total amount, but the actual amounts applied to principal and interest change with each payment.

The Amortization Schedule product is designed to be user-friendly and customizable for a variety of loan types, including personal loans, home mortgages, auto loans, and business loans. The intuitive interface allows users to input their loan amount, interest rate, loan term, and start date to instantly generate a personalized repayment plan. The format provides a clear visual representation of the decreasing interest portion and the increasing principal portion with each successive payment.

In addition to its primary function, the Amortization Schedule offers extra features such as the ability to calculate the impacts of extra payments on the loan’s lifespan and overall interest paid. Users can plan and strategize for early payoff scenarios, or simply gain insight into how additional payments could accelerate equity building. With a printable and exportable format, the Amortization Schedule is a handy tool for financial planning, tax preparation, and communicating with financial advisors or lenders about loan progress.

As we close the curtain, let’s pay tribute with a heartfelt in memory Of My brother who Passed away, who inspired us to always look ahead, and to Jamesy Boy, whose resilience reminds us that every step of the financial journey is a step towards growth and understanding. Keep dancing to the rhythm of your amortization, and your financial future will be as bright as you’ve orchestrated it to be.

Dive Into the World of Your Amortization Schedule!

Hold your horses! Before you gallop into the sunset with your mortgage keys in hand, let’s have some fun unraveling the twists and turns of your amortization schedule. Think of it as the roadmap for your home loan journey, showing you every nook and cranny of your payments from now ’til kingdom come.

The Early Bird Gets More Interest

Ya know, in the wacky world of amortization, the early payments are like a overly-enthusiastic friend—loaded with interest. It’s as if they’re saying, “Hey, pay attention to me first!” But as the years roll by, principal, that shy buddy in the background, starts to come out of its shell. By the end, you and principal are best pals, sharing the lion’s share of your payment pie.

The Plot Twist of Extra Payments

Just when you think you’ve got your amortization schedule all figured out, bam! You decide to throw in some extra payments, and it’s like a plot twist in a Nicholas gonzalez movie—you’re speeding up the drama and cutting to the finale quicker. Making extra payments can shave off years like a time machine, tweaking your script for an even happier ending.

The Numbers Nerdfest

Look, I get it. Numbers might not be everyone’s cup of tea. But when they line up in an amortization schedule, it’s like watching a beautiful symphony of digits. Each payment is meticulously planned, like a choreographed dance between you and your lender. So don your nerdy glasses and embrace the beauty of it all—it’s honestly kind of mesmerizing!

The Balloon Payment: The Big Shebang!

Occasionally, some amortization schedules come with a grand finale—a balloon payment. This hulk of a payment waits in the shadows until—wham!—it’s time to pay up, and it’s go big or go home. This isn’t for the faint of heart, but hey, it sure adds a dash of excitement to your payment journey!

Time Heals All… Debts?

Isn’t it wild how time works its magic on your amortization schedule? In the beginning, it may seem like your debt’s a mountain that’s too steep to climb. But give it some time, and you’ll be singing “Ain’t No Mountain High Enough” all the way to your last payment. It’s like watching your favorite long-running TV series—eventually, you reach that satisfying finale.

So, keep your eyes on the prize, and remember, your amortization schedule is the key to unlocking the mysteries of your mortgage. It’s spaced out so perfectly over time that, before you know it, you’ll be toasting to a mortgage well-managed. Cheers to that! 🥂

Monthly Payment Amortization Schedule Loan,Mortgate Payment, Term, and Start Date, Savings Plan, Savings Prompts, Monthly Budget Planner, Annual … , Record Balance ,And Interest X”

$8.61

Introducing the “Xtreme Finance Planner,” a comprehensive tool designed to streamline your financial management and help you achieve your fiscal goals with precision. The planner’s core feature is its Monthly Payment Amortization Schedule, which is essential for anyone managing loans or mortgages. Enter your loan amount, interest rate, term, and start date to receive a detailed breakdown of monthly payments, showing how much of each payment is applied toward the principal balance versus interest, helping you to understand the lifecycle of your loan. This clarity empowers you to plan for extra payments and visualize the impact on the loan’s term, ensuring you can save on interest and pay off debts more quickly.

The planner goes beyond loan management by including a meticulously structured Savings Plan section, coupled with motivating Savings Prompts to keep you on track towards your financial objectives. Be it for an emergency fund, a major purchase, or retirement, set your targets and let the planner guide you through systematic monthly contributions. The prompts provide timely reminders and actionable advice to boost your savings habit, adapting to your progress and keeping you accountable. With this tool, you’re not just paying off debts; you’re also building wealth, striking the perfect balance between today’s liabilities and tomorrows aspirations.

To complement these features, the Xtreme Finance Planner encompasses a Monthly Budget Planner along with an Annual Snapshot, enabling complete oversight of your financial health. The monthly budget planner helps you categorize and allocate funds efficiently, avoiding overspending, and staying mindful of cash flow. At year’s end, the annual summary provides a panoramic view of your financial journey, allowing you to assess performance and adjust strategies. All this, paired with a Record Balance and Interest section, ensures that every dollar is accounted for, optimizing your financial well-being and offering you peace of mind as you navigate through your fiscal year.

How to do an amortization schedule?

Alright, let’s dive into these FAQs with some jazzed-up, digestible answers:

How to calculate amortization in Excel?

Wondering how to do an amortization schedule? It’s like baking a cake, but with numbers! Start out by grabbing a loan’s principal amount, interest rate, and term length. Then break down each payment by month, slicing your payment into interest and principal portions until the balance hits zero. Voila, you’ve got a complete schedule!

How do I get a loan amortization schedule?

Want to calculate amortization in Excel? Excel’s your financial Swiss Army knife for this! Use the PMT function to determine the periodic payment, then plug and chug with IPMT and PPMT to find the interest and principal. Column by column, you’ll unveil the grand mystery of your loan’s future.

How do I see my amortization schedule?

Need a loan amortization schedule? Don’t fret! Most lenders are happy to provide one when your loan’s all set up. Just ask ’em for it, or, if you’re tech-savvy, online calculators or spreadsheet programs are ripe for the picking!

What happens if I pay 2 extra mortgage payments a year?

Curious to see your amortization schedule? Give a shout to your lender—they usually hand these out or have ’em on their websites. Alternatively, get crafty with some software or an online tool, punch in your loan details, and there you have it; it’s as easy as pie.

What is an example of amortization?

If you toss 2 extra mortgage payments a year into the mix, you’re looking at chopping down that interest like a lumberjack and saying “hasta la vista” to your loan years ahead of schedule. It’s like finding a shortcut on your drive home!

What is the easiest way to calculate amortization?

An example of amortization? Imagine buying a shiny new car for $20,000 with a 5-year loan. Amortization is the roadmap showing how each payment takes a little bite out of the interest and principal until you’re cruising debt-free.

Does Excel have amortization template?

The easiest way to calculate amortization? Snag an online amortization calculator where you just punch in the loan details and bam! It spits out a schedule so you can skip the number crunching and get straight to the good stuff.

Can Excel make an amortization schedule?

Does Excel have an amortization template? You betcha! It’s like Excel’s got your back with a ready-to-use template where all you do is input your loan details. Instantly, you’ve got a full-blown schedule without starting from scratch.

Can I make my own amortization schedule?

Can Excel make an amortization schedule? Absolutely, that’s Excel’s bread and butter. Plenty of functions and templates in there can help you build one from the ground up, like a financial DIY project.

How do you calculate monthly payments on a loan?

Can I make my own amortization schedule? Sure thing! Roll up your sleeves and create one in Excel, or find an online calculator where you input your digits and let it do the heavy lifting. It’s like making a mixtape, but for your loan.

What is the formula for the monthly payment?

How do you calculate monthly payments on a loan? It’s a piece of cake! Take your loan amount, sprinkle in the interest rate and loan term, then use the PMT function in Excel or an online loan calculator. Voilà, your monthly payment is served!

Can I ask my bank for an amortization schedule?

What is the formula for the monthly payment? It’s the sort of recipe where you mix the loan amount with a dash of interest, over the number of payments. The precise formula is a bit of a jigsaw puzzle, but that’s the general gist!

What is a normal amortization schedule?

Can I ask my bank for an amortization schedule? Oh, for sure! Banks and lenders are usually more than willing to hand over an amortization schedule. It’s like asking for extra napkins with a take-out order—they’ve got you covered.

What is a 10 year loan with 25 year amortization?

What is a normal amortization schedule? It’s just your standard loan life story. Payments are divvied up, usually monthly, with early payments being mostly interest and the balance shifting more toward the principal as time marches on.

What is the formula for monthly amortization?

What is a 10-year loan with a 25-year amortization? Think of it like a cliffhanger TV show with an extended series finale; you’ve got 10 years of fixed payments, but they’re stretched out as if the loan’s over 25 years, meaning a balloon payment or new terms when the initial decade ends.

What is the first step in creating an amortization schedule?

What is the formula for monthly amortization? The formula is like a secret sauce—complex, but tasty! It involves the total loan amount, the interest rate per period, and the total number of periods. For the exact recipe, grab a financial calculator or Excel to lend a hand.

What is the formula for amortization in accounting?

What is the first step in creating an amortization schedule? First things first, gather your ingredients: loan amount, interest rate, and length of the loan. It’s like prepping to make a stew; without these bits, you’re going nowhere fast.

What does 5 year term 20 year amortization mean?

What is the formula for amortization in accounting? In the accounting kitchen, the amortization formula is like your grandma’s secret recipe. It takes the initial cost of an intangible asset and divides it by the asset’s useful life—spreading the cost as expenses over time, baking it evenly into financial statements.